Profits, Scale Economies, and the Gains from Trade and Industrial Policy

Ahmad Lashkaripour (Indiana University, CESifo, CEPR)

Volodymyr Lugovskyy (Indiana University)

American Economic Review · October 2023

Read PDF · Markdown source · Reader view · Slides · Online appendix

Abstract. This paper examines the efficacy of second-best trade restrictions at correcting sectoral misallocation due to scale economies or profit-generating markups. To this end, we characterize optimal trade and industrial policies in an important class of quantitative trade models with scale effects and profits, estimating the structural parameters that govern policy outcomes. Our estimates reveal that standalone trade policy measures are remarkably ineffective at correcting misallocation, even when designed optimally. Unilateral adoption of corrective industrial policies is also ineffective due to immiserizing growth effects. But industrial policies coordinated internationally via a deep agreement are more transformative than any unilateral policy alternative.

The United States will likely adopt an explicit industrial policy in the coming decade. Similar developments are well underway in other countries (Aiginger and Rodrik (2020)). And with industrial policy back on the scene, we are witnessing a revival of old-but-questionable trade policy practices. Govenments are often turning to protectionist trade policy measures to pursue their industrial policy objectives—as manifested by the United States National Trade Council’s mission or the Chinese, Made in China 2025 initiative.See Bhagwati (1988) and Irwin (2017) for a historical account of trade restrictions being used by governments to promote their preferred industries. A prominent example dates back to 1791, when Alexander Hamilton approached Congress with “the Report on the Subject of Manufactures,” encouraging the implementation of protective tariffs and industrial subsidies. These policies were intended to help the US economy catch up with Britain.

These developments have sparked new interest in old-but-open questions regarding trade and industrial policy. For instance: \(\boldsymbol {(i)}\) Is trade policy an effective tool for correcting misallocation in the domestic economy? \(\boldsymbol {(ii)}\) If not, should governments undertake unilateral domestic policy interventions to correct misallocation? or \(\boldsymbol {(iii)}\) should they coordinate their industrial policies via a deep trade agreement?

To answer these questions, we characterize optimal trade and industrial policies in an important class of multi-industry, multi-country quantitative trade models where misallocation occurs due to scale economies or profit-generating markups. Guided by theory, we estimate the key parameters that govern the welfare consequences of trade and industrial policy in open economies. We then combine our estimated parameters with optimal policy formulas to quantify the ex-ante gains from trade and industrial policy among 43 major countries.

Our estimation reveals that trade policy is remarkably ineffective at correcting misallocation, reflecting a deep tension between allocative efficiency and terms of trade. Unilateral adoption of corrective industrial policies can also backfire as it often triggers immiserizing growth. These considerations, we argue, may have spurred a global race to the bottom, wherein governments either avoid corrective industrial policies or pair them with hidden trade barriers. A deep agreement can remedy this problem and deliver welfare gains that are more transformative than any unilateral policy intervention.

Section 1 presents our theoretical framework. Our baseline model is a generalized multi-industry Krugman (1980) model that features a non-parametric utility aggregator across industries and a nested CES utility aggregator within industries. This specification has an appealing property wherein the degrees of firm-level and country-level market love-for-variety can diverge. We analyze both the restricted and free entry cases of the model to distinguish between the short-run and long-run consequences of policy. With a reinterpretation of parameters, our baseline framework also nests \((a)\) the multi-industry Melitz (2003)-Pareto model, and \((b)\) the multi-industry Eaton and Kortum (2002) model with industry-level Marshallian externalities. We later extend our baseline model to accommodate non-parametric input-output linkages.

Section 2 derives sufficient statistics formulas for first-best and second-best trade and industrial policies. Unilaterally optimal policies in our framework pursue two objectives: First, they seek to improve the home country’s terms-of-trade (ToT) vis-à-vis the rest of the world. Second, they seek to restore allocative efficiency in the domestic economy by reallocating workers towards high-returns to scale or high-profit industries.

The first-best optimal policy consists of misallocation-blind import tariffs and export subsidies that purely maximize ToT gains. Allocative efficiency under the first-best is restored via domestic Pigouvian subsidies.The optimal subsidy rate in each industry equals the inverse of the industry-level scale elasticity or markup. While these insights resonate with the targeting principle, our optimal policy formulas have other implications worth highlighting. First, even though 1st-best trade policies are blind to misallocation (the dispersion in scale elasticities), they depend on the overall strength of scale economies (the level of scale elasticities). Second, the optimal tariff formula is input-output-blind provided that export subsidies are assigned optimally.Specifically, optimal import tariffs are equal to the inverse export supply elasticity regardless of input-output relationships. Consequently, in the absence of profits and scale economies, optimal tariffs become uniform when export subsidies are set optimally—revealing that the uniformity result in Costinot et al. (2015) extends to environments with input-output linkages.

Our second-best trade policy formulas apply to scenarios where governments are reluctant to use industrial subsidies for correcting misallocation—the root of which could be political pressures or institutional barriers.Trade policy has been regularly used—in place of domestic industrial policy—to promote critical industries (Bhagwati (1988); Harrison and Rodríguez-Clare (2010); Irwin (2017)). Relatedly, see Lane (2020) for a historical account of various industrial policy practices around the world. Second-best trade tax-cum-subsidies are composed of two elements: a neoclassical ToT-improving component and a misallocation-correcting component. The former aims to restrict relative exports in nationally differentiated industries. The latter seeks to restrict imports and promote exports in high-returns-to-scale industries, mimicking the first-best Pigouvian subsidies.

Section 3, guided by our optimal policy framework, puts forth two conjectures concerning the efficacy of trade and industrial policy: First, if industry-level trade and scale elasticities exhibit a strong negative correlation, standalone trade policy measures deliver limited welfare gains even when set optimally—reflecting their inability to strike a balance between ToT-improving and misallocation-correcting objectives.In some canonical cases, optimal second-best trade policies are even industry-blind—unable to beneficially correct inter-industry misallocation or manipulate the ToT on an industry-by-industry basis. Second, in these conditions, unilateral scale (or markup) correction via industrial policy can cause immiserizing growth due to adverse ToT effects. Consequently, shallow trade agreements may be insufficient for reaching global efficiency. Once governments agree to abandon inefficient trade restrictions under a shallow agreement, they become tangled in a coordination game involving corrective industrial policies. The outcome of this game is a race to the bottom wherein governments are reluctant to implement corrective industrial policies without violating their commitments to free trade. A deep agreement can remedy this problem.

To test these conjectures, Section 5 estimates the structural parameters necessary for ex-ante policy evaluation. Our optimal policy formulas reveal that the sufficient statistics for measuring policy outcomes include observables and two sets of parameters: \((i)\) industry-level scale elasticities that govern the extent of misallocation and \((ii)\) industry-level trade elasticities that control the scope for ToT manipulation. In our generalized Krugman (1980) model, scale elasticities reflect the degree of love-for-variety whose social benefits are not internalized by firms’ entry decisions; and trade elasticities represent the degree of national product differentiation. We recover both elasticities from firm-level demand parameters, which are estimated by fitting a structural demand function to the universe of Colombian import transactions covering over 225,000 firms from 251 countries. Our identification strategy leverages high-frequency data on import transactions and exchange rates to construct a shift-share instrument that measures exposure to aggregate exchange rate fluctuations at the firm-product-year level.We develop this identification strategy to overcome challenges that are difficult to resolve with standard demand estimation techniques. Firm-level demand estimation techniques from the Industrial Organization literature leverage information on observed product characteristics, which are unavailable at the scale we conduct our estimation. Also, unlike traditional country-level import demand estimations, we cannot rely on tariff data for identification, as tariff rates do not vary sufficiently among firms from the same country. This estimation strategy is well-suited for our end goal of policy evaluation as it separately identifies the scale elasticities from trade elasticities, accurately pinpointing their covariance.

Section 6 combines our estimated scale and trade elasticity parameters, our optimal policy formulas, and macro-level data from the 2014 World Input-Output Database to quantify the (maximal) ex-ante gains from policy among 43 major economies. Our analysis delivers three main findings.

First, we find that trade policy is remarkably ineffective at correcting misallocation in the domestic economy—even without factoring in the cost of retaliation by trading partners. Under free entry, second-best export subsidies and import taxes can raise the average country’s real GDP by only 1.19%, which amounts to less than \(\frac{4}{10}\) of the gains attainable under the unilaterally first-best policy. Third-best import taxes are even less effective as a standalone policy, raising real GDP by a mere 0.63%. These findings corroborate the argument that trade policy has difficulty striking a balance between ToT and misallocation-correcting objectives.

Second, the unilateral adoption of corrective industrial policies triggers severe immiserizing growth in most countries. The average country’s real GDP declines by 2.7% if they implement scale-correcting subsidies without reciprocity by trading partners. Aversion to these consequences, we argue, may have spurred a global race to the bottom in industrial policy implementation. To escape immiserizing growth, governments either avoid corrective policies or pair them with hidden trade barriers that breach shallow trade cooperation.The Chinese government, for instance, pairs its domestic subsidies with hidden export taxes. These hidden barriers are applied via partial value-added tax rebates and are designed to restore China’s ToT (Garred (2018)).

Third, deep agreements can remedy the race to the bottom and deliver welfare gains that are more transformative than any unilateral intervention. To offer some perspective, corrective industrial policies coordinated via a deep agreement can elevate the average country’s real GDP by 3.2%. These welfare gains rival the already-realized gains from shallow agreements for most countries. They, moreover, exceed any welfare gains achievable through unilateral trade or industrial policy interventions—even not considering that unilateralism often backfires in the form of retaliation by trading partners.

Related Literature—Our theory relates to an emerging literature on optimal policy in distorted open economies. In a concurrent paper, Bartelme et al. (2019) characterize the first-best optimal policy for a small open economy in a multi-sector Ricardian model with Marshallian externalities. Relatedly, Haaland and Venables (2016) characterize optimal policy for a small open economy in two-by-two Krugman and Melitz models.Demidova and Rodriguez-Clare (2009) and Felbermayr, Jung and Larch (2013) characterize optimal tariffs in a single industry Melitz-Pareto model. The single industry assumption ensures that markets are efficient (Dhingra and Morrow (2019)) and import and export taxes are equivalent (the Lerner symmetry). So, the unilaterally first-best can be reached with import tariffs alone. Costinot, Rodríguez-Clare and Werning (2016) examine optimal policy in the single industry Melitz-Pareto model from a different lens, characterizing optimal firm-level taxes. Beyond optimal policy, Campolmi, Fadinger and Forlati (2018) employ a two-sector Melitz-Pareto model to elucidate the trade-offs facing countries that join shallow and deep trade agreements.Other papers have also used new or quantitative trade models to analyze piecemeal policy reforms in distorted economies or optimal policy in non-distorted economies—e.g., Costinot and Rodríguez-Clare (2014); Campolmi, Fadinger and Forlati (2014); Costinot et al. (2015); Bagwell and Lee (2018); Caliendo et al. (2015); Demidova (2017); Beshkar and Lashkaripour (2019, 2020). Our analysis of second-best trade policies speaks to an older literature emphasizing the firm-delocation rationale for trade restrictions (e.g., Venables (1987); Ossa (2011)), and supplements Bagwell and Staiger’s (2001; 2004) result about the role of trade agreements in distorted economies. We also build on Kucheryavyy, Lyn and Rodríguez-Clare (2023) to establish isomorphism between our baseline model and other workhorse models in the literature. Our quantitative examination of trade and industrial policy connects to two strands of literature. First, a mature line of research measuring the ex-post consequences of tariff cuts (Costinot and Rodríguez-Clare (2014); Caliendo and Parro (2015); Ossa (2014, 2016); Spearot (2016)). Second, a growing literature examining the ex-ante consequences of optimal policy. Ossa (2014), most notably, quantifies the consequences of cooperative and non-cooperative import tariffs in a multi-industry Krugman model with restricted entry. Lastly, our work relates to a vibrant literature examining the impacts of exogenous trade shocks in distorted economies (e.g., De Blas and Russ (2015); Edmond, Midrigan and Xu (2015); Baqaee and Farhi (2019)).

We contribute to the calculus of optimal policy in open economies by developing a new dual technique for optimal policy derivation in general equilibrium quantitative trade models with many countries, increasing returns-to-scale production technologies, and input-output linkages. Our approach has applications beyond those considered in this paper. Lashkaripour (2021), for instance, adopts a special case of this technique to characterize Nash tariffs in a monopolistic competition model with restricted entry.Lashkaripour (2021) examines the cost of non-cooperative import restrictions when governments simultaneously apply their 3rd-best optimal import tariffs. To expedite the computational process, Lashkaripour (2021) uses analytic formulas for Nash tariffs, which correspond to a special of our Theorem 3.Farrokhi and Lashkaripour (2021) extend this technique to analyze optimal carbon pricing under international climate externalities.

Lastly, our paper supplements the broader quantitative trade literature by developing an estimation technique that separately identifies the scale elasticity from the trade elasticity in certain environments. Our indirect approach to scale elasticity estimation complements the direct method concurrently proposed by Bartelme et al. (2019). The main limitation of our indirect approach is that it cannot detect scale externalities unrelated to love-for-variety, as it does not directly leverage scale-related moments. Despite this limitation, our approach has two useful properties for policy evaluation. First, it separately identifies the trade elasticity from the scale elasticity, provided that scale economies arise from love-for-variety, which is valuable since the covariance between these elasticities regulates policy outcomes. Second, our approach is robust to the presence of quasi-fixed production inputs, enabling us to isolate scale effects that impair allocative efficiency from fixed-input-driven diseconomies of scale.

1 Theoretical Framework

Our baseline model is a generalized multi-industry, multi-country Krugman model with semi-parametric preferences. In Section 4 we show that our theory readily applies to alternative models featuring firm-selection à la Melitz–Chaney and external economies of scale à la Kucheryavyy, Lyn and Rodríguez-Clare (2023). We also extend our theory later to accommodate arbitrary input-output networks and political economy pressures.

We consider a world economy consisting of multiple countries and industries. Countries are indexed by of \(i,j,n\in \mathbb {C}\). Industries are indexed by \(g,k\in \mathbb {K}\). Industries can differ in fundamentals such as the degree of scale economies or trade elasticity. Each country \(i\in \mathbb {C}\) is populated by \(L_{i}\) individuals who supply one unit of labor inelasticity. Labor is the sole primary factor of production in each economy. Workers cannot relocate between countries but are perfectly mobile across industries within a country, and are paid a country-wide wage, \(w_{i}\).

1.1 Preferences

Each good in our model is indexed by a triplet, which signifies its location of production (origin), it

location of final consumption (destination), and the industry under which the good is classified. To give an

example: Good “\(ji,k\) ” denotes a good corresponding to origin country \(j\)–destination country \(i\)–industry \(k\).

Cross-Industry Demand.\(\quad\) The representative consumer in country \(i\in \mathbb {C}\) faces a vector of industry-level consumer

price indexes \(\mathbf{\tilde {\mathbf{P}}}_{i}=\{\tilde {P}_{i,k}\}\), where index \(\tilde {P}_{i,k}\equiv \tilde {P}_{i,k}(\tilde {P}_{1i,k},...,\tilde {P}_{Ni,k})\) aggregates over industry \(k\) goods sourced from various origins. The consumer

chooses their demand for industry-level bundles \(\mathbf{Q}_{i}\equiv \{Q_{i,k}\}\) to maximize a non-parametric utility function

subject to a budget constraint. This choice yields an indirect utility, which is a function of the

consumer’s income, \(Y_{i}\), and the vector of industry-level “consumer” price indexes in market \(i\), \(\tilde {\mathbf{P}}_{i}\):

Throughout this paper, the tilde notation on price is used to distinguish between “consumer” and

“producer” prices. The former includes taxes, whereas the latter does not. this problem yields an

industry-level Marshallian demand function, which we denote by \(Q_{i,k}=\mathcal {D}_{i,k}\left (Y_{i},\tilde {\mathbf{P}}_{i}\right )\). This function tracks how (given prices

and total income) consumers allocate their expenditure across industries. A special case of our

general cross-industry demand function is the Cobb-Douglas case, wherein \(U_{i}(\mathbf{Q}_{i})=\prod _{k\in \mathbb {K}}Q_{i,k}^{e_{i,k}}\) implying that \(Q_{i,k}=e_{i,k}Y_{i}/\tilde {P}_{i,k}\).

Within-Industry Demand.\(\quad\) Each industry-level bundle aggregates over various origin-specific composite

varieties: \(Q_{i,k}\equiv Q_{i,k}(Q_{1i,k},...,Q_{Ni,k})\). Each origin-specific composite variety, itself, aggregates over multiple firm-level

varieties: \(Q_{ji,k}\equiv Q_{ji,k}(\mathbf{q}_{ji,k})\), where \(\mathbf{q}_{ji,k}=\left \{ q_{ji,k}\left (\omega \right )\right \} _{\omega \in \Omega _{j,k}}\) is a vector with each element \(q_{ji,k}\left (\omega \right )\) denoting the quantity consumed of firm \(\omega\)’s

output.\(\Omega _{j,k}\) denotes the set of all firms operating in origin \(j\)–industry \(k\). In our baseline model, firms do not incur a fixed exporting cost, so each firm in \(\Omega _{j,k}\) serves market \(i\). We relax this assumption in Section 4.

We assume that the within-industry utility aggregator has a nested-CES structure, which enables us to

abstract from variable markups and direct our attention to the scale-driven and profit-shifting effects of

policy.

Assumption (A1).\(\,\) The within-industry utility aggregator is nested-CES. In particular,

with \(\gamma _{k}\geq \sigma _{k}>1\) and \(\varphi _{ji,k}(\omega )>0\) corresponding to a constant variety-specific taste shifter.

Based on (A1), the demand for the composite national-level variety \(ji,k\) (origin country \(j\)–destination country \(i\)–industry \(k\)) is given by

where \(\tilde {P}_{ji,k}\) and \(\tilde {P}_{i,k}\) respectively denote the origin-specific and industry-level CES price indexes.Namely, \(\tilde {P}_{ji,k}=\left (\sum _{\omega \in \Omega _{ji,k}}\varphi _{ji,k}(\omega )\tilde {p}_{ji,k}\left (\omega \right )^{1-\gamma _{k}}\right )^{\frac {1}{1-\gamma _{k}}}\) and \(\tilde {P}_{i,k}=\left (\sum _{j\in \mathbb {C}}\tilde {P}_{ji,k}^{1-\sigma _{k}}\right )^{\frac {1}{1-\sigma _{k}}}\). Recall that \(Q_{i,k}\) denotes industry-level demand, which is given by \(Q_{i,k}=\mathcal {D}_{i,k}\left (Y_{i},\tilde {\mathbf{P}}_{i}\right )\). The demand facing individual firms from country \(j\) is, accordingly, given by

Importantly, the above parameterization of demand allows for the

firm-level and national-level degrees of market power to diverge. \(\gamma _{k}\) governs the degree of firm-level market

power and love-for-variety, while \(\sigma _{k}\) governs the degree of national-level market power in industry \(k\).

Elasticity of Demand Facing National-Level Varieties.\(\quad\) Following Equation 1, the demand for aggregate

variety \(ji,k\) is a function of total income in market \(i\), \(Y_{i}\), and the entire vector of origin\(\times\) industry-specific

consumer price indexes in that market: Namely, \(Q_{ji,k}=\mathcal {D}_{ji,k}\left (Y_{i},\tilde {\mathbf{P}}_{i}\right )\). To keep track of changes in demand, we define

the elasticity of demand for national-level variety \(ji,k\) w.r.t. to the price of variety \(ni,g\) as follows:

Under Cobb-Douglas preferences (i.e., zero cross-substitutability between industries), the national-level demand elasticities are fully determined by the upper-tier CES parameter \(\sigma _{k}\) and national-level expenditure shares. Specifically, \(\varepsilon _{ji,k}^{\jmath i,g}=0\) if \(g\neq k\), while

where \(\lambda _{ji,k}\equiv \tilde {P}_{ji,k}Q_{ji,k}/\sum _{\jmath }\tilde {P}_{\jmath i,k}Q_{\jmath i,k}\) denotes the (within-industry) share of expenditure on \(ji,k\). In the presence of cross-substitutability between industries, the demand elasticity will feature an additional term that accounts for cross-industry demand effects.

In our setup, optimal policy internalizes the entire matrix of own- and cross-demand elasticities. To

present our optimal policy formulas concisely, we use the following matrix notation to track the elasticity

of demand w.r.t. goods sourced from various origins and industries.

Definition (D1).\(\,\) Let \(K=\left |\mathbb {K}\right |\) denote the number of industries. The \(K\times K\) matrix \(\mathbf{E}_{ji}^{(ni)}\) describes the elasticity of demand

for origin \(j\in \mathbb {C}\) goods w.r.t. the price of origin \(n\in \mathbb {C}\) goods in market \(i\):

To simplify the notation, we use \(\mathbf{E}_{ji}\sim \mathbf{E}_{ji}^{(ji)}\) to denote the elasticity of origin \(j\) goods w.r.t. origin \(j\) prices, and use the \(K\times (N-1)K\) matrix, \(\mathbf{E}_{ji}^{(-ii)}=\left [\mathbf{E}_{ji}^{(ni)}\right ]_{n\neq i}\), to summarize the elasticity of demand for origin \(j\) goods w.r.t. price of all import varieties in market \(i\) (i.e., all varieties source from any origin \(n\neq i\)). Important for our analysis, \(\mathbf{E}_{ji}\) is an invertible matrix—the proof of which is provided in the online appendix using the primitive properties of Marshallian demand.

1.2 Production and Firms

Each economy \(i\in \mathbb {C}\) is populated with a mass \(M_{i,k}=\left |\Omega _{i,k}\right |\) of single-product firms in industry \(k\in \mathbb {K}\) that compete under monopolistic competition. Labor is the only factor of production. Firm entry into industry \(k\) is either free or restricted. Under restricted entry, \(M_{i,k}=\overline {M}_{i,k}\) is invariant to policy. Under free entry, a pool of ex-ante identical firms can pay an entry cost \(w_{i}f_{k}^{e}\) to serve industry \(k\) from origin \(i\). After paying the entry cost, each firm \(\omega \in \Omega _{i,k}\) draws a productivity \(z(\omega )\geq 1\) from distribution \(G_{i,k}\left (z\right )\), and faces a marginal cost \(\tau _{ij,k}w_{i}/z\left (\omega \right )\) for producing and delivering goods to destination \(j\in \mathbb {C}\), where \(\tau _{ij,k}\) denotes a flat iceberg transport cost. Collecting these assumptions, the “producer” price index of composite good \(ij,k\) (which aggregates over firm-level varieties associated with origin \(i\)–destination \(j\)–industry \(k\)) is

where \(\bar {a}_{i,k}\equiv \left [\int _{1}^{\infty }z^{\gamma _{k}-1}dG_{i,k}(z)\right ]^{\frac {1}{1-\gamma _{k}}}\) denotes the average unit labor cost in origin \(i\).Notice that \(\bar {a}_{i,k}\) is constant in our baseline model. This is no longer true in the Melitz (2003) extension of oue model explored in Section 4, in which firms incur a fixed cost to serve individual markets. Following Kucheryavyy, Lyn and Rodríguez-Clare (2023), we refer to \(\frac {1}{\gamma _{k}-1}=-\frac {\partial \ln P_{ij,k}}{\partial \ln M_{i,k}}\) as the industry-level scale elasticity:

Considering Equation 3, \(\mu _{k}\) represents both \((a)\) the constant firm-level markup in industry \(k\) (i.e., \(1+\mu _{k}=\frac {\gamma _{k}}{\gamma _{k}-1}\)), and \((b)\) the

elasticity by which (variety-adjusted) TFP increases with industry-level employment \(L_{i,k}\) (noting that

\(L_{i,k}\propto M_{i,k}\)).With free entry and constant markups, it follows immediately that \(L_{i,k}=\bar {c}_{i,k}M_{i,k}\) where \(\bar {c}_{i,k}\) is a constant. The

equivalence between markup and scale elasticity is not a universal property but a specific feature of our

baseline Krugman model. We take advantage of this equivalence to simplify notation, but it is not

essential for the theoretical results that follow. As shown in Section 4, our analytical formulas for

optimal policy extend to alternative models where the scale elasticity and markup levels diverge.

Expressing Producer Prices in terms of Profit-Adjusted Wages.\(\quad\) Our optimal policy framework reveals a

tight connection between the restricted and free entry cases—even though misallocation stems from

markup distortions in the former and scale distortions in the latter. To illustrate this connection and

integrate optimal policy results for the two cases, we specify producer prices as a function of

profit-adjusted wage rates. The idea is that net profits (if any) are rebated back to workers. The

profit-adjusted wage rate in country \(i\) is defined as

where \(\overline {\mu }_{i}\) denotes economy \(i\)’s average profit margin across all industries. Namely,

Under free entry, profits are drawn to zero, resulting in \(\overline {\mu }_{i}=0\). Under restricted entry, the average profit margin is positive and depends on the industrial composition of country \(i\)’s output—with a higher \(\overline {\mu }_{i}\) reflecting more sales in high-markup (high-\(\mu\)) industries. Appealing to our definitions for \(\grave {w}_{i}\) and \(\mu _{k}\), we can reformulate Equation 3 to express producer prices as a function of profit-adjusted wages:

In the above formulation, \(\varrho _{ij,k}\equiv \left (1+\mu _{k}\right )\tau _{ij,k}\bar {a}_{i,k}^{\frac {1}{1+\mu _{k}}}\left (\mu _{k}/f_{k}^{e}\right )^{\frac {-\mu _{k}}{1+\mu _{k}}}\) and \(\varrho '_{ij,k}\equiv \tau _{ij,k}\bar {a}_{i,k}\bar {M}_{i,k}^{-\mu _{k}}\) are constant price shifters; and \(\sum _{j\in \mathbb {C}}\left [\tau _{ij,k}Q_{ij,k}\right ]\) denotes origin \(i\)–industry \(k\)’s gross output.Under free entry, the total cost of entry must equal gross profits across all markets. I particular,\[w_{i}f_{k}^{e}M_{i,k}=\sum _{j\in \mathbb {C}}\left [\frac {\mu _{k}}{1+\mu _{k}}P_{ij,k}Q_{ij,k}\right ]\qquad \qquad \left (\text{Free Entry Condition}\right ).\] Replacing \(P_{ij,k}\) in the above equation with 3 yields \(M_{i,k}=\left (\frac {\mu _{k}}{f_{k}^{e}}\sum _{j}\left [\bar {a}_{ij,k}Q_{ij,k}\right ]\right )^{\frac {1}{1+\mu _{k}}}\). Equation 5, then, follows from plugging the expression for \(M_{i,k}\) back into Equation 3. As we explain shortly, the above formulation of producer prices is useful for tracking the terms-of-trade gains from policy in open economies. These gains require a contraction of producer prices in the rest of world, which can occur through alterations to production scale,\(\sum _{j\in \mathbb {C}}\left [\tau _{ij,k}Q_{ij,k}\right ]\), under free entry or average profit margins, \(\overline {\mu }_{i}\), under restrict entry.

1.3 The Instruments of Policy

The government in country \(i\) has is afforded a complete set of revenue-raising trade and domestic policy instruments; namely,

- 1.

- import tax, \(t_{ji,k}\), applied to all goods imported from origin \(j\neq i\) in industry \(k\);

- 2.

- export subsidy, \(x_{ij,k}\), applied to all goods sold to market \(j\neq i\) in industry \(k\);

- 3.

- industrial subsidy, \(s_{i,k}\), applied to industry \(k\)’s output irrespective of where it is sold.

Our specification of policy is quite flexible as it accommodates import subsidies or export taxes (\(-1\leq t<0\) or \(-1\leq x<0\)) as well as production taxes (\(-1\leq s<0\)). We disregard consumption taxes as they are redundant given the availability of the other tax instruments (see the online appendix). There is a simple intuition behind this redundancy: Country \(i\in \mathbb {C}\) has access to \(2(N-1)+2\) different tax instruments in each industry (where \(N\equiv \left |\mathbb {C}\right |\) denotes the number of countries). These \(2(N-1)+2\) tax instruments can directly manipulate \(2(N-1)+1\) consumer price indexes: \(N-1\) export prices, \(N-1\) import prices, and one price associated with the domestically-produced and consumed variety (namely, \(\tilde {P}_{ii,k}\)). So, by construction, one of the \(2(N-1)+2\) tax instruments in each industry is redundant. Here, we treat the industry-level consumption tax as a redundant instrument.With more than two countries (\(N>2)\), Country \(i\) has access to \(2(N-1)+2\) instruments per industry. These instruments can manipulate \(2(N-1)+1\) price variables, which implies the same redundancy.

The above tax instruments create a wedge between consumer price indexes, \(\{\tilde {P}_{ji,k}\}\) and producer price indexes, \(\{P_{ji,k}\}\), as follows:

These tax instruments also generate/exhaust revenue for the tax-imposing country. The combination of all taxes imposed by country \(i\in \mathbb {C}\) produce a tax revenue equal to

Tax revenues are rebated to the consumers in a lump-sum fashion. After we account for tax revenues, total income in country \(i\) equals the sum of profit-adjusted wage payments, \(\grave {w}_{i}L_{i}=(1+\overline {\mu }_{i})w_{i}L_{i}\), and tax revenues. Namely, \(Y_{i}=\grave {w}_{i}L_{i}+\mathcal {R}_{i}\), where \(\mathcal {R}_{i}\) can be positive or negative depending on whether country \(i\)’s policy consists of net taxes or subsidies.

1.4 General Equilibrium

For convenience, we refer to profit-adjusted wages as just wages going forward, using \(\mathbf{w}\equiv \{\grave {w}_{i}\}\) to denote the global

vector of wages. We also assume throughout the paper that the underlying parameters of the model

are such that the necessary and sufficient conditions for the uniqueness of equilibrium are

satisfied.Following Kucheryavyy, Lyn and Rodríguez-Clare (2023), this assumption holds in the two country case if \(\gamma _{k}\geq \sigma _{k}\) and holds otherwise if trade costs are sufficiently small.

To present our theory, we express all equilibrium outcomes (except wages) as an explicit function of global

taxes (\(\mathbf{x}\), \(\mathbf{t}\), and \(\mathbf{s}\)) and wages \(\mathbf{w}\), with the understanding that \(\mathbf{w}\) is itself an equilibrium outcome. As detailed in

the online appendix, this formulation derives from solving a system that imposes all equilibrium

conditions aside from the labor market clearing conditions. For future reference, we outline this

formulation of equilibrium variables below.

Notation.\(\,\) For a given vector of taxes and wages \(\mathbf{T}=(\mathbf{t},\mathbf{x},\mathbf{s};\mathbf{w})\), equilibrium outcomes \(Y_{i}(\mathbf{T})\), \(P_{ji,k}(\mathbf{T})\), \(\tilde {P}_{ji,k}(\mathbf{T})\), \(Q_{ji,k}(\mathbf{T})\) are determined such that \((i)\)

producer prices are characterized by Equation 5; \((ii)\) consumer prices are given by Equation 6; \((iii)\)

industry-level consumption choices are a solution to with demand for national-level varieties, \(Q_{ji,k}\),

given by Equation 1; and \((iv)\) total income (which dictates total expenditure by country \(i\)) equals

profit-adjusted wage payments plus tax revenues:

where tax revenues \(\mathcal {R}_{i}(\mathbf{T})\) are described by Equation .

Considering the above formulation of equilibrium variables, welfare, too, can be expressed as an explicit function of taxes and wages, \(\mathbf{T}=(\mathbf{t},\mathbf{x},\mathbf{s};\mathbf{w})\). Namely,

Since \(\mathbf{w}\) is itself an equilibrium outcome, vector \(\mathbf{T}=(\mathbf{t},\mathbf{x},\mathbf{s};\mathbf{w})\) is feasible

iff \(\mathbf{w}\) is the equilibrium wage consistent with \(\mathbf{t}\), \(\mathbf{x}\), and \(\mathbf{s}\). Accordingly, our objective in this paper is to study

problems where the government in \(i\) choses \(\mathbf{T}=(\mathbf{t},\mathbf{x},\mathbf{s};\mathbf{w})\) to maximize \(W_{i}\left (\mathbf{T}\right )\) subject to the noted feasibility constraint, which

is formally defined below.

Definition (D2).\(\,\) The set of feasible policy–wage vectors, \(\mathbb {F}\), consists of any vector \(\mathbf{T}=(\mathbf{t},\mathbf{x},\mathbf{s};\mathbf{w})\) where \(\mathbf{w}\) satisfies the

labor market clearing condition in every country, given \(\mathbf{t}\), \(\mathbf{x}\), and \(\mathbf{s}\):

There is a basic reason for why we formulate equilibrium outcomes as a function of \(\mathbf{T}=(\mathbf{t},\mathbf{x},\mathbf{s};\mathbf{w})\) instead of just \((\mathbf{t},\mathbf{x},\mathbf{s})\). This choice of formulation allows us to articulate an important intermediate result regarding tax neutrality. This result, which is stated below, simplifies our theoretical derivation of optimal policy to a great degree.

Lemma 1 [Tax Neutrality]For any \(a\) and \(\tilde {a}\in \mathbb {R}_{+}\) \((i)\) if \(\mathbf{T}=(\boldsymbol {1}+\mathbf{t}_{i},\mathbf{t}_{-i}\),\(\boldsymbol {1}+\mathbf{x}_{i},\mathbf{x}_{-i},\boldsymbol {1}+\mathbf{s}_{i},\mathbf{s}_{-i};\grave {w}_{i},\mathbf{w}_{-i})\in \mathbb {F}\), then \(\mathbf{T}'=(a(\boldsymbol {1}+\mathbf{t}_{i}),\mathbf{t}_{-i},a(\boldsymbol {1}+\mathbf{x}_{i}),\mathbf{x}_{-i},\frac {1}{\tilde {a}}(\boldsymbol {1}+\mathbf{s}_{i}),\mathbf{s}_{-i};\frac {a}{\tilde {a}}\grave {w}_{i},\mathbf{w}_{-i})\in \mathbb {F}\). Moreover, \((ii)\) welfare is preserved under \(\mathbf{T}\) and \(\mathbf{T}'\): \(W_{n}(\mathbf{T})=W_{n}(\mathbf{T}')\) for all \(n\in \mathbb {C}\).

The above lemma is proven in the online appendix, and connects two fundamental tax neutrality principles: The Lerner symmetry (Lerner (1936); Costinot and Werning (2019)) and the welfare-neutrality of uniform subsidies or markups (Lerner (1934); Samuelson (1948)). Importantly, Lemma 1 implies that there are multiple optimal tax combinations for each country \(i\)—a result that simplifies our forthcoming task of characterizing optimal policy. To give some detail: The contribution of general equilibrium wage and income effects to the optimal tax schedule is often summarized by aggregate tax-shifters that are industry-blind. The neutrality established by Lemma 1, simplifies the task of handling of these aggregate terms.

| Variable | Description |

| \(\tilde {P}_{ji,k}\) | Consumer price index (origin \(j\)–destination \(i\)–industry \(k\)) |

| \(P_{ji,k}\) | Producer price index (origin \(j\)–destination \(i\)–industry \(k\)) |

| \(Y_{i}\) | Total income in country \(i\) |

| \(\mathcal {R}_{i}\) | Total tax revenue in country \(i\) (the corresponding equation) |

| \(w_{i}\) and \(\grave {w}_{i}\) | pure and profit-adjusted wage rates in country \(i\): \(\grave {w}_{i}=(1+\overline {\mu }_{i})w_{i}\) |

| \(x_{ji,k}\) | Export subsidy applied to good \(ji,k\) (if \(j\neq i\)) |

| \(t_{ji,k}\) | Import tax applied on good \(ji,k\) (if \(j\neq i\)) |

| \(s_{i,k}\) | Industrial subsidy applied to all goods from origin \(i\)–industry \(k\) |

| \(\lambda _{ji,k}\) | Within-industry expenditure share (good \(ji,k\)): \(\tilde {P}_{ji,k}Q_{ji,k}/\sum _{\jmath }\tilde {P}_{\jmath i,k}Q_{\jmath i,k}\) |

| \(r_{ji,k}\) | Within-industry sales share (good \(ji,k\)): \(P_{ji,k}Q_{ji,k}/\sum _{\iota }P_{j\iota,k}Q_{j\iota,k}\) |

| \(e_{i,k}\) | Industry-level expenditure share (destination \(i\)–industry \(k\)) |

| \(\rho _{i,k}\) | Industry-level sales share (origin \(i\)–industry \(k\)) |

| \(\mu _{k}\) | industry-level markup ˜ industry-level scale elasticity |

| \(\overline {\mu }_{i}\) | Average profit margin in origin \(i\) (Equation 4) |

| \(\sigma _{k}\) | Cross-national CES parameter ˜ (1 + trade elasticity) |

| \(\varepsilon _{ji,k}^{(ni,g)}\) | Elasticity of demand for good \(ji,k\) w.r.t. the price of \(ni,g\) |

| \(\omega _{ji,k}\) | Inverse of good \(ji,k\)’s supply elasticity (the corresponding equation) |

2 Sufficient Statistics Formulas for Optimal Policy

This section derives sufficient statistics formulas for optimal trade and industrial policies. These formulas are later employed to quantify the ex-ante gains from policy among many countries. Before proceeding to the derivation, let us review the two rationales for policy intervention in our setup. A non-cooperative, welfare-maximizing government seeks to \((i)\) restrict trade and reap unexploited terms-of-trade (ToT) gains vis-à-vis the rest of the world, and \((ii)\) correct misallocation in the domestic economy. Misallocation, notice, stems from the cross-industry heterogeneity in markups or scale elasticities, leading to inefficiently low output in high-profit or high-returns-to-scale (high-\(\mu\)) industries. A crucial difference between these policy objectives is that ToT manipulation is inefficient from a global standpoint, as it distorts international prices to transfer surplus from the rest of the world to the tax-imposing country.

2.1 Efficient Policy from a Global Standpoint

As a useful benchmark, we first characterize the efficient policy from a global standpoint. Efficient policies, by definition, are the solution to a central planner’s problem that maximizes global welfare via taxes and lump-sum international transfers. Let \(\delta _{i}\) denote the Pareto weight assigned to country \(i\) in the planner’s objective function. The globally efficient policy solves the following planning problem subject to the availability of lump-sum transfers:

Keep in mind that the above problem affords the planner enough instruments to obtain their first-best. Good-specific taxes allow the planner to restore allocative efficiency, while lump-sum transfers allow her to redistribute inter-nationally based on the Pareto weights, \(\delta _{i}\). This point is expanded on in the online appendix, were it is shown that the efficient tax policy involves zero trade taxes and Pigouvian subsidies that restore marginal-cost-pricing globally:To be specific, the implementation of the efficient allocation involves the above taxes plus lump-sum international transfers based on Pareto weights. The logic is that the planner maximizes global output by restoring marginal-cost pricing and redistributes the corresponding income gains between countries via efficient transfers. Absent transfers, implementing \(\left \{ \mathbf{t}^{\star },\mathbf{x}^{\star },\mathbf{s}^{\star }\right \}\) would deliver a Kaldor-Hicks improvement (Kaldor (1939); Hicks (1939)), but not necessarily a Pareto improvement relative to Laissez-faire—see online Appendix for more details.

The above characterization applies to both the free and restricted entry cases—with the understanding that \(\mu _{k}\) assumes different interpretations in each case. Appealing to this result, the online appendix establishes a basic point about international cooperation: Welfare-maximizing governments will settle on the efficient policy only if they are unable to influence consumer/producer prices in the rest of the world. Otherwise, they will defect to take advantage of terms-of-trade (ToT) gains. This result indicates that the pursuit of ToT gains is the sole reason welfare-maximizing governments deviate from efficient policy choices—at least when they are afforded sufficient policy instruments.This need not be true if government are prohibited from using domestic taxes and afforded only import tax instruments. Following Venables (1987) and Ossa (2011), welfare-maximizing governments will erect tariffs in that case, even if they perceive world prices as invariant to their policy choice. By doing so, they improve allocative efficiency in the domestic economy but impose a negative firm-delocation externality on the rest of the world. This result echos the argument in Bagwell and Staiger (2001, 2004), generalizing it to settings with many countries and differentiated industries.

In the next section, we characterize the unilaterally optimal policy of non-cooperative governments. This exercise elucidates two issues. First, it determines how governments deviate from the cooperative policy choice when ToT considerations are taken into account. Second, it clarifies how governments approach industrial policy when they view 1st-best Pigouvian subsidies as politically infeasible. Once we settle these two issues, we argue that the implementation of globally efficient policies requires both a “shallow agreement” to discipline trade policy choices and a “deep agreement” to coordinate industrial policy implementation.

2.2 Unilaterally Optimal Policy Choices

2.2.1 First-Best: Unilaterally Optimal Trade and Domestic Policies

We now characterize a non-cooperative country’s unilaterally optimal policy. We consider cases where a non-cooperative country \(i\in \mathbb {C}\) selects taxes, \(\mathbf{t}_{i}\equiv \{t_{ji,k}\}\), \(\mathbf{x}_{i}\equiv \{x_{ij,k}\}\), and \(\mathbf{s}_{i}\equiv \{s_{i,k}\}\), taking policy choices elsewhere as given. Countries in the rest of the world are passive in their use of taxes but actively maintain internal cooperation.One aspect of internal cooperation requires further clarification: Country \(i\)’s policy could, in principle, disrupt the balance of market access concessions in the rest of the world, leading to a deterioration of one cooperative country’s ToT relative to another. Cooperation within the rest of the world entails that these extraterritorial ToT effects be neutralized via buffers that preserve \(w_{n}/w_{j}\) for all \(n,j\neq i\)—see online Appendix for further details. We begin with the unilaterally first-best case where the government in \(i\) is afforded all possible tax instruments. The first-best unilaterally optimal policy solves the following problem:Given that the rest of the world is passive in their use of taxes (i.e.,\(\mathbf{t}_{-i}=\mathbf{x}_{-i}=\mathbf{s}_{-i}=\mathbf{0}\)), we condense the notation by specifying equilibrium variables as a function of only \(\left (\mathbf{t}_{i},\mathbf{x}_{i},\mathbf{s}_{i},\mathbf{w}\right )\).

We analytically solve Problem (P1) under both the restricted and free entry cases. We perceive the

restricted entry case to be a more appropriate benchmark if governments are concerned with short-run

gains from policy. The free entry case, on the other hand, is more relevant if governments are concerned

with long-run gains. These two cases exhibit an important difference: Producer prices respond

differently to contractions in export supply under restricted and free entry—as we elaborate next.

Conditional Export Supply Elasticity.\(\quad\) The terms-of-trade gains from policy, in our framework, channel

through changes in the price of imported and exported goods. The government in \(i\in \mathbb {C}\) cannot directly dictate

the producer price of say good, \(ji,k\), that is imported from origin \(j\neq i\). Instead, it can deflate its producer price (\(P_{ji,k}\))

indirectly by contracting or expanding its export supply (\(Q_{ji,k}\)). The contraction in \(Q_{ji,k}\) also affects the producer

price of goods supplied by other locations through general equilibrium linkages. Our theory indicates that,

for optimal policy analysis, the conditional inverse export supply elasticity is sufficient to track these

effects. To present this elasticity, let \(\tilde {\mathbb {P}}_{i}\) contain the consumer price of all goods either produced by

or consumed in country \(i\). These are prices that country \(i\)’s government can fully control via

taxes. We define the conditional inverse export supply elasticity of good \(ji,k\) as

where \(r_{ni,g}\equiv \frac {P_{ni,g}Q_{ni,g}}{\sum _{\iota }P_{n\iota,g}Q_{n\iota,g}}\) and \(\rho _{n,g}\equiv \frac {\sum _{\iota }P_{n\iota,g}Q_{\iota,g}}{\sum _{\iota,s}P_{n\iota,s}Q_{\iota,s}}\) respectively denote the good-specific and industry-wide sales shares associated with origin \(n\). Notice, \(\omega _{ji,k}\) is a conditional elasticity that describes how the producer prices linked to economy \(i\) respond to a change in \(Q_{ji,k}\), holding \(\tilde {\mathbb {P}}_{i}\) and the entire vector of wage and income levels constant. This elasticity encapsulates different economic forces under free and restricted entry, as we detail next.

Under restricted entry, producer prices from origin \(j\in \mathbb {C}\) are fully determined by the (profit-adjusted) wage rate, \(\grave {w}_{j}\), and the aggregate profit margin, \(\overline {\mu }_{j}\) (see Equation 5). Policy, thus, has two distinct effects on producer prices under restricted entry: One effect that channels through wages, \(\mathbf{w}\); and another that channels through aggregate profit margins. To explain the latter, hold \(\mathbf{w}\) constant: contracting the export supply of good \(ji,k\) with taxes will alter all producer prices associated with origin \(j\) through a change in origin \(j\)’s aggregate profit margin, \(\overline {\mu }_{j}\). The change in \(\overline {\mu }_{j}\) derives from the fact that industries have differential markup margins, and that taxing good \(ji,k\) alters the industrial composition of output in origin \(j\in \mathbb {C}\).

Under free entry, producer prices from origin \(j\in \mathbb {C}\) are determined by the wage rate, \(\grave {w}_{j}\), and the origin \(j\)–industry \(k\)-specific scale of production. So, aside from wage-related effects, policy has a second effect on producer prices that channels through industry-level scale economies. To elaborate, consider an import tax on good \(ji,k\) (origin \(j\)–destination \(i\)–industry \(k\)). Such a tax contracts the supply of \(ji,k\) and the scale of production in origin \(j\)–industry \(k\). Given Equation 5, this contraction in scale increases the entire vector of producer price indexes associated with origin \(j\)–industry \(k\)—all through additional firm entry.

In both cases, \(\omega _{ji,k}\) describes how expanding or contracting good \(ji,k\)’s export supply impacts country \(i\)’s terms-of-trade via either profit-shifting or industry-level scale economies. Importantly, \(\omega _{ji,k}\) can be characterized (to a first-order approximation) as a simple function of sales shares, scale elasticities, and Marshallian demand elasticities (see the online appendix):The above approximation derives from Wu et al.’s (2013) first-order approximated inverse of a diagonally-dominant matrix. Figure () in online Appendix illustrates the precision of this approximation. The same appendix also presents an exact (approximation-free) formulation for \(\omega _{ji,k}\).

The

above formulation for \(\omega _{ji,k}\) is quite intuitive: Under restricted entry, \(\omega _{ji,k}\) governs the relationship between export

supply and the average markup paid on imports. Accordingly, \(\omega _{ji,k}\) is non-zero only when industries exhibit

differential markup levels. Otherwise, \(\omega _{ji,k}\) collapses to zero as the average markup (or profit margin) paid on

imports is constant and invariant to changes in export supply, i.e., \(\overline {\mu }_{j}=\mu _{k}=\mu\) \(\Longrightarrow\) \(\omega _{ji,k}=0\). Under free entry, \(\omega _{ji,k}\) regulates the

terms-of-trade gains from policy that channel through scale economies. Accordingly, in the limit where

industries operate based on constant-returns to scale, \(\omega _{ji,k}\) once again collapses to zero—namely, \(\lim _{\mu _{k}\rightarrow 0}\omega _{ji,k}=0\).

Three-Step Dual Approach to Characterizing Optimal Policy.\(\quad\) Our characterization of optimal policy

employs the dual approach and is presented in the online appendix. Below, we provide a verbal summary

of our approach, which involves three main steps.

First, we simplify Problem (P1) by reformulating it into a problem where country \(i\)’s government chooses the vector of prices \(\tilde {\mathbb {P}}_{i}=\left \{ \tilde {\mathbf{P}}_{ii},\tilde {\mathbf{P}}_{ji},\tilde {\mathbf{P}}_{ij}\right \}\) associated with its own economy. Country \(i\)’s optimal tax/subsidy schedule \(\mathbb {T}_{i}^{*}\equiv \left (\mathbf{t}_{i}^{*},\mathbf{x}_{i}^{*},\mathbf{s}_{i}^{*}\right )\) is then recovered as the wedge between the optimal price vector \(\mathbb {\tilde {P}}_{i}^{*}\) and producer prices.

Second, we derive the first-order conditions (F.O.C.) associated with country \(i\)’s reformulated optimal policy problem. We use two technical tricks to overcome the complications related to general equilibrium analysis: First, we use the envelope conditions associated with optimal demand choices to net out redundant behavioral responses. Second, we identify additional welfare neutrality conditions specific to Problem (P1). Most importantly, we observe that terms in the F.O.C.s that account for general equilibrium wage and income effects are redundant in the neighborhood of the optimum. That is, we could specify the F.O.C.s associated with (P1) as if wages were constant and Marshallian demand functions were income-inelastic.Farrokhi and Lashkaripour (2021) streamline the dual approach developed in this paper, extending our result about the welfare neutrality of wages and income effects to settings with arbitrary inter-national externalities.

Third, we combine the F.O.C.s and solve them as part of one system. In this process, we appeal to the tax neutrality result specified by Lemma 1 to eliminate redundant tax shifters, which are difficult to characterize. We then appeal to well-known properties of Marshallian demand functions (e.g., Cournot aggregation and homogeneity of degree zero) to establish that our system of F.O.C.s admits a unique solution.To be clear, it is possible that our model admits multiple optimal policy equilibria. Yet the optimal policy formulas are uniquely specified by Theorem 1 in each case. Together, these steps lead us to simple sufficient statistics formulas for unilaterally optimal policies, as summarized by the following theorem.We later combine the formulas specified by Theorem 1 with micro-estimated parameter values to quantify the ex-ante gains from policy. In online Appendix , we test the accuracy and speed of our formulas by performing 150 numerical simulations in which the underlying model parameters are repeatedly sampled from a uniform distribution. The theoretical policy predictions are then compared to those obtained from numerical optimization.

Theorem 1 Country \(i\)’s unilaterally optimal policy is unique up to two uniform tax shifters \(1+\bar {s}_{i}\) and \(1+\bar {t}_{i}\in \mathbb {R}_{+}\), and is implicitly given by

where \(\omega _{ji,k}\) denotes the good \(ji,k\)’s inverse supply elasticity as given by Equation 7, while \(\mathbf{E}_{ij}\sim \mathbf{E}_{ij}^{(ij)}\) and \(\mathbf{E}_{ij}^{(-ij)}\) denote matrixes of Marshallian demand elasticities as defined under (D1).\(\mathbf{E}_{ij}^{(-ij)}=\left [\mathbf{E}_{ij}^{(nj)}\right ]_{n\neq i}\) is a \(K\times (N-1)K\) matrix and \(\mathbf{1}\equiv \mathbf{1}_{(N-1)K\times 1}\) is a column vector of ones. Also, in the general case with asymmetric income elasticities of demand, \(\mathbf{E}_{ij}\) should be replace with \(\tilde {\mathbf{E}}_{ij}\equiv [\frac {e_{ij,g}}{e_{ij,k}}\varepsilon _{ij,g}^{(ij,k)}]_{g,k}\). Otherwise, the symmetry of the Slutsky matrix implies that \(\frac {e_{ij,g}}{e_{ij,k}}\varepsilon _{ij,g}^{(ij,k)}=\varepsilon _{ij,k}^{(ij,g)}\), which implies that \(\mathbf{E}_{ij}=\tilde {\mathbf{E}}_{ij}\).

The uniform tax shifters, \(\bar {s}_{i}\), and \(\bar {t}_{i}\) account for the multiplicity of optimal policy equilibria (as indicated

by Lemma 1). These shifters can be assigned any arbitrary value, provided that \(1+\bar {s}_{i}\) and \(1+\bar {t}_{i}\in \mathbb {R}_{+}\). For instance, if we

assign a sufficiently high value to \(\bar {t}_{i}\) and \(\bar {s}_{i}\), the optimal policy will involve import tariffs, export

subsidies, and industrial subsidies. Conversely, if we assign a sufficiently low value to \(\bar {t}_{i}\) and \(\bar {s}_{i}\), the

optimal policy will involve import subsidies, export taxes, and industrial production taxes.

Intuition Behind Optimal Tax Formulas.\(\quad\) Theorem 1 states that country \(i\)’s unilaterally optimal policy

consists of \((1)\) Pigouvian subsidies that restore marginal cost pricing in economy \(i\); \((2)\) import taxes/subsidies

that exploit country \(i\)’s collective import market power, delivering an optimal mark-down on the producer

price of imported goods \(P_{ji,k}\); and \((3)\) export taxes/subsidies that exploit country \(i\)’s collective export market

power, charging the optimal national-level mark-up on the consumer price of exported goods

\(\tilde {P}_{ij,k}\).Theorem 1 reveals that once scale/markup distortions are corrected via domestic subsidies, optimal trade taxes resemble those derived by Dixit and Norman (1980) in perfectly competitive, constant-returns to scale environments (see also Matsuyama (2008)). The main difference between our formula and Dixit and Norman (1980) is that our Theorem 1 equates the optimal tariff to a conditional elasticity, \(\omega _{ji,k}\), free of general equilibrium wage-and-income effects. These difficult-to-characterize general equilibrium effects, we prove, are redundant in the neighborhood of the optimum policy and can be disregarded. This specific feature of our optimal policy formulas makes them useful for quantitative analysis—as we demonstrate later in Section 6.

Theorem 1 has two additional implications worth highlighting. The first is that 1st-best optimal tariffs and export subsidies are misallocation-blind but not necessarily blind to the overall magnitude of scale economies. In particular, \(\mathbf{t}_{ji}^{*}\) and \(\mathbf{x}_{ij}^{*}\) are misallocation-blind in that allocative efficiency is restored exclusively via industrial subsidies under the 1st-best. At the same time, \(\mathbf{t}_{ji}^{*}\) and \(\mathbf{x}_{ij}^{*}\) are sensitive to scale economies because raising the average scale elasticity modifies \(\mathbf{t}_{ji}^{*}\) and \(\mathbf{x}_{ij}^{*}\) regardless of the underlying degree of misallocation.By the degree of misallocation, we mean the log welfare distance to the efficient frontier, \(\mathcal {L}_{i}\). In a closed economy with Cobb-Douglas-CES preferences, \(\mathcal {L}_{i}=\mathbb {E}_{\rho _{i}}\left [\mu \log \mu \right ]-\mathbb {E}_{\rho _{i}}\left [\mu \right ]\log \mathbb {E}_{\rho _{i}}\left [\mu \right ],\) where \(\mathbb {E}_{\rho _{i}}\left [\mu \right ]\) denotes to the sales-weighted average scale elasticity. Note that scale economies do not necessarily lead to misallocation. If the scale elasticity is strictly positive but uniform across industries, then \(\mathcal {L}_{i}=0\).

The optimal export tax-cum-subsidy, furthermore, depends on the entire matrix of own- and cross-price demand elasticities, echoing our previous assertion that \(x_{ij,k}^{*}\) (in Theorem 1) corresponds to the optimal markup of a multi-product monopolist. To better understand this point, assign \(\bar {t}_{i}=0\), in which case \(x_{ij,k}^{*}\) represents a tax on good \(ij,k\) (rather than a subsidy). The optimal tax rate on \(ij,k\) is equal to the optimal mark-up on that good if country \(i\)’s government was pricing its exports as a multi-product monopolist rather than an individual single-product firm. The government’s optimal pricing decision, accordingly, internalizes the effect of raising \(\tilde {P}_{ij,k}\) on its sales of other products in destination \(j\).

Lastly, Theorem 1 can be useful for quantitative applications. It specifies optimal policy as a function

of Marshallian demand elasticities and inverse export supply elasticities, both of which are fully

determined by observable shares (\(r_{ij,k}\) and \(\lambda _{ij,k}\)) and industry-level trade and scale elasticities (\(\sigma _{k}\) and \(\mu _{k}\)). In other

words, Theorem 1 characterizes optimal policy in terms of a set of observable or estimable sufficient

statistics. We capitalize on this feature to simplify our quantitative analysis of optimal policy in Section 6.

Optimal Tariffs are Uniform, Absent Scale Economies or Profits. A canonical special case of Theorem 1 is

the multi-industry Armington case, in which \(\mu _{k}=0\) for all \(k\in \mathbb {K}\). In that case, \(\omega _{ji,k}=0\) for all \(ji,k\) implying that

optimal import tariffs are uniform, i.e., \(t_{ji,k}^{*}=\bar {t}_{i}\) for all \(ji,k\). Intuitively, in the absence of scale economies

or profits, import tariffs cannot influence the producer price of imports on a good-by-good

basis. At best, they can elicit a uniform reduction in import prices by deflating \(\mathbf{w}_{-i}\) relative to \(w_{i}\),

which is best achieved via a uniform import tax rate. Section 4 shows that in the absence of

scale economies and markups, 1st-best optimal tariffs remain uniform even with input-output

linkages.To be clear, these results hinge on the restriction that country \(i\)’s policy does not influence aggregate relative wages in the rest of world. This restriction holds trivially in the two-country case, but requires internal cooperation in the rest of the world otherwise (see online Appendix ).

Special Case with Cobb-Douglas Preferences across Industries.\(\quad\) To gain deeper intuition about Theorem 1, consider a

special case where preferences are Cobb-Douglas across industries. In that case, the formulas specified by Theorem

1 reduce toIn the Cobb-Douglas case, \(\varepsilon _{nj,k}^{(ij,k)}=-\sigma _{k}\mathbf{1}_{n=j}+(\sigma _{k}-1)\lambda _{ij,k}\) and \(\varepsilon _{nj,g}^{(ij,k)}=0\) if \(g\neq k\), which when plugged into the restricted entry case of Equation 5, delivers\[\omega _{ji,k}\approx \frac {\left (1-\frac {\overline {\mu }_{j}}{\mu _{k}}\right )\sum _{g}r_{ji,g}\rho _{j,g}}{1+\sum _{g}\sum _{\iota \neq i}\left [1-\left (1-\frac {\overline {\mu }_{j}}{\mu _{g}}\right )r_{j\iota,g}\rho _{j,g}\left (1+(\sigma _{g}-1)(1-\lambda _{j\iota,g})\right )\right ]}.\] The parameterization of \(\omega _{ji,k}\) under free entry can be derived similarly.

A well-known special case of the above formula is the single-industry\(\times\) two-country formula in Gros (1987). To demonstrate this, drop the industry subscript \(k\) and reduce the global economy into two countries, i.e., \(\mathbb {C}=\left \{ i,j\right \}\). Noting that \(1-\lambda _{ij}=\lambda _{jj}\) in the two-country case, we can deduce from the above formulas that

By the Lerner symmetry, export and import taxes are equivalent in the single-industry model.The Lerner symmetry is a special case of the equivalence result presented under Lemma 1. Also, note that the decentralized equilibrium is efficient in the single industry Krugman model studied by Gros (1987). As such, the optimal industrial subsidy can be also normalized to zero, i.e., \(s_{i}^{*}=0\). Hence, without loss of generality, we can set \(x_{ij}^{*}=0\) and arrive at the familiar-looking optimal tariff formula in Gros (1987), i.e., \(t_{ji}^{*}=1/(\sigma -1)\lambda _{jj}\).

The Cobb-Douglas case of Theorem 1 is also a strict generalization of the formula derived concurrently by Bartelme et al. (2019) for a small open economy with multiple sectors. Specifically, enforcing the small open economy assumption—i.e., setting \(\omega _{ji,k}\approx \lambda _{ij,k}\approx 0\); \(\lambda _{jj,k}\approx 1\)—our optimal policy formulas in the Cobb-Douglas case reduce to:

2.2.2 Second-Best: Unilaterally Optimal Import Tariffs and Export Subsidies

Suppose the government in \(i\in \mathbb {C}\) cannot use domestic subsidies due to say institutional barriers or political pressures. It is optimal, in that case, to use trade taxes as a second-best policy to restore allocative efficiency in the domestic economy. In this section, we derive analytic formulas for second-best optimal trade taxes in such circumstances. Country \(i\)’s optimal policy problem, in this case, includes an added constraint that \(\mathbf{s}_{i}=\mathbf{0}\):

Using the dual approach discussed earlier, we analytically solve Problem (P2) and derive sufficient statistics formulas for second-best optimal trade taxes. The following theorem presents these formulas, with a formal proof provided in the online appendix.

Theorem 2 Suppose the government is unable (or unwilling) to apply domestic industrial subsidies. In that case, the second-best optimal import tariffs and export subsidies are unique up to a uniform tax shifter \(\bar {t}_{i}\in \mathbb {R}_{+}\) and are implicitly given by:

where \(\boldsymbol {\Omega }_{ji}=\left [\omega _{ji,k}\right ]_{k}\) is a vector of inverse export supply elasticities (Equation 7); \(\overline {\mu }_{i}\) denotes the output-weighted average markup in economy \(i\) (Equation 4); and \(\mathbf{E}_{-ii}\), \(\mathbf{E}_{-ii}^{(ii)}\), \(\mathbf{E}_{ij}\), and \(\mathbf{E}_{ij}^{(-ij)}\) are matrixes of Marshallian demand elasticities as defined under Definition (D1).Letting \(N\) and \(K\) denote the number of countries and industries: \(\mathbf{E}_{-ii}\sim \mathbf{E}_{-ii}^{(-ii)}=\left [\mathbf{E}_{ni}^{(\jmath i)}\right ]_{n\neq i,\jmath \neq i}\) is a square \((N-1)K\times (N-1)K\) matrix, where \(\mathbf{E}_{ni}^{(\jmath i)}\equiv \left [\varepsilon _{ni,k}^{(\jmath i,g)}\right ]_{k,g}\) as defined under Definition (D1). Likewise, \(\mathbf{E}_{ij}^{(-ij)}=\left [\mathbf{E}_{ij}^{(nj)}\right ]_{n\neq i}\) and \(\mathbf{E}_{-ii}^{(ii)}=\left [\mathbf{E}_{ni}^{(ii)}\right ]_{n\neq i}\) are respectively \(K\times (N-1)K\) and \((N-1)K\times K\) matrixes. In all the equations, \(\mathbf{1}\equiv \mathbf{1}_{(N-1)K\times 1}\) is a columns vector of ones. Meanwhile, \(\boldsymbol {\Omega }_{-ii}=\left [\omega _{ni,k}\right ]_{n\neq i,k}\) is a \((N-1)K\times 1\) vector; and the operators \(\odot\) and \(\oslash\) denote element-wise multiplication and division.

Theorem 2 asserts that, when governments cannot use industrial subsidies, \((i)\) the optimal export

subsidy is adjusted to promote exports in high-returns-to-scale (high-\(\mu\)) industries, and \((ii)\) the optimal import

tax is adjusted to restrict import competition in high-returns-to-scale (high-\(\mu\)) industries. Intuitively, the

government’s objective when solving (P2) is to mimic Pigouvian industrial subsidies with trade

taxes/subsidies. To reach this objective, import taxes and export subsidies should increase in

high-returns-to-scale industries relative to the first-best benchmark. While these adjustments elevate

domestic production in high-\(\mu\) industries, they are insufficient for obtaining the unilaterally first-best

allocation.

Special Case with Cobb-Douglas Preferences across Industries.\(\quad\) We can invoke the Cobb-Douglas

assumption to further elucidate the second-best tax formulas under Theorem 2. Under this assumption,

there are zero cross-demand effects between industries and the optimal policy formulas specified by

Theorem 2 can be simplified as follows:

where \(1+t_{ji,k}^{*}=(1+\omega _{ji,k})(1+\bar {t}_{i})\) and \(1+x_{ji,k}^{*}=\frac {(\sigma _{k}-1)\sum _{n\neq i}\left [(1+\omega _{ni,k})\lambda _{nj,k}\right ]}{1+(\sigma _{k}-1)(1-\lambda _{ij,k})}(1+\bar {t}_{i})\) denote the first-best optimal rate (the corresponding equation). For a small open economy, the formulas further reduce to

In summary, the above formulas indicate that second-best import taxes are higher in \((1)\) industries with a greater-than-average markup, and \((2)\) industries in which country \(i\) has a comparative advantage (i.e., high-\((\sigma _{k}-1)\lambda _{ii,k}\) industries). These two properties allow second-best import taxes to mimic Pigouvian subsidies to the best extent possible. Likewise, second-best export subsidies feature a misallocation-correcting component that favors industries with a higher-than-average scale elasticity or markup.

Importantly, if the markup or scale elasticity is uniform across industries (i.e., \(\mu _{k}=\mu =\overline {\mu }_{i}\)), the above formulas

yield the first-best or purely ToT-improving tax rate—i.e., \(t_{ji,k}^{**}=t_{ji,k}^{*}\) and \(x_{ij,k}^{**}=x_{ij,k}^{*}\). The intuition is that the Krugman model

without cross-industry markup heterogeneity is efficient; leaving no room for policy interventions to

restore allocative efficiency.

2.2.3 Third-Best: Unilaterally Optimal Import Tariffs

Now suppose that, in addition to restrictions on industrial subsidies, the use of export subsidies is also restricted. The government’s optimal policy problem in this case features two additional constraints, \(\mathbf{s}_{i}=\mathbf{x}_{i}=\mathbf{0}\):

Some variation of the above problem has been studied by an expansive literature on optimal tariffs. Though, nearly all existing studies are limited to partial equilibrium two-by-two models. Here, we use the same dual approach described earlier to analytically solve Problem (P3) within our multi-country, multi-industry general equilibrium framework. Our derivation, as before, yields simple sufficient statistics formulas for optimal third-best import taxes. The following theorem presents these formulas, with a formal proof provided in the online appendix.In the special case where entry is restricted and countries are sufficiently small, the optimal tariff formula presented under Theorem 4 reduces to the formula used by Lashkaripour (2021) to examine global tariff wars.

Theorem 3 Suppose the government is unable to apply domestic industrial subsidies or export subsidies. In that case, 3rd-best optimal import tariffs are uniquely given by

Unlike Theorems 1 and 2, the third-best optimal tariff schedule identified by Theorem 3 is unique. That is because the multiplicity implied by Lemma 1 no longer applies when both export and industrial subsidies are restricted to zero. Nevertheless, the third-best tariff specified by Theorem 3 differs from the second-best tariffs (in Theorem 2) by only a uniform tariff shifter, \(1+\bar {\tau }_{i}^{*}\). So, barring the uniform component, \(1+\bar {\tau }_{i}^{*}\), we can understand the above formula based on the same intuition provided under Theorem 2.

The uniform tariff component, \(1+\bar {\tau }_{i}^{*}\), compensates for the unavailability of export tax-cum-subsidies to the government. By the Lerner symmetry, which is implicit in Lemma 1, import taxes can perfectly mimic a uniform export tax. This ability was previously redundant (under Theorems 1 and 2) because export taxes/subsidies were directly applicable, and there was no point in using other instruments to mimic them. But since export taxes are restricted under Problem (P3), it is optimal to uniformly raise all tariffs by a factor \(1+\bar {\tau }_{i}^{*}\), using them as a second-best substitute for optimal export taxes/subsidies.

3 Discussion: The Efficacy of Trade and Industrial Policy

This section, guided by Theorem 1-3, discusses the efficacy of trade and industrial policy in distorted open

economies. We conjecture that standalone trade policy measures can be ineffective even when chosen

optimally. Unilateral scale correction via industrial policy can also backfire, underscoring the importance

of international coordination. We later test these conjectures by estimating model parameters and

utilizing our optimal policy formulas.

Tension between Allocative Efficiency and ToT.\(\quad\) Theorems 2 and 3 reveal that second-best trade

policies seek to strike a balance between \((a)\) improving the terms-of-trade (ToT), which requires contracting

exports in nationally differentiated (low-\(\sigma\)) industries, and \((b)\) correcting misallocation, which requires

expanding output in high-returns-to-scale (high-\(\mu\)) industries. Obtaining this balance becomes difficult if

not impossible when \(Cov\left (\sigma _{k},\mu _{k}\right )<0\)—which is the empirically-relevant case based on our forthcoming estimation. To

navigate this tension, a welfare-maximizing government must tailor its (2nd-best) trade policy in a way

that curtails the ToT gains without necessarily correcting misallocation. This balancing act erodes

the gains from 2nd-best trade policies and can even render them industry-blind—unable to

beneficially correct inter-industry misallocation or manipulate industry-specific export market

power.In the canonical Krugman (1980) model where \(\mu _{k}=1/\left (\sigma _{k}-1\right )\), optimal (2nd-best) import tariffs and export subsidies are industry-blind for a small open economy. In particular, applying Theorem 2 to this special case yields,\[1+t_{ji,k}^{**}=1+\bar {t}_{i};\qquad \qquad \qquad 1+x_{ij,k}^{**}=\left (1+\bar {t}_{i}\right )\left (1-\frac {1}{\overline {\sigma }_{i}}\right ),\] where \(\bar {t}_{i}\in \mathbb {R}\) is an arbitrary tax shifter and \(\overline {\sigma }_{i}=\left (\sum _{k}\rho _{i,k}/\sigma _{k}\right )^{-1}\) is the sales-weighted average trade elasticity facing country \(i\). The optimal trade tax in each industry is evidently blind to misallocation (\(\mu _{k}\)) or industry-specific export market power (\(\sigma _{k}\))—reflecting the difficulty to reconcile these two policy considerations. All this policy choice can achieve is to improve country \(i\)’s aggregate ToT by inflating its wage relative to the rest of the world.

The tension between allocative efficiency and ToT can be theoretically demonstrated for a local change in policy (see the online appendix). But how this tension precisely modifies the ex-ante gains from trade policy is an empirical matter. Our conjecture is that if industry-level trade and scale elasticities exhibit a strong negative correlation, the welfare gains from trade policy are limited—a claim we evaluate quantitatively in Section 6.

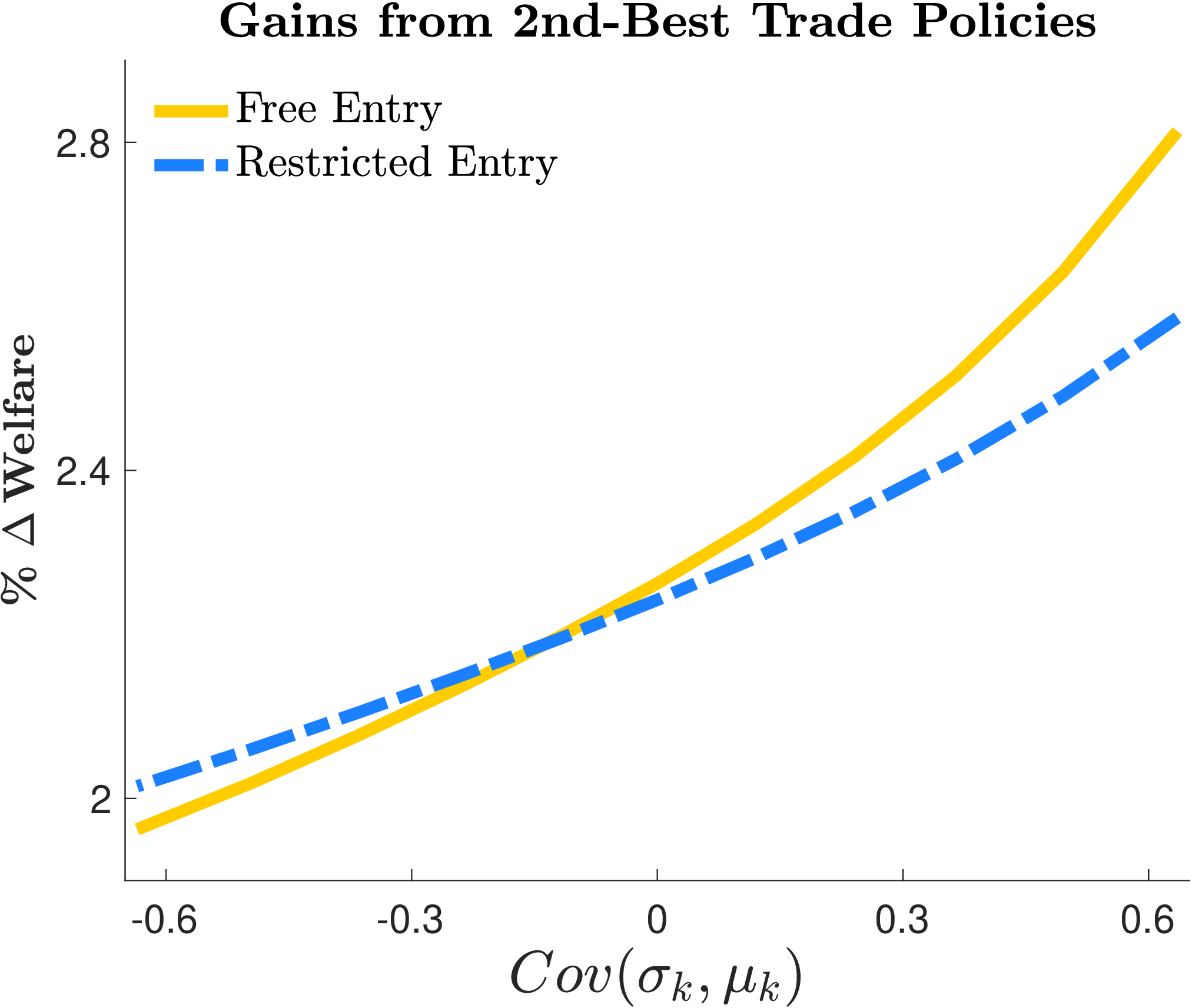

Conjecture 1 If industry-level trade and scale elasticities exhibit a strong negative correlation (\({Cov\left (\sigma _{k},\mu _{k}\right )\ll 0}\)), standalone trade policy measures deliver limited welfare gains even when set optimally.

A formal evaluation of this conjecture requires estimating model parameters, as performed in Sections 5 and 6. Nevertheless, we can numerically illustrate this point using artificial parameter values, as presented in Figure 1. The left panel demonstrates that the gains from 2nd-best trade policies diminish rapidly as \(Cov\left (\sigma _{k},\mu _{k}\right )\) is artificially lowered from positive to negative values. In each case, the trade elasticities are held constant, meaning that the scope for ToT gains remains the same. The only thing that changes is the tension between ToT and corrective gains from policy, which amplifies as \(Cov\left (\sigma _{k},\mu _{k}\right )\) becomes more negative.This tension is distinct from the targeting principle (Bhagwati and Ramaswami (1963)), which applies irrespective of the sign of \(Cov\left (\sigma _{k},\mu _{k}\right )\). Indeed, 2nd-best trade taxes become more potent despite the targeting principle if \(Cov(\sigma _{k},\mu _{k})>0\); but we focus on the case where \(Cov\left (\sigma _{k},\mu _{k}\right )<0\) as it aligns with our forthcoming estimation.

Unilateral Scale Correction can Cause Immiserizing Growth.\(\quad\)

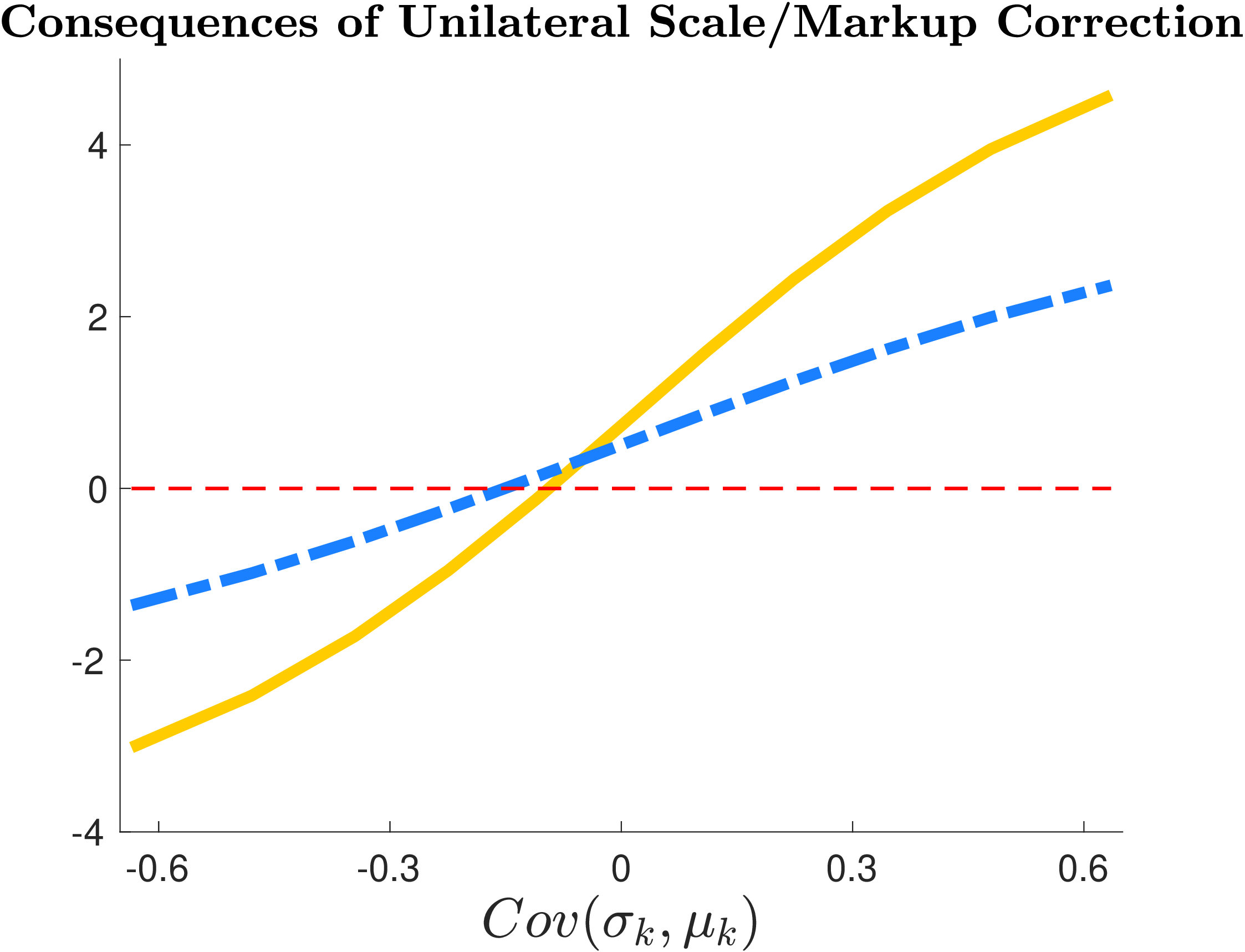

The flip side of the noted tension is that if \(Cov\left (\sigma _{k},\mu _{k}\right )<0\), unilateral implementation of scale-correcting Pigouvian subsidies worsens the ToT, resulting in possibly adverse welfare consequences. These arguments echo the immiserizing growth paradox in Bhagwati, 1958 and follow a simple logic. If \(Cov\left (\sigma _{k},\mu _{k}\right )<0\), scale-correcting Pigouvian subsidies expand domestic output in high-\(\sigma\) industries, which are nationally differentiated industries in which countries hold significant export market power. Elevating output and, thus, exports in these industries could worsen the ToT to the point of triggering immiserizing welfare effects.

the online appendix demonstrates theoretically that if \(Cov\left (\sigma _{k},\mu _{k}\right )<0\), unilateral scale/markup correction worsens the ToT. But whether these adverse ToT effects outweigh the allocative efficiency gains from scale/markup correction is an empirical matter. We conjecture that if industry-level trade and scale elasticities exhibit a strong negative correlation, the adverse ToT effects from scale correction are large enough to cause immiserizing growth.

Conjecture 2 If industry-level trade and scale elasticities exhibit a strong negative correlation (\({Cov\left (\sigma _{k},\mu _{k}\right )\ll 0}\)), unilateral scale (or markup) correction via industrial policy will likely worsen national welfare, echoing the immiserizing growth paradox.

We evaluate this conjecture with micro-estimated parameters in Section 6, but a numerical

illustration with artificial parameter values is also provided in Figure 1 (right panel). This figure is

produced by fixing the degree of inter-industry misallocation and artificially adjusting trade elasticities to

vary \(Cov\left (\sigma _{k},\mu _{k}\right )\) from positive to negative values. In regions where \(Cov\left (\sigma _{k},\mu _{k}\right )<0\), a unilateral adoption of scale-correcting subsidies

compromises welfare, causing immiserizing growth. These immiserizing consequences, as we discuss next,

can be an obstacle for industrial policy implementation for countries committed to efficient trade policies

under shallow agreements.

Industrial Policy Coordination via Deep Agreements.\(\quad\) Immizerising growth

can be a major obstacle to industrial policy implementation in open economies. To

convey this point, we adopt the common view that intentional negotiations involve two

stages.Modeling international cooperation as a two-stage game consisting of enactment and implementation stages is commonplace in the global governance literature (Shaffer and Pollack (2009)). In the trade and environmental policy literature, many studies treat international negotiations as multi-stage games where initial stages restrict policy choices and latter stages ensure implementation (e.g., Murdoch, Sandler and Vijverberg (2003); Drazen and Limão (2008); Kosfeld, Okada and Riedl (2009)). In

the first-stage, governments negotiate over policy space to ensure each party restricts itself to the globally

efficient policy choice (the corresponding equation). In the second stage, governments negotiate a deeper agreement to

ensure the implementation of efficient (misallocation-correcting) policies, with each country having the

choice to either implement efficient policies or withhold implementation.