Markups as Shadow Tariffs:

How Market Power Skews Trade Reciprocity

Siying Ding (UIBE)

Ahmad Lashkaripour (Indiana University, CESifo, CEPR)

Volodymyr Lugovskyy (Indiana University)

Working paper · January 2026

Read PDF · Markdown source · Reader view · Slides

Abstract. We show that in open economies, firm markups function as shadow tariffs: they generate domestic deadweight losses but also shift surplus internationally through excess profits earned abroad. These international profit-shifting effects represent a pure distributive externality, benefiting countries that capture a larger share of global excess profits. We derive a new formula for the welfare loss from market power under these distributive externalities and compile global data on firm markups and multinational ownership to measure the tariff-equivalent of observed markups. Our findings reveal that high-income countries capture a disproportionate share of global excess profits. Consequently, the welfare losses from market power for these countries are mitigated, and in some cases reversed, through net profit inflows from abroad. We estimate that these profit-shifting externalities are equivalent to a 17.6 percent shadow tariff imposed by high-income countries—challenging the view that advanced countries have made outsized concessions under existing trade agreements.

1 Introduction

Growing trade integration and market power are two defining features of today’s global economy. Taken together, they raise a basic question: are the welfare losses from market power localized, or do they spill over internationally through increased trade integration? Current research provides no clear answer. The literature has largely focused on how trade integration curbs market power through pro-competitive pressures. Far less attention has been paid to spillover effects: whether the burden of market power has shifted internationally through trade relations. If such spillovers exist, they amount to an international externality, the kind that cannot be addressed by domestic policy alone.

This paper explores this often overlooked aspect of global market power. Our central thesis is that firm markups generate significant international spillover effects, making them functionally equivalent to import tariffs. Like tariffs, markups introduce a domestic deadweight loss. But they also create distributive beggar-thy-neighbor effects: monopolistic markups shift surplus from foreign consumers to domestic firms through excess profits earned abroad. We show that, under fairly general conditions, there exists a shadow tariff schedule that replicates the aggregate welfare effects of markups.

Our analysis begins with a theoretical welfare decomposition that separates the aggregate loss from market power into two parts: \((i)\) the conventional deadweight loss from markup dispersion, and \((ii)\) a distributive profit-shifting externality. The latter mirrors classic terms of trade effects: it benefits countries that capture a larger share of global excess profits at the expense of others.

We measure these distributive profit-shifting effects empirically and test our equivalence result using newly compiled data on firm markups and multinational ownership across countries. Our analysis reveals that high-income economies collect a disproportionate share of global excess profits. As a result, the welfare losses from market power in these countries are partly, or in some cases entirely, counterbalanced by incoming profits earned abroad. The Netherlands offers a particularly bold example: although markups introduce the usual distortion to domestic prices in this country, the inflow of foreign-raised excess profits more than compensates for the loss in consumer surplus, yielding a net aggregate welfare gain.

On average, we estimate that profit-shifting effects have attenuated the aggregate welfare loss from market power in high-income countries by roughly 15%, precisely because these economies are net recipients of global profit inflows. By contrast, lower-income countries that experience net profit outflows face magnified welfare losses—approximately 44% higher than they would in the absence of profit-shifting. These equilibrium profit-shifting effects represent a shadow tariff of about 17.6 percent imposed by high-income nations on their trading partners. In practice, such shadow tariffs erode, or even neutralize, the non-reciprocal concessions that developed countries extend under the WTO framework, challenging a growing line of criticism regarding asymmetries in the global trading system.

Section 3 presents our baseline semi-parametric model of the global economy, which borrows elements from Arkolakis et al. (2019) and Errico and Lashkari (2022). Our baseline model features many countries and industries. Firms apply variable and heterogeneous markups and select into international markets à la Melitz and Ottaviano (2008). We also formalize and quantify extensions with firm entry dissipating quasi-rents, multi-national ownership, and global input-output linkages.

Section 4 presents our sufficient statistics formulas for the aggregate loss from market power under trade relations. We show that the loss can be decomposed into \(\left (i\right )\) an entropy-based measure of markup dispersion, \((ii)\) changes to the gains from trade due to markup-distorted relative factor prices, and \((iii)\) zero-sum international profit-shifting effects.

International profit-shifting effects are a pure distributive externality. Our formula equates them to the ratio of the average expenditure-side markup to the average output-side markup. This ratio diverges from one due to a locational decoupling between where markups burden consumer surplus and where the excess profits are remitted to households. As a result of this decoupling, countries that collect a disproportionate share of global excess profits experience a reduced loss due to net profit inflows from abroad, while other countries endure a disproportionately higher welfare loss due to net profit outflows.

Section 5 presents our duality result: if countries are sufficiently open to trade, firm-level markups function as shadow tariffs. The markups shift the terms of trade in favor of countries that collect a greater share of global excess profits. We establish this result in three steps. First, we show that a country can unilaterally raise its welfare through a uniform markup on exports. Second, we demonstrate that a centralized uniform markup on exports is equivalent to an import tariff, echoing the Lerner symmetry. Third, we show that the centralized markup or tariff yields higher welfare gains than decentralized markups. Taking these results together, we invoke the Intermediate Value Theorem to show that if trade levels are sufficiently high, there exists a uniform tariff that replicates the aggregate welfare effects of decentralized markups.

We calibrate our model using data described in Section 6. First, we construct novel data on multinational profit flows using financial statements of multinational enterprises from the ORBIS database. Second, we estimate global firm markups using two conventional approaches: the cost-based method and the demand-based approach. For the cost-based estimates, we use a global sample of publicly traded firms from WORLDSCOPE. Because performing structural demand estimation at scale is challenging, we employ the computationally efficient linear approximation of Salanié and Wolak (2019), and leverage high-frequency transaction-level trade data to guide identification despite limited information on product characteristics. We supplement these firm-level data with international statistics on aggregate output, expenditure, and sectoral input-output shares from the OECD Inter-Country Input-Output (ICIO) tables. Combining these sources, we estimate (1) markup dispersion, (2) expenditure-weighted average markup, (3) output-weighted average markup, and (4) profit ownership shares across 64 major countries plus an aggregate of the rest of the world over the period 2005–2015.

Using data on global markups and profit flows, we measure the aggregate welfare loss from market power across many countries. We find that these losses have modestly increased over time in most countries, with markups reducing real consumption globally by more than 7% in 2015. However, the losses are markedly larger among low-income countries. In fact, some high-income countries, such as the Netherlands, even benefit on net from market power because of sizable profit inflows from abroad.

The North–South divide in welfare losses from market power is largely driven by profit-shifting externalities. Net excess profit flows from low-income to high-income countries have increased the burden of market power for low-income economies by 44%, while reducing the burden for high-income countries by 15%. This pattern is robust to alternative assumptions about how markups are estimated, multinational ownership structures, global input-output linkages, and fixed-cost payments. These asymmetries reflect the fact that low-income countries tend to specialize in less sophisticated, low-markup industries.

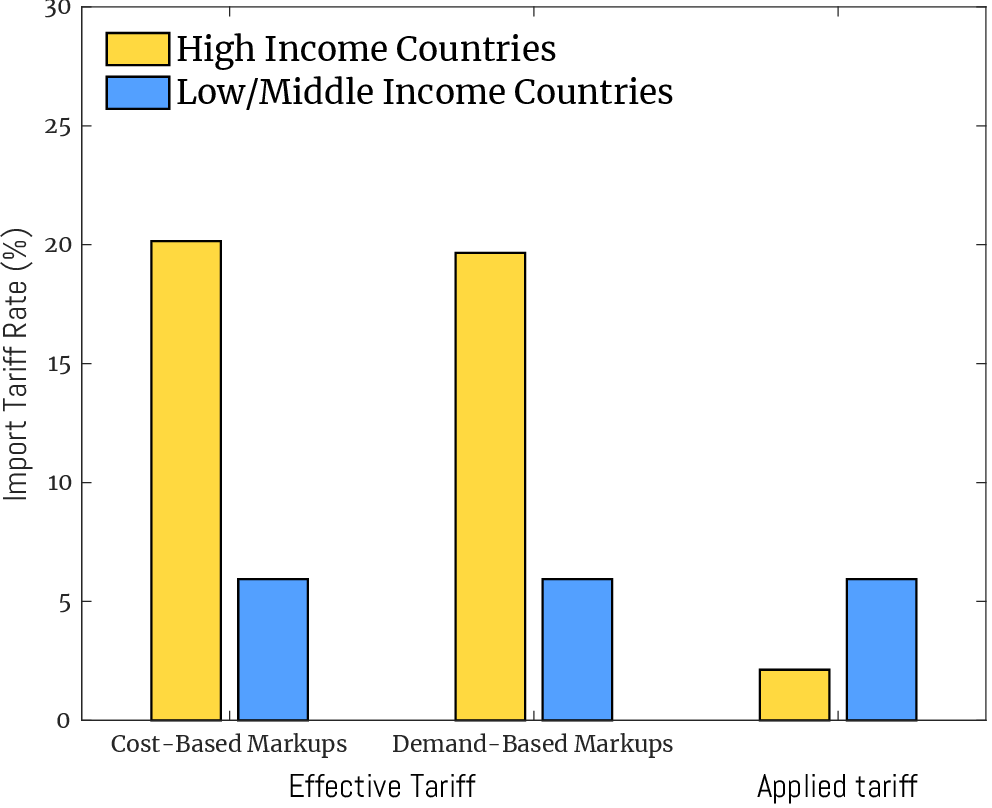

We estimate that international profit-shifting externalities are akin to a 17.6% shadow tariff imposed by high-income countries on their trading partners. This finding sheds fresh light on the current state of concessions within global trade agreements, challenging the growing narrative that high-income countries, such as the United States, have made disproportionately greater concessions under the status quo (Chow et al., 2018). On a superficial level, high-income countries may appear to be making additional concessions and offering preferential treatment to their low-income counterparts under the WTO’s Generalized System of Preferences (GSP). But in reality, profit-shifting externalities more than counteract the GSP concessions. After factoring in the implicit tariff due to profit-shifting externalities, high-income countries are effectively applying a 14% excess tariff on low-income partners.

Our theoretical framework relates to a vibrant literature examining the aggregate welfare loss from market power, and distortions more broadly. A key insight from the early generation of studies, including Lerner (1934) and Harberger (1954), is that aggregate welfare losses in closed economies are linked to markup dispersion. Later work, such as Hsieh and Klenow (2009), Baqaee and Farhi (2020), and Edmond, Midrigan, and Xu (2023) provide parametric formulas for these aggregate welfare losses in closed-economy settings. There are limited counterparts for these formulas in open-economy contexts. Several studies including Atkin and Donaldson (2021), Baqaee and Farhi (2024) provide general frameworks for ex-ante growth accounting in distorted open economies.As in Arkolakis, Costinot, Donaldson, and Rodríguez-Clare (2019), pro-competitive effects are essentially absent in our framework because the direct pro-competitive effects on firm markups are exactly offset by firm-selection effects. However, there is literature examining pro-competitive effects in alternative settings, including Melitz and Ottaviano (2008), Holmes, Hsu, and Lee (2014), De Blas and Russ (2015),Edmond, Midrigan, and Xu (2015), Feenstra and Weinstein (2017). Relatedly, Bai, Jin, and Lu (2024) note that trade integration can exacerbate misallocation in distorted economies, potentially worsening aggregate welfare.The idea that trade can exacerbate domestic misallocation has also been explored by Epifani and Gancia (2011); Bai, Jin, and Lu (2019), Manova (2013), Farrokhi et al. (2024), and Dix-Carneiro et al. (2021) in various contexts. We contribute to this literature by proving a trade-adjusted formula for the aggregate welfare loss from markup distortions, emphasizing the zero-sum profit-shifting effects, and establishing conditional equivalence between firm markups and tariffs.

Our equivalence result is related to an old literature that converts micro-level tariff wedges into one macro-level tariff index (Anderson and Neary (1996, 2005, 2003); Looi Kee et al. (2009); Irwin (2010); Soderbery (2021)). Our approach is similar in that we convert micro-level wedges into a representative tariff index. However, we differ from these papers in important ways: we establish equivalence between decentralized firm-level markups and a centralized tariff index. This equivalence has implications for reciprocity and bilateral tariff concessions, contributing to recent quantitative assessments of reciprocity as in Bown, Parro, Staiger, and Sykes (2023) and Anderson and Yotov (2025).

The profit-shifting externalities emphasized in this paper are related but different from those in the strategic trade policy literature (e.g., Brander and Spencer (1985); Ossa (2012); Bagwell and Staiger (2012); Lashkaripour (2021); Mrázová (2024)). In these frameworks profit-shifting is not an equilibrium externality, but is strategically generated by government policies. More specifically, government may use trade policy measures to promote high-profit activities and strategically shift excess profits to their country. Our contribution to this literature is to highlight the reverse aspect: We demonstrate that decentralized pricing decisions by firms generate large distributive externalities, yielding terms-of-trade benefits that, for some countries, outweigh the domestic efficiency losses from markup pricing. As a result, governments may purposefully avoid regulating firms to preserve these implicit terms of trade benefits.

2 Simple Illustration of Profit-Shifting Externalities

Before presenting our general model, we showcase the profit-shifting mechanism using a simple model. There are two countries: North (\(N\)) and South (\(S\)); and two traded sectors: a differentiated sector and a homogeneous sector. The latter is indexed \(0\) and is perfectly competitive. The homogeneous good is traded and produced one-to-one with labor in both countries. We assign the homogeneous good as the numeraire (\(p_{i,0}=p_{0}=1\)) and assume that the homogeneous sector is sufficiently large to have active production in both countries, equalizing prices internationally.

The utility function across industries is quasi-linear: \(U_{i}=q_{i,0}+\frac {\alpha }{\beta }Q_{i}-\frac {1}{2\beta }Q_{i}^{2}\), where \(Q_{i}\) is a composite aggregator over differentiated firm varieties and \(q_{i,0}\) is the quantity of the homogeneous good. Utility maximization implies a linear demand for the composite differentiated good in each country:

where \(P_{i}\) is the price index of the composite differentiated good in country \(i\).

Production and markups in the differentiated sector.\(\quad\) A fixed measure \(M_{i}\equiv \mid \Omega _{i}\mid\) of firms indexed by \(\omega \in \Omega _{i}\) supply the differentiated good in each country. The firms are symmetric and monopolistically competitive. Each operates with a common unit labor cost, \(c\). The demand for firm varieties of the differentiated good is CES. In particular, the consumption aggregator is \(Q_{i}=(\int _{\Omega _{i}}q_{\omega }^{\frac {\sigma -1}{\sigma }}d\omega )^{\frac {\sigma }{\sigma -1}}\), yielding a constant elasticity demand for firm varieties: \(q_{\omega }=p_{\omega }^{-\sigma }\times P_{i}^{\sigma }Q_{i}\). The monopolistically competitive firms charge a constant markup \(\mu =\frac {\sigma }{\sigma -1}\) over marginal cost \(c\), implying a common firm-level price, \(p_{\omega }=\mu \times c\). The unit price for the composite differentiated good is thus:

For simplicity, we assume henceforth that \(M_{i}=1\), so that the price of the composite differentiated good is equalized to \(P\equiv \mu \times c\) in both countries.

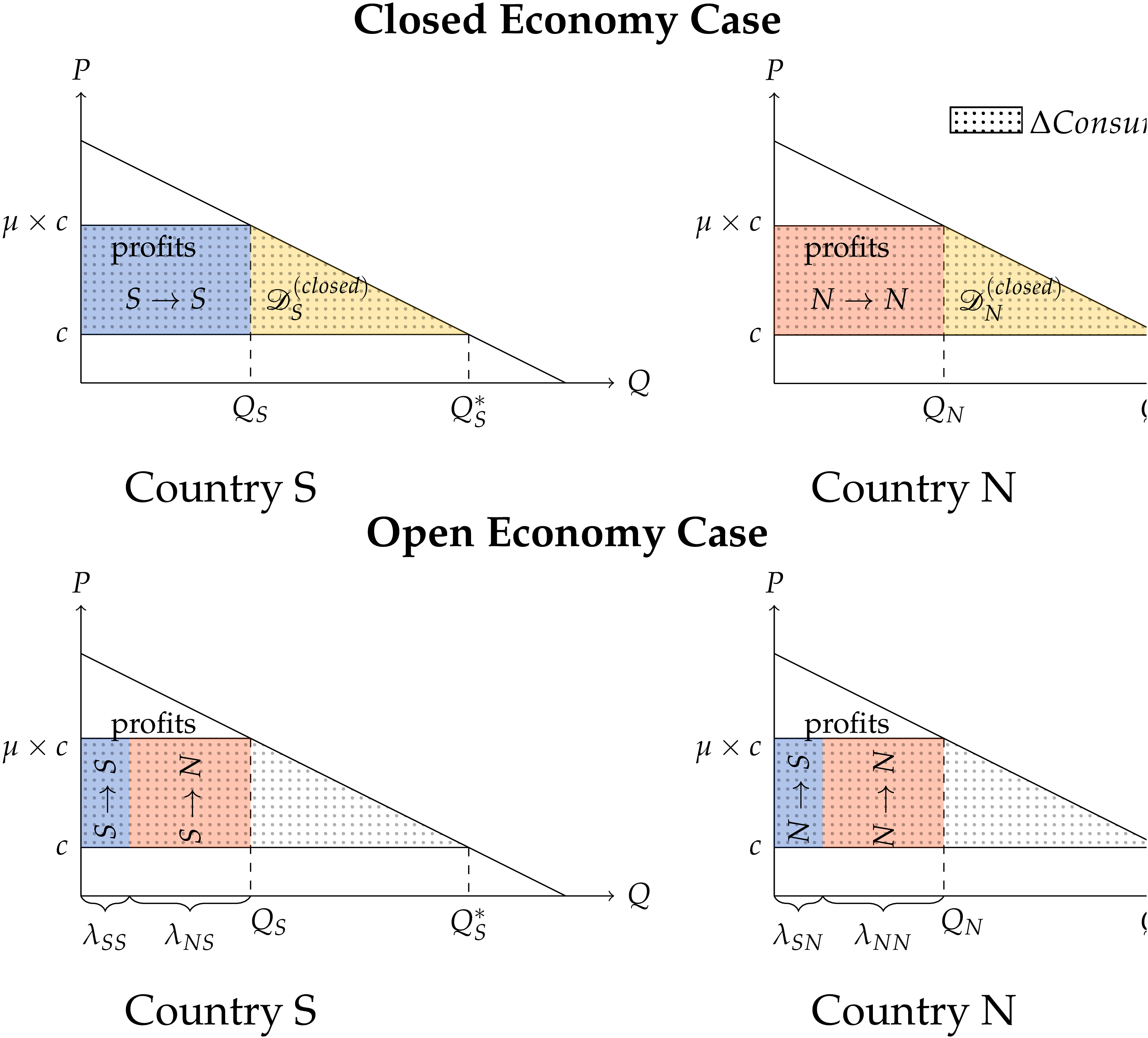

Aggregate welfare loss from markups.\(\quad\) We now characterize the aggregate welfare loss from markups, starting from the closed economy case. As shown in the top panel of Figure 1, the aggregate welfare loss from markups for each country \(i=N,S\) is the reduction in consumer surplus \(\Delta CS_{i}\) minus the profit rebates, \(\frac {\mu -1}{\mu }PQ_{i}\). Namely,

Figure 1 is a textbook digram: it states that the losses coincides with the Harberger triangle. The intuition is that excess profits in each country are ultimately rebated to consumers as supplementary lump-sum transfers. Thus, the loss in consumer surplus due to markups is partially offset by these rebates, leaving a residual deadweight loss equal to the triangle.

Now, consider an open economy setting. Here, the textbook argument breaks down because excess profits are no longer remitted within the same location where they distort prices and reduce consumer surplus. To illustrate this, we retain the assumption that consumer have access to measure \(M_{i}\equiv \mid \Omega _{i}\mid =1\) of varieties. However, they now can choose from domestic and foreign varieties. In particular, \(\Omega _{i}=\Omega _{Ni}\cup \Omega _{Si}\) with \(M_{Ni}\equiv \mid \Omega _{Ni}\mid\) and \(M_{Si}\equiv \mid \Omega _{Si}\mid\). Since the total number of varieties is unchanged (i.e., \(M_{i}=1\)) the price index of the differentiated good is unaffected: \(P=\mu \times c\). However, now a share \(\lambda _{\ell i}=M_{\ell i}/M_{i}\coloneqq M_{\ell i}\) of country \(i\)’s demand quantity and expenditure comes from firms located in country \(\ell \in \{N,S\}\).

Consider a scenario where \(N\) has a revealed comparative advantage in the differentiated sector, due to hosting a larger measure of differentiated firms:

The south \(S\) is, thus, a net importer of the differentiated good and a net exporter of the homogeneous good for markets to clear.

The bottom panel in Figure 1 illustrates the welfare effects of markup pricing in the open economy scenario. Suppose profits earned by firms located in country \(i\) are repatriated to households in that country. The loss to consumer surplus in country \(i\) is now offset by profits earned on both domestic and foreign sales. This leads to a locational decoupling between profit rebates and the loss to consumer surplus. Consequently, the welfare loss from markups no longer equals the Harberger triangle. Instead, the losses are either greater or smaller depending on whether country \(i\) is a net payer or recipient of excess profits to/from abroad. In this example, the aggregate loss is amplified for the South (\(S\)) due to net profit outflows. In particular, noting that \(Q\coloneqq Q_{S}=Q_{N}\) under symmetric demand, we get

By comparison, the aggregate loss for the North (\(N\)) is attenuated by net profit inflows from the South:

Profit-shifting effects, thus, constitute a pure distributive externality. They are zero-sum transfers from one country to another, enabled by inefficient price wedges.

This stylized model clarifies that countries capturing a disproportionate share of global excess profits benefit from profit-shifting externalities. Appendix B presents stylized evidence indicating that high-income countries indeed appropriate a larger share of global excess profits. To conduct formal measurement, we first formalize this mechanism in a general equilibrium model with many countries and sectors operating under variable and heterogeneous markups. We then show that markups operate as shadow tariffs when countries are sufficiently open.

3 Theoretical Model

We consider a semi-parametric model of the global economy consisting of multiple countries, indexed by \(n,\,i=1,..,N\). The product space is partitioned into multiple industries, indexed by \(k,g=1,...,K\). Country \(i\) hosts a fixed number of firms indexed by \(\omega\) in each industry \(k\). Each firm supplies a single traded and differentiated product variety. Labor is the only primary factor of production, and each country \(i\) is endowed with an inelastic supply of labor, \(L_{i}\), that is paid an equilibrium wage, \(w_{i}\). Labor is internationally immobile but mobile across different production activities within a country.

Demand. The representative consumer in country \(n\) maximizes a semi-parametric utility function with unitary elasticity of substitution across industries. Let \(\Omega _{n,k}\) denote the set of varieties available to the consumer in industry \(k\), with \(\mathbf{p}_{n,k}\equiv \{p_{\omega }\}_{\omega \in \Omega _{n,k}}\) denoting the price vector associated with these varieties. The demand for individual varieties is of the homothetic with aggregator form, nesting an important class of demand systems commonly used in the literature. Specifically, the share of expenditure on variety \(\omega \in \Omega _{n,k}\) with price \(p_{\omega }\) is

where \(P_{n,k}\equiv \mathscr {P}_{k}(\mathbf{p}_{n,k})\) is a homogeneous of degree one price aggregator. This aggregator solves the following depending on whether preferences are directly implicit additive, indirectly implicit additive, or of the single aggregator type (e.g., Kimball):

The function \(D_{k}(x)\) is positive-valued and decreasing over \(x\in \left (0,a\right )\) and exhibits a constant relative choke price \(a\in \mathbb {R}_{+}\): \(\lim _{x\rightarrow a}D_{k}\left (x\right )=0\) and \(D_{k}\left (x\right )=0\) for \(x\geq a\). Without loss of generality we normalize \(a=1\), hereafter.

Demand Function.\(\quad\) The demand facing a firm \(\omega \in \Omega _{n,k}\) is fully determined by its price \(p_{\omega }\), two aggregate shifters, \(P_{n,k}\) and \(\Upsilon _{n,k}\). Namely,

where \(P_{n,k}\) is the price aggregator defined above and \(\Upsilon _{n,k}\equiv \frac {e_{n,k}E_{n}}{P_{n,k}}\left (\int _{\Omega _{n,k}}\frac {p_{\omega '}}{P_{n,k}}D_{k}(\frac {p_{\omega '}}{P_{n,k}})d\omega '\right )^{-1}\), with \(e_{n,k}\) denoting the constant share of expenditure on industry \(k\) goods and \(E_{n}\) denoting total expenditure in country \(n\).

Firms and Production. Country \(i\) hosts a fixed set of firms in industry \(k\) that sell to various locations and compete under monopolistic competition. In our baseline model, there are no fixed overhead costs associated with accessing individual markets. Hence, firm selection across markets is driven solely through the choke price. Throughout the paper, we assume that goods markets are perfectly segmented across countries. Let \(\Omega _{in,k}\subset \Omega _{i,k}\) denote the set of firms that actively serve market \(n\) from origin \(i\). For firm \(\omega \in \Omega _{in,k}\) with productivity \(\varphi\), the unit cost of supplying its variety to country \(n\) is,

where \(\tau _{in}\geq 1\) represents the iceberg trade cost (with \(\tau _{ii}=1\)) and \(w_{i}\) is the wage rate.

Firm Productivity Distribution.\(\quad\) The firm-level productivity \(\varphi\) is the realization of a random variable drawn independently across firms in each country and industry from distribution \(G_{i,k}(\varphi )\). As in Melitz and Ottaviano (2008), we assume that \(G_{i,k}\) is Pareto with a location-specific scale parameter but the same shape parameter \(\theta >0\) globally, with \(\varphi \geq \bar {\varphi }_{i,k}\):

Profit Maximization and Markups.\(\quad\) The profits collected by firm \(\omega \in \Omega _{in,k}\) from sales to market \(n\) can be specified as

The firms are monopolistically competitive and choose their price \(p_{\omega }\) à la Bertrand to maximize profits. Firms’ profit maximization implies an optimal price that exhibits a variable and heterogeneous markup \(\mu _{\omega }\) over marginal cost:

where \(\mu _{\omega }=m_{k}(\nu _{\omega })\), with \(\nu _{\omega }\equiv P_{n,k}/c_{\omega }\) representing the competitiveness of variety \(\omega \in \Omega _{in,k}\) in that market. The function \(m_{k}(\nu _{\omega })\) is injective and the implicit solution to

where \(\varepsilon _{k}(x)\equiv -\partial \ln D_{k}(x)/\partial \ln x\). We assume that \(\varepsilon _{k}'(x)<0\), which is a sufficient condition for \(m_{k}(.)\) to be injective. Since \(\lim _{x\to 1}\varepsilon _{k}(x)=\infty\), then \(m_{k}(1)=1\), indicating that the marginal cost \(c\) of the least efficient firm that can remain active is equal to the choke price, irrespective of the firm’s origin. Accordingly, firms actively selling from origin \(i\) to destination \(n\), have \(\nu\) values that span the entire set \(\mathcal {V}=[1,\infty ]\), irrespective of the cost and demand profiles of countries \(i\) and \(n\).

General Equilibrium. For a given set of parameters, equilibrium is vector of demand quantities, \(\mathbf{q}\), prices, \(\mathbf{p}\), wages, \(\mathbf{w}\), and income, \(\mathbf{Y}\), such that the representative consumer’s utility is maximized in each country; firm-level profits are maximized; labor markets clear, so wage payments in country \(i\) equal sales net of markups,

and aggregate expenditure \(E_{i}\) equals aggregate income, \(Y_{i}\), which is wage income plus lump-sum profit rebates:

Our baseline model assumes that profits are entirely rebated to consumers in the firms’ country of origin. Later, we relax this assumption and allow for multinational production and global profit ownership.

Aggregate equilibrium shares.\(\quad\) Aggregate trade shares are described by a gravity equation

with a trade elasticity equal to \(\theta\). The shifter \(\chi _{i,k}\) collects all the constants, including those specific to (\(i,k\)), such as \(\bar {\varphi }_{i,k}\). Total sales from country \(i\) are thus \(Y_{i}=\sum _{n}\sum _{k'}\lambda _{in,k'}e_{n,k'}E_{n}\), where \(e_{n,k}\) is the constant expenditure share on industry \(k\) in destination \(n\) Accordingly, the share of country \(i\)’s sales collected from goods pertaining to industry \(k\) is

Markup-Based Equilibrium Representation. Recall that for each country-pair the set of firms that actively export from one to the other spans the entire set \(\nu \in (1,\infty )\). Hence, it is straightforward to verify that the markup distribution of exports from any origin to any destination has a common form:

Since \(m_{k}(.)\) is injective and firm productivity, and thus, \(\nu\), follows a Pareto distribution, the markup distribution can be obtained as

Additionally, within industry \(k\), there is a one-to-one country-blind correspondence between a firm’s markup and its competitiveness measure, \(\nu _{k}(\mu )=m_{k}^{-1}(\mu )\). As a result, for any market \(n\), the price is fully determined by knowing the markup as

Note that the origin-specific cost shifters (\(\tau\) and \(w\)) do not explicitly appear in the above equation, but they implicitly influence the markup \(\mu\). Firms from higher cost locations charge a lower markup with the same productivity, which also translates to a lower \(m_{k}^{-1}(\mu )\). In other words, firm markups convey all the price-relevant information marginal cost parameters.

Building on these observations, for any market \(n\), the market share of firms with markup \(\mu\) within industry \(k\) is given by

irrespective of its origin, where \(\widetilde {g}_{k}(x)\equiv d\widetilde {G}_{k}(x)/dx\). Note that \(\lambda _{k}(\mu )\) is not only origin blind but it is also destination-blind, since the aggregator \(P_{n,k}\) shifts all prices in market \(n\) uniformly without affecting relative demand shares; thus, dropping out of the above equation.

Aggregate expenditure and sales shares.\(\quad\) Country \(i\)’s aggregate share of expenditure on goods with markup \(\mu \in [1,\infty )\) is the weighted sum across all industries

where \(e_{i,k}\) is the industry-level expenditure share pinned down by the cross-industry utility aggregator and the aggregate sales shares are

where \(y_{i,k}\) is the industry-level sales share described by Equation 3. These equations draw on the result that \(\lambda _{k}(\mu )\) is independent of destination and origin, representing the within-industry share of expenditure and sales for varieties with markup \(\mu\).

Additional Notation. To condense the notation, we hereafter use \(\mathbb {E}_{\omega }\left [.\right ]\), \(\widetilde {\mathbb {E}}_{\omega }\left [.\right ]\), and \(MLD_{\omega }\left [.\right ]\) to denote the arithmetic mean, harmonic mean, and mean log deviation operators. In particular, for a generic function, \(f:[1,\infty )\rightarrow \mathbb {R}\), define

where \(\omega:[1,\infty )\rightarrow [0,1]\) is a well-behaved weight function that satisfies \(\int _{1}^{\infty }\omega \left (\mu \right )d\mu =1\). To showcase how the above operators simplify notation, take the aggregate expendable income described by Equation 2. Appealing to our definition for sales share, \(y_{i}(\mu )\), we can rewrite this equation as

Rearranging this equation yields a more compact expression for aggregate income:

where \(\widetilde {\mathbb {E}}_{y_{i}}\left [\mu \right ]\) is country \(i\)’s output-weighted harmonic mean markup.

4 Aggregate Welfare Loss from Market Power

The market equilibrium is inefficient, because markups cause relative prices (relative marginal rates of substitution) to diverge from relative marginal costs (relative marginal rates of transformation). More formally,

Our goal is to measure the aggregate welfare loss from

market power. To this end, we begin a formal definition of aggregate welfare in our economic

setting.

Aggregate welfare.\(\quad\) We define aggregate welfare as the utility of the representative consumer.

We can specify this measure for country \(i\) under the factual markups \(\boldsymbol {\mu }\) as

where \(v_{i}(.)\) is the indirect utility function. \(E_{i}=\widetilde {\mathbb {E}}_{y_{i}}\left [\mu \right ]w_{i}L_{i}\) denotes expendable income under the status quo, which is the sum of wage income and profit rebates. \(\mathbf{p}_{i}=\{p_{\omega }\}_{\Omega _{i}}\) is the equilibrium vector of prices in country \(i\), where \(p_{\omega }=\mu _{\omega }c_{\omega }\).

Now, consider a counterfactual equilibrium in which markups are eliminated. This would yield an efficient allocation wherein prices are equal to marginal cost globally: \(\mathbf{p}^{*}=\mathbf{c}^{*}\equiv \{c_{\omega }^{*}\}_{\Omega ^{*}}\). Total expendable income equals merely the wage income, \(E_{i}^{*}=w_{i}^{*}L_{i}\), after this shift. Eliminating markups, modifies the entire vector of wages and, thus, marginal costs, with \(w^{*}\) and \(c^{*}\) denoting the wage and marginal cost under the efficient equilibrium. Welfare under the efficient marginal-cost-pricing allocation is

Aggregate welfare loss from market power.\(\quad\) We define the welfare loss from market power for

country \(i\) as the log welfare distance to the efficient marginal-cost-pricing equilibrium:

It is important to reiterate that the marginal-cost-pricing equilibrium without transfers represents one point on the Pareto efficient frontier. As show in Appendix C this allocation can be rationalized as the solution to a global planning problem under a specific choice of Pareto weights. However, as we will later demonstrate, some countries could be worse off after transitioning from the status quo to marginal-cost-pricing equilibrium, though the weighted sum of global welfare improves.

4.1 Closed Economy Setting

As an intermediate step, we analyze a closed economy setting. This setting is characterized by prohibitively high trade costs (\(\boldsymbol {\tau }\rightarrow \infty\)) implying equality between domestic output and expenditure: \(\lambda _{ii}=1\) and \(\mathbf{y}_{i}=\mathbf{e}_{i}\). The following proposition shows that the aggregate loss from markups in this setting is purely determined by markup dispersion.

Proposition 1.The aggregate welfare loss from market power for a closed economy is

The above formula generalizes the Hsieh and Klenow (2009) formula to a setting endogenous wedges and firm selection effects. It reflects the logic outlined earlier. The inefficiency arising from market power stems from the divergence between relative prices and relative marginal costs. If markups are uniform, they preserve the equality between relative prices and relative marginal costs and, therefore, do not disrupt allocative efficiency—even if they are nonzero.

4.2 Open Economy Setting

Now consider an open economy for which supply and demand are decoupled, \(\mathbf{y}_{i}\neq \mathbf{e}_{i}\), and the domestic expenditure share is strictly less than one, \(\lambda _{ii}<1\), and endogenously determined. We derive a new formula for the welfare loss from market power in this case.

Proposition 2.The aggregate welfare loss from market power for an open economy is

The aggregate welfare loss has three elements under trade relations. The first element, \(\text{MLD}_{e_{i}}\left [1/\mu \right ]\), mirrors the closed economy formula. The second terms captures how markup correction affects the gains from trade. These gains depend on the extent to which markup correction modifies relative international expenditure shares, \(\Delta _{\mu }\ln \tilde {\lambda }_{ii}=\ln \tilde {\lambda }_{ii}(\boldsymbol {\mu };\boldsymbol {\tau })-\ln \tilde {\lambda }_{ii}(\boldsymbol {1};\boldsymbol {\tau })\). And since the within-industry markup distribution is origin-blind, expenditure share changes arise exclusively from shifts in relative wages, which are muted as we confirm quantitatively in later analysis.Formally: \(\Delta _{\mu }\ln \tilde {\lambda }_{ii}=\int _{\boldsymbol {\mu }}^{1}\left (\frac {\partial \ln \tilde {\lambda }_{ii}}{\partial \ln \mathbf{w}}\cdot \frac {\partial \ln \mathbf{w}}{\partial \boldsymbol {\mu }}d\boldsymbol {\mu }\right )\), where \(\frac {\partial \ln \mathbf{w}}{\partial \boldsymbol {\mu }}\) is the wage change in response to markup correction and partial derivative in the integral is \(\frac {\partial \ln \tilde {\lambda }_{ii}}{\partial \ln \mathbf{w}}\cdot \frac {\partial \ln \mathbf{w}}{\partial \boldsymbol {\mu }}=\theta \left [-(1-\tilde {\lambda }_{ii})\frac {\partial \ln w_{i}}{\partial \boldsymbol {\mu }}+\boldsymbol {\tilde {\lambda }}_{-ii}\cdot \frac {\partial \ln \boldsymbol {w}_{-i}}{\partial \boldsymbol {\mu }}\right ].\) Also, this terms is fundamentally distributive: if markups depress relative wages in one group of countries, they inevitably elevate them in others. Thus, \(\Delta _{\mu }\ln \tilde {\lambda }_{ii}\) becomes positive for the former and negative for the latter.

The last term, which represents rent-shifting is the most notable, and largely overlooked by the past literature. To understand the intuition, let us first refer back to the closed economy case: there, profits were rebated to the same consumers whose surplus was negatively impacted by markups. Now, markup could undermine consumer surplus in one location, generating excess profits that are rebated elsewhere. Hence, the loss from market power is elevated or mitigated, depending on whether country \(i\) is a net receiver or a net payer of excess profits to the rest of the world. Consistent with this logic, exposure to profits-shifting effects is determined by a country’s revealed comparative advantage across low versus high-markup goods. Specifically,

where \(Cov\left (.\right )\) is the covariance operator. The above equation states that a country’s exposure to profit-shifting externalities is regulated by its pattern of specialization. Positive exposure results from revealed comparative advantage in high-markup goods, i.e., \(\partial (\frac {y_{i}(\mu )}{e_{i}(\mu )})/\partial \mu >0\). And negative exposure stems from revealed comparative advantage in low-markup goods.

Does trade openness impact the loss?\(\quad\) We define the pure effect of trade as the change relative to the no trade of autarky benchmark. Specifically, for a generic variable \(X\) define the trade-induced change as

where \(X(\boldsymbol {\tau })\) denotes the value of \(X\) under the status quo trade cost levels and \(X(\boldsymbol {\infty })\) denotes the counterfactual level under prohibitive trade costs or autarky.

Our goal is to determine \(\Delta _{\tau }\mathscr {D}_{i}^{\mu }\) using the formulas under Propositions 1 and 2. The markup dispersion term in these formulas is invariant to trade, given our previous result that the markup distribution, \(\widetilde {G}_{k}(\mu )\), and the conditional expenditure share, \(\lambda _{k}(\mu )\), is unaffected by trade costs. The intuition for this invariance is that the pro-competitive effects of on markups at the intensive margin are exactly offset by the selection effects at the extensive margin. Thus, the degree of markup dispersion is unaffected by trade within narrowly-defined industry segments, i.e., \(\Delta _{\tau }\text{MLD}_{e_{i}}\left [1/\mu \right ]=0\).

Instead, trade openness influences the welfare loss from market power in two ways. First, market power distorts international relative prices and the gains from trade in open economies. Second, trade activates the zero-sum profit shifting effects discussed earlier. Formally, the pure effect of trade is

The first term represents the change to the efficiency gains from trade relative to what the gains would have been without markup distortions. The second represents profit-shifting effects.

The Gains from Trade.\(\quad\) While profit-shifting externalities attenuate the gains from trade for some countries, they do not reverse the overall benefits of trade. This point can be formalized using the standard definition of the gains from trade, \(GT_{i}=1-W_{i}(\boldsymbol {\mu };\boldsymbol {\infty })/W_{i}(\boldsymbol {\mu };\boldsymbol {\tau })\). These gains are described by the following formula:

where \(\Lambda _{i}\) represents profit-shifting effects specified by Proposition 2 and \(\tilde {\lambda }_{ii}^{\frac {1}{\theta }}\) denotes the efficiency gains, where \(\tilde {\lambda }_{ii}\equiv \prod _{k}\lambda _{ii,k}^{e_{i,k}}\) is the geometric mean of domestic expenditure shares across industries. Overall, the above formula suggests that profit-shifting magnifies the gains from trade for countries that collect net profits from the rest of the world while diminishing them for others. In principle, rent-shifting effects could large enough to reverse the gains from trade. However, outside of extreme cases, the overall gains should remain positive if \(\theta\) is sufficiently low.

4.3 Extensions

We re-derive the formula for \(\mathscr {D}_{i}\) and \(\Delta _{\tau }\mathscr {D}_{i}\) under free entry, multi-national ownership, input-output linkages, and fixed overhead costs. In the interest of brevity we present a verbal description of each extension here, with detailed derivations provided in the appendix.

\(\left (a\right )\) Free Entry and Rent Dissipation. Our baseline model abstracts from firm entry and the fact that a fraction of profits represents quasi-rents used to cover sunk entry costs. Appendix E demonstrates that even with firm entry, cross-country profit imbalances generate distributive firm-relocation externalities that mirror the profit-shifting effects identified earlier. These relocation externalities, however, arise not from excessive markups but rather from excessive entry of firms into low-markup industries.

Specifically, suppose firms pay a sunk entry cost to develop a blueprint. The number of entrants paying this cost is determined by a free-entry condition that equates variable profits to the entry cost in each industry and country. For simplicity, assume demand exhibits a CES parametrization. We show that a closed economy’s distance to the efficient frontier under free entry is

This formula represents the aggregate welfare loss from inefficient firm entry decisions, which fail to internalize the social benefits of adding new product varieties. The extent of this loss is tied to the degree of markup dispersion: \(\mathscr {D}_{i}^{closed}\approx Var_{e_{i}}[\mu ]\). Trade openness modifies welfare losses through firm-relocation externalities. As demonstrated in Appendix section E, the trade-induced change in \(\mathscr {D}_{i}\) is

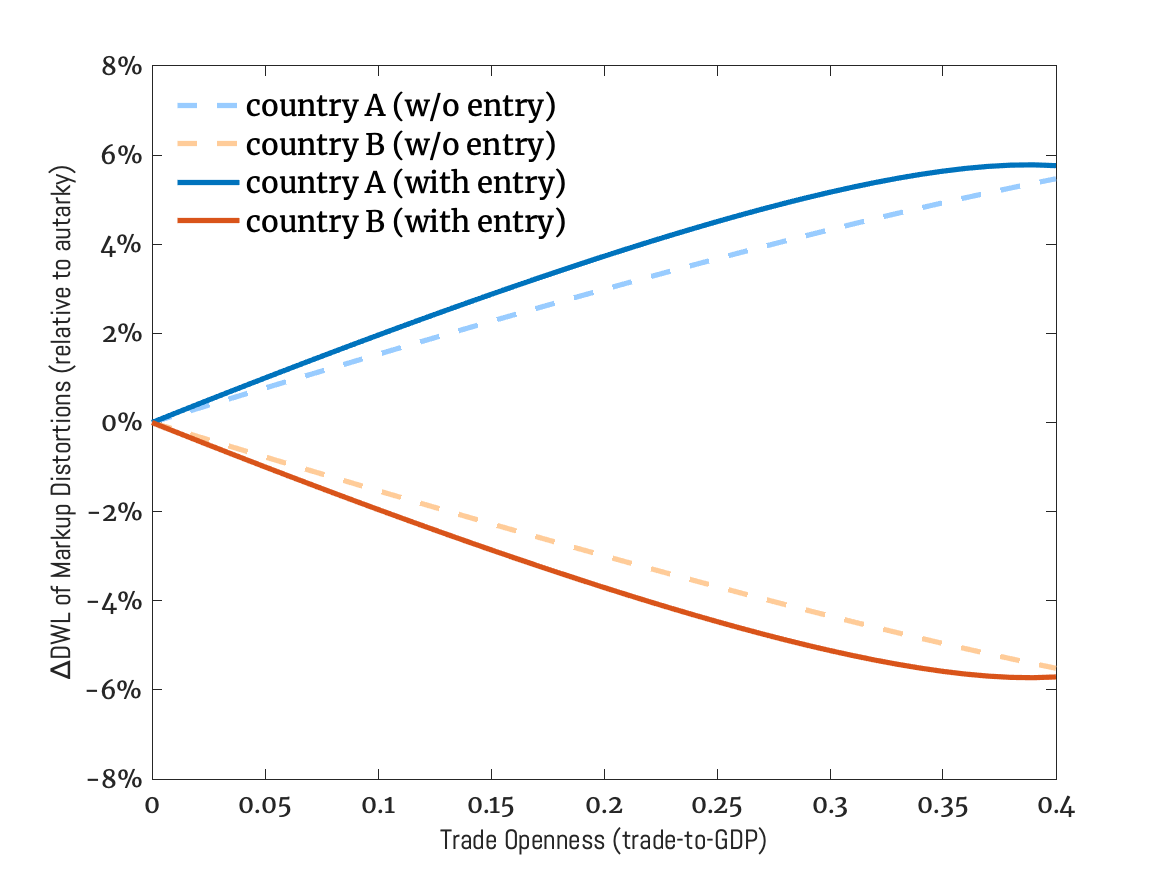

where \(y_{i}^{*}\left (\mu \right )\) denotes the counterfactual output share under the efficient allocation. One can verify that \(y_{i}^{*}\left (\mu \right )/y_{i}\left (\mu \right )\) is increasing in \(\mu\) if a country is a net exporter of high-markup goods, implying that firm-delocation mitigates the loss from entry distortions (i.e., \(\Delta _{\tau }\mathscr {D}_{i}<0\)) for the same countries that benefit from profit-shifting.The argument goes as follows: restoring efficiency entails increasing the relative wage of countries that are net exporters of high-markup goods. The higher wage suppresses demand relatively more for these countries’ output of low-markup goods, since these goods face more price-elastic demand. In other words, firm-delocation effects generate distributive externalities that merely mirror profits-shifting effects.Figure A.6 in the appendix illustrates this point by simulating a generic model featuring two countries. The countries are symmetric except for their revealed comparative advantage in low-markup versus high-markup goods. The simulation demonstrates that under both free and restricted entry, trade openness amplifies the deadweight loss of monopoly distortions for the country that is a net importer of high-markup goods. Conversely, it reduces these costs for the other country. This affirms that monopoly distortions have internationally zero-sum effects, even in scenarios where firm entry dissipates quasi-rents. The underlying logic is that the degree of market power is correlated with entry distortions, and exposure to these distortions mirrors exposure to profit-shifting under restricted entry.

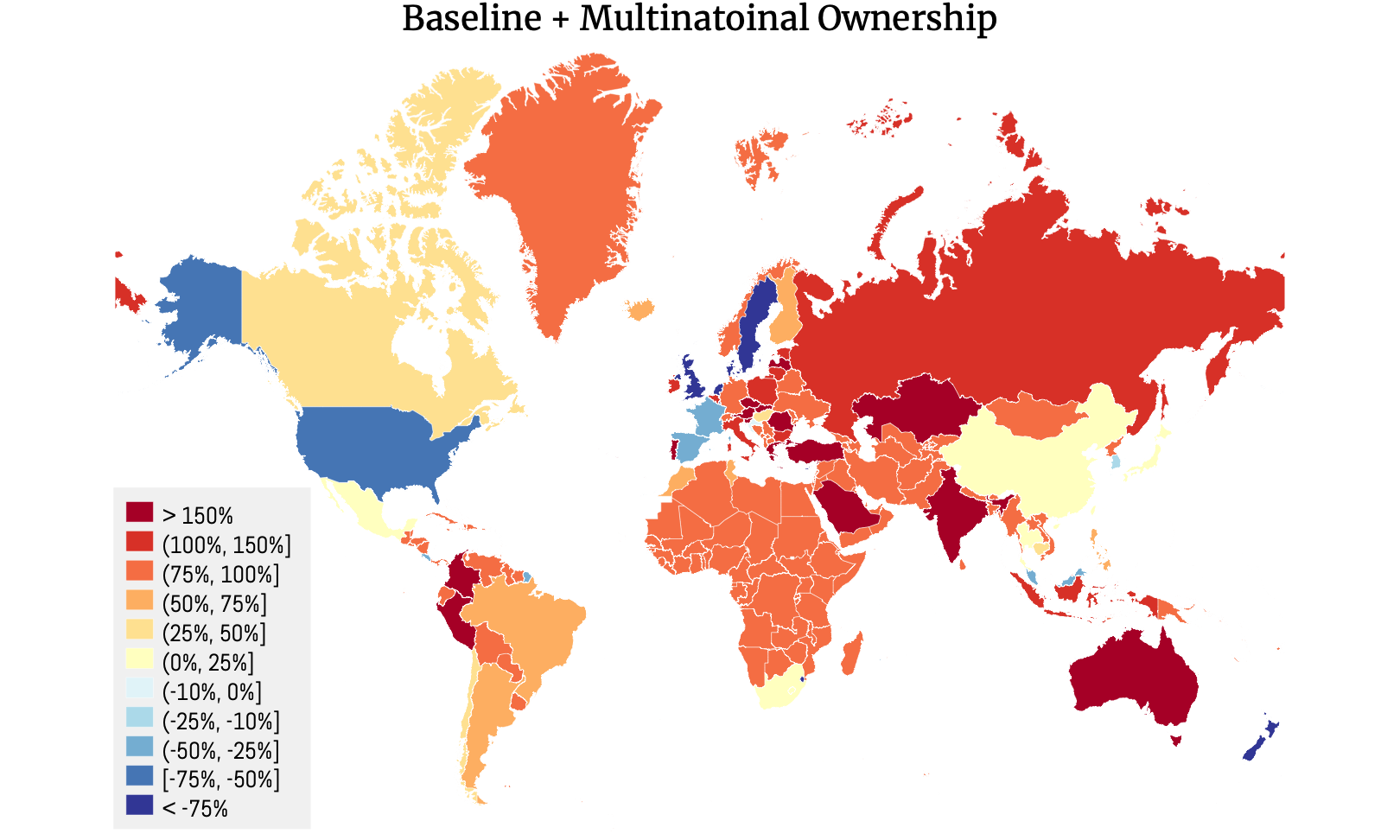

\(\left (b\right )\) Multinational Ownership and Cross-Border Profit Payments. As documented earlier, only a minor fraction of profits are repatriated to foreign shareholders—hence, the abstraction from cross-border profit payments in our baseline model. However, we can easily extend our baseline formulas to account for such payments. Appendix F derives updated formulas for \(\Delta \mathscr {D}_{i}\), under the condition where a constant share \(\pi _{ni}\) of country \(n\)’s profits are repatriated to international shareholders in country \(i\). The new formula for \(\Delta \mathscr {D}_{i}\) features an additional term that accounts for the cross-border profit payments to foreign shareholders. More formally,

The last term in the above equation represents the net inflow of repatriated profits for country \(i\), calculated as the difference between the inflow and outflow of such profits. Importantly, the semi-parametric model allows us to evaluate this term using aggregate profit ownership shares, denoted as \(\left \{ \pi _{ni}\right \} _{n,i}\), which can be inferred from firm-level ownership data. The calculation also requires data on industry-level output and expenditure shares and the sales-weighted average markup for each industry, as in our baseline model.

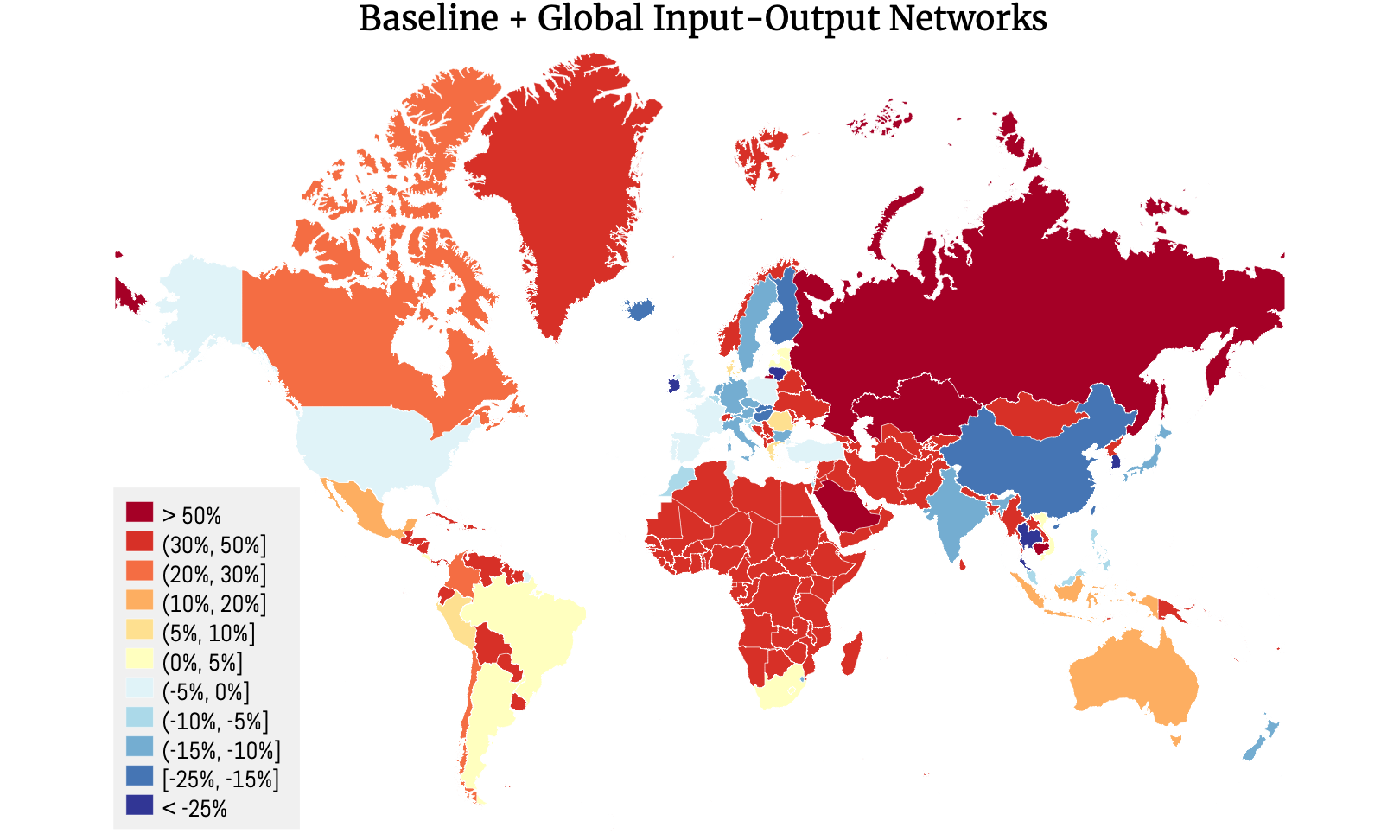

\(\left (c\right )\) Global Input-Output Networks. Appendix H examines a global economy in which production relies on labor and internationally traded intermediate inputs. In this extension, the magnitude of international profit-shifting depends on the degree to which the markup paid on imported inputs is re-exported and passed on to foreign consumers after production. As a result, the formulas that describe the impacts of trade on the national-level incidence of monopoly distortions depend on the elements of the global input-output matrix. We present these sufficient statistics formulas in Appendix H and observe that the core logic from our baseline model continues to hold. Specifically, trade intensifies the incidence of monopoly distortions for countries that are net exporters of high-markup goods while reducing it for others, where net exports now take into account global input-output linkages.

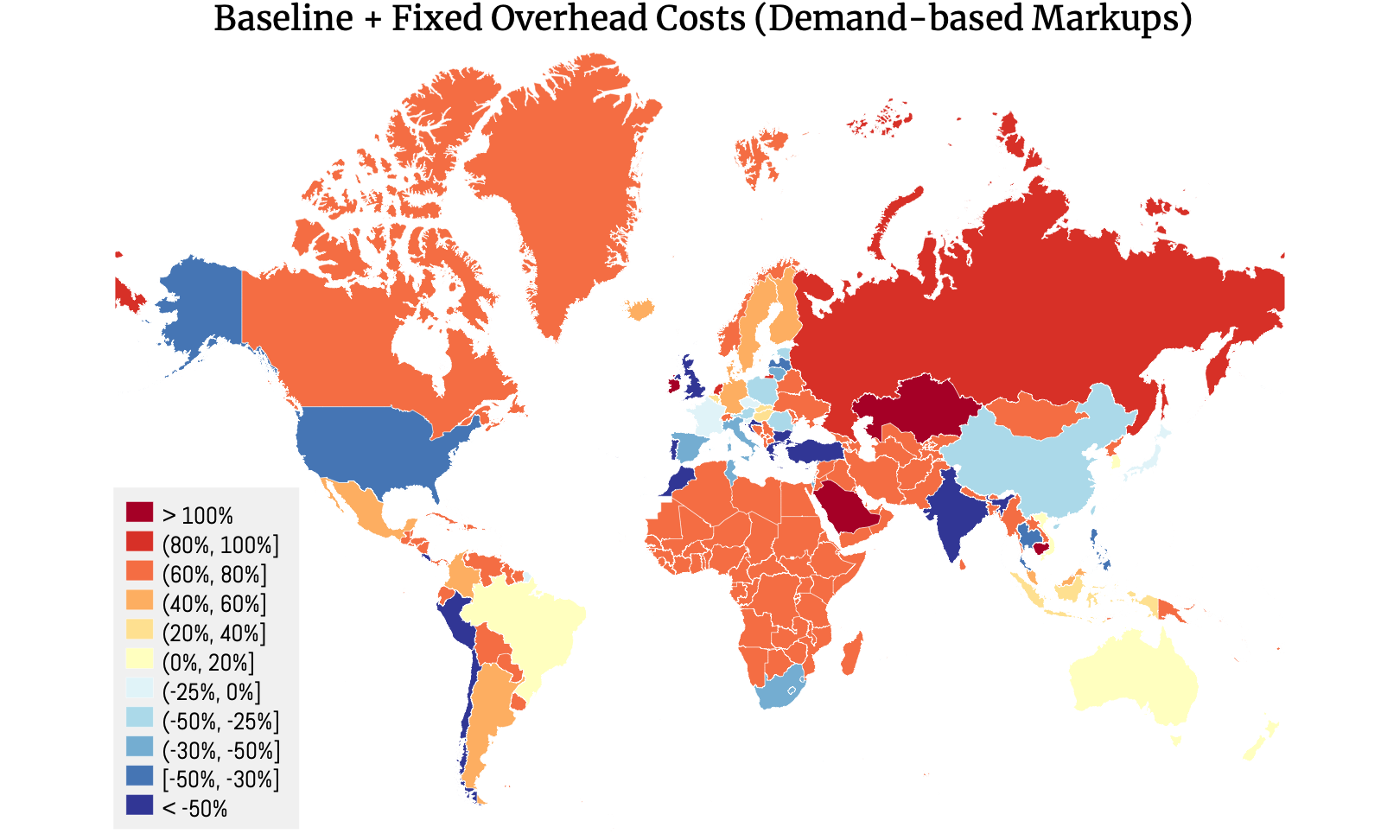

\(\left (d\right )\)Accounting for Fixed Overhead Costs. Earlier, we showed that considering sunk entry cost payments does not eliminate the zero-sum welfare effects associated with market power. In Appendix I, we explore how accounting for fixed overhead costs affects the zero-sum international profit-shifting effects. Specifically, we analyze a global economy where serving individual markets requires paying a fixed cost that consumes a portion of the profits. We provide updated formulas for calculating the welfare loss from market power, isolating how trade alters these costs. Our updated formulas demonstrate that a country’s exposure to international profit-shifting in the presence of fixed overhead costs is influenced by two factors: the shape of the firm productivity distribution and how this industry-specific shape parameter correlates with a country’s net exports. These factors determine the net profits paid to the rest of the world via fixed cost payments.

5 Duality Between Tariffs and Markups

This section shows that, for sufficiently open economies, markups function as a shadow tariff. The general idea is that both markups and tariffs introduce a local efficiency loss to extract excess surplus in the form of government revenues or profits from the rest of the world. Both wedges, therefore, have similar aggregate welfare effects. To formalize this point, we first define the general equilibrium under tariffs and markups.

General Equilibrium with Tariffs.\(\quad\) Suppose that the price of every variety \(\omega \in \Omega _{i}\) available to consumers in country \(i\) includes an additional wedge that is applied specifically to imported varieties:

We focus on uniform tariffs, as the optimal tariff is uniform absent markup wedges. That is, the uniform tariff outperforms any heterogeneous tariff schedule for country \(i\), starting from the efficient-pricing schedule.The uniformity of optimal tariffs is a general result that holds across a wide class of constant-returns to scale quantitative trade models, in which labor is the only primary production factor and labor market are non-segmented within countries. Tariffs also generate revenues to the amount of \(\frac {t_{i}}{1+t_{i}}(1-\lambda _{ii})E_{i}\), where \((1-\lambda _{ii})E_{i}\) is total import expenditure. Total expendable income inclusive of tariff revenues is

where \(\lambda _{ii}=\sum _{k}e_{i,k}\lambda _{ii,k}\) is the aggregate domestic expenditure share, aggregate over all industries. The industry-level aggregate expenditure shares are described by the gravity equation adjusted for tariffs:

Lastly, since the economy is plagued with additional distortive wedges, we specify aggregate welfare as an explicit function of both markups and tariffs: \(W_{i}(\boldsymbol {\mu },\mathbf{t};\boldsymbol {\tau })=v_{i}(E_{i},\mathbf{p}_{i})\). Let \(\boldsymbol {\mu }_{i}\equiv \{\mu _{\omega }\}_{\cup _{n}\Omega _{in}}\subset \boldsymbol {\mu }\) denote the subset of markups applied by firms located in country \(i\). With a slight abuse of notation we hereafter use

to denote welfare under a choice of local markups and tariffs given markups and tariffs in the rest of the world.

Intermediate Equivalence Results.\(\quad\) Our goal in this section is to establish a duality between decentralized markups and a centralized uniform tariff. To this end, we begin by presenting an intermediate equivalence result that connects the factual heterogeneous markup schedule and a uniform tariff to fictitious semi-uniform markup schedules.

Lemma 1.For country \(i\): (a) The semi-uniform markup schedule \(\{\mu '_{\omega }\}_{\Omega }\), where

(b) a uniform tariff \(t_{i}\) is equivalent to a uniform markup \(\mu _{\omega }=1+\mathbb {{1}}_{\omega \notin \Omega _{ii}}t_{i}\) applied exclusively to goods produced in country \(i\) and exported abroad.

The intuition behind the lemma is straightforward: the markups assigned to export goods affect aggregate welfare, \(W_{i}=v(Y_{i},\tilde {\mathbf {p}}_{i})\), only through their impact on aggregate income \(Y_{i}\). The lemma shows that replacing export-side markups with semi-uniform industry-wide markups preserves the global wage vector and aggregate profits, and therefore leaves aggregate income unchanged. Domestic prices are also unaffected, \(\tilde {\mathbf {p}}_{i}=\{\mu _{\omega }\}_{\Omega _{i}}\), since markups and wages remain the same for goods sold in the domestic market. The second part of the lemma essentially reflects the Lerner Symmetry: a uniform import tariff is equivalent to a uniform export-side markup, as such a markup functions like a uniform export tax from an aggregate perspective.

Unilaterally-optimal firm markups.\(\quad\) Define the unilaterally-optimal markup schedule that maximizes country \(i\)’s aggregate welfare as

Note that \(\boldsymbol {\mu }_{i}^{*}\) is inefficient from a global standpoint as it does not internalize the welfare externalities of \(\boldsymbol {\mu }_{i}\) on other countries. In fact, as discussed earlier, the socially-optimal markup from a global standpoint is zero.

Our first result characterizes the unilaterally-optimal markup without imposing any uniformity restrictions. It shows that the optimal markup is zero for goods sold in the domestic market, but exceeds decentralized markups for exported goods, and features limit pricing for marginal products.

Lemma 2.The unilaterally-optimal markup schedule for country \(i\) is

The optimal markup on goods sold domestically is zero because such markups distort domestic consumption and transfer surplus from domestic consumers to domestic firms, resulting in a net deadweight loss. In contrast, export-side markups distort prices faced by foreign consumers and transfer surplus from abroad to domestic firms. From an aggregate perspective, the government acts as a multi-product monopolist and thus has an incentive to raise markups on export goods. However, increasing these markups risks pricing some marginal export goods above the foreign choke price. As a result, the markup is set to the limit-pricing level for marginal goods.

Unilaterally-optimal macro markups.\(\quad\) Now we impose uniformity restrictions on markups to characterize the unilaterally-optimal macro markup, which is formally defined as

The added restriction imposes that a common markup be applied to all goods supplied to market \(n,k\). The motivation behind this restriction is that decentralized markups on export goods mimic a macro markup per Lemma 1. We basically want to show that the decentralized markups are not necessarily optimal from an aggregate standpoint. The following lemma states this result.

Lemma 3.The unilaterally-optimal macro markup, involves no markup on domestically-sold goods and a uniform industry-blind markup on exported goods:

Together, Lemmas 1 and 3 state that there exists a uniform tariff that strictly outperforms factual markups from an aggregate welfare standpoint. If we show that there exist a tariff that yields a strictly greater welfare loss than the factual markups, then we can use the Intermediate Value Theorem to prove the existence of a tariff rate that exactly replicates the aggregate welfare effects of markups. For this, we appeal to our previously-derived formulas for the gains from trade and the welfare loss from markups. Since the markup distribution is Pareto, the welfare loss from markups is bounded from above. However, if country \(i\) is sufficiently open, the losses from prohibitive tariffs, \(t_{i}\rightarrow \infty\), can grow arbitrarily large as \(\theta\) is lowered. Under these conditions, prohibitive tariffs exert a cost greater than factual markups. Thus, the Intermediate Value Theorem states that there exists a tariff \(\check {t}_{i}\) that yields the same aggregate welfare level as the decentralized markups, \(\boldsymbol {\mu }_{i}\), under the status quo.

Proposition 3.Suppose factual trade barriers (\(\boldsymbol {\tau }\), \(\mathbf{t}\)) are sufficiently low and \(\theta\) is sufficiently small. Then, markups function as shadow tariffs: There exists a centralized shadow tariff (\(\check {t}_{i}\)) that replicates the aggregate welfare effects of decentralized markups:

The above proposition establishes a local duality between tariffs and monopolistic markups, stating that a tariff can replicate the aggregate welfare effects of decentralized markups charged by firms in that country. However, our forthcoming quantitative analysis reveals an even stronger duality. We identify a global vector of tariffs that replicates the welfare loss from markups globally.

Understanding the markup-tariff duality.\(\quad\) Below we elucidate Proposition 3 by drawing parallels between the trade-off faced by unilateral markups and tariffs. Following Proposition 2, we can decompose the welfare effects of unilateral markups as

The first term is strictly positive because country \(i\) is a net collector of profits from abroad under \(\boldsymbol {\mu }_{i}\) alone. The remaining two terms represent the local efficiency loss from markups. Markups distort relative prices domestically, the loss from which captured by \(MLD_{e_{i}}[1/\mu ]\). They also distort relative prices internationally, leading to a potential reduction in the gains from trade,\(\frac {1}{\theta }\,\Delta _{\mu }\ln \tilde {\lambda }_{ii}\). All in all, the decomposition reveals that decentralized markups impose a local efficiency loss but also extract and transfer excess surplus (profits) from foreign households to the home economy.

Next, consider the aggregate welfare effects of a unilaterally applied uniform tariff \(t_{i}\). Starting from the efficient marginal-cost-pricing equilibrium, the welfare effect of the tariff can be written as

The first term represents excess revenue collected on imports and is strictly positive, where \(\lambda '_{ii}\equiv \lambda _{ii}+\Delta _{t}\lambda _{ii}\) denotes the post-tariff expenditure share. The second term captures the local efficiency loss arising from trade contraction. In line with the textbook optimal-tariff argument, if the revenue gain exceeds the associated efficiency loss, country \(i\) can unilaterally benefit from imposing a tariff. The logic mirrors that for markups: tariffs create a local efficiency loss to extract surplus from foreign producers.

Implications for Trade Reciprocity.\(\quad\) Casting markups as a shadow tariff has two immediate implications. First, it reveals that the monopolistic pricing behavior of firms can be viewed as a decentralized form of terms of trade manipulation, resembling tariffs imposed by a central government. This insight suggests that governments seeking to manipulate the terms of trade, but constrained by international commitments, may choose to refrain from regulating anti-competitive practices to not disrupt the implicit terms of trade benefits. Second, by converting profit-shifting externalities into equivalent tariff measures, we can identify policy solutions that are enforceable under existing trade agreements, as these agreements are designed to discipline explicit border policy measures. For instance, under the World Trade Organization (WTO), tariffs must adhere to the principle of reciprocity (Bagwell and Staiger (1999)). Proposition 3 implies that unilateral tariff concessions could effectively neutralize profit-shifting externalities by simply invoking the reciprocity principle within the WTO framework.

6 Mapping Theory to Data

Calculating the aggregate loss from markups requires the following sufficient statistics: the sales-weighted average markup by industry and aggregate expenditure and sales shares (\(e_{i,k}\), \(y_{i,k}\)). Specifically, the profit shifting term is

where \(\mathbb {\widetilde {E}}_{\lambda _{k}}\left [\mu \right ]\) is the harmonic mean sales-weighted average markup in industry \(k\), which is common across locations. Therefore, it can be calculated by pooling the entire sample of global firms within a narrowly defined industry \(k\) and computing the mean using the global sample.Likewise, the mean log deviation term could be recovered as \(\emph {MLD}_{e_{i}}[1/\mu ]=\mathbb {E}_{e_{i}}\left [\ln \mu \right ]-\ln \tilde {\mathbb {E}}_{e_{i}}\left [\mu \right ]\), where \(\mathbb {E}_{e_{i}}\left [\ln \mu \right ]=\sum _{k}e_{i.k}\mathbb {E}_{\lambda _{k}}\left [\ln \mu \right ]\) and \(\tilde {\mathbb {E}}_{e_{i}}\left [\mu \right ]=\left [\sum _{k}e_{i,k}\tilde {\mathbb {E}}_{\lambda _{k}}\left [\mu \right ]^{-1}\right ]^{-1}\).

In more complex environments, we also need multi-national profits ownership shares (\(\pi _{in}\)) and aggregate input-output shares. Among these statistics, markups must be estimated, while the rest are directly observable. We source the aggregate shares from the OECD INTER-COUNTRY INPUT-OUTPUT (ICIO) TABLES, which cover 64 major countries and 36 sectors from 2005 to 2015. We construct original data on profit ownership shares using ORBIS, which we detail in the following section.

Since profit-shifting effects are distributive by nature, we are interested in whether they disproportionately affect high-income vs low/middle income countries. To this end, we classify the 64 countries in our sample into a low/middle income or high-income category based on the UNITED NATIONS COUNTRY CLASSIfiCATION. Table A.3 presents the complete list of countries in our sample along with their respective income status. It is important to note that our sample also includes an aggregate of the rest of the world, which mostly represents low-income countries and is classified accordingly.

6.1 Multi-National Profit Ownership Shares

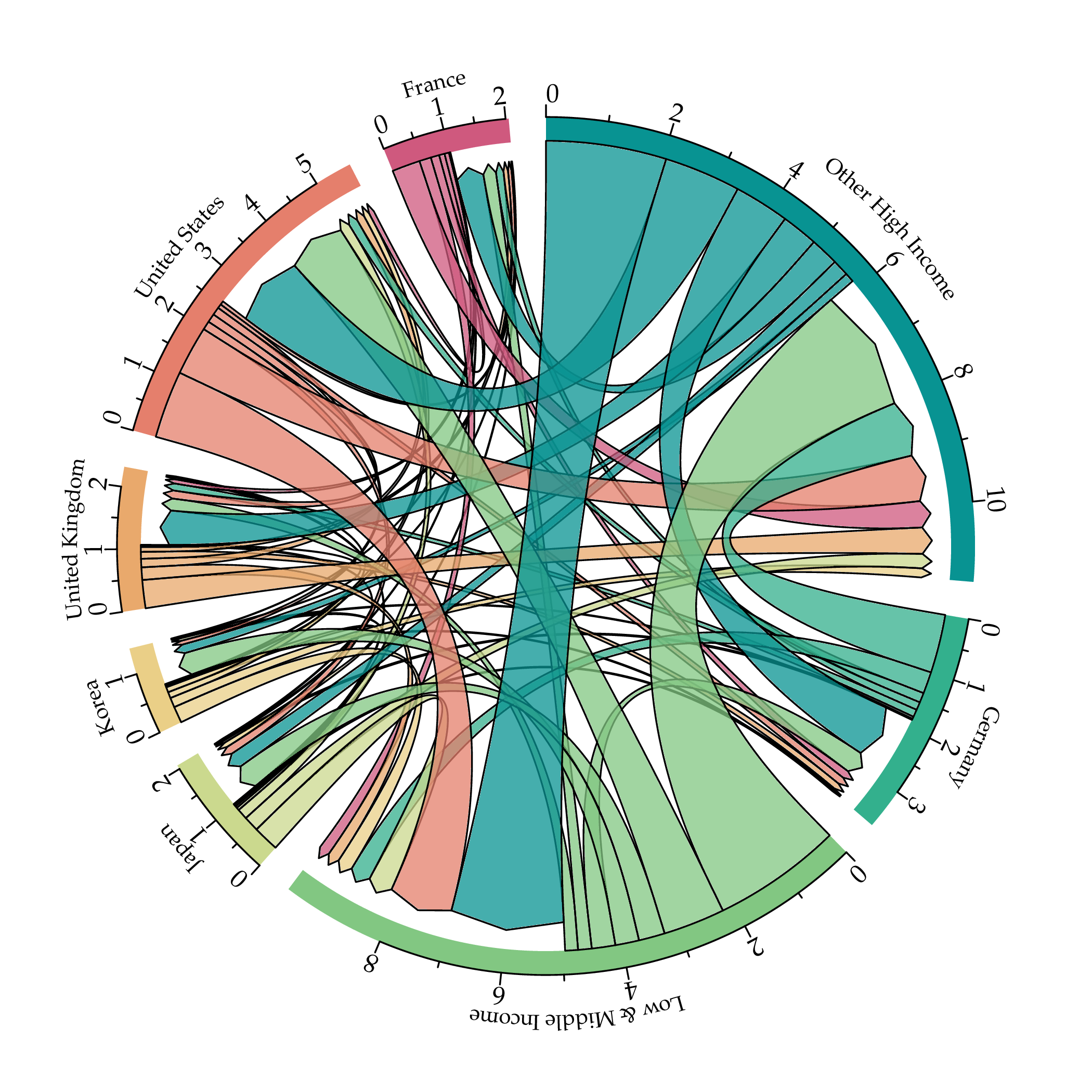

We assemble data on profit ownership shares, \(\left \{ \pi _{in,t}\right \}\), using the ORBIS database provided by BUREAU VAN DIJK (BVD). We first clean and refine the data using the algorithm described in Appendix A. The cleaned dataset forms a panel consisting of 3,075,899 firms globally from 2005 to 2015. For each firm \(\omega\) in this sample, we have information on its gross profits, denoted as \(\pi _{\omega }\), in year \(t\), where the subscript \(i\) represents the country in which the firm’s operation is based. Additionally, we observe the firm’s equity share associated with shareholders located in country \(n\), denoted as \(\kappa _{\omega n}\in (0,1]\). Using this information, we calculate the share of country \(i\)’s profits repatriated to country \(n\) in year \(t\) via equity financing using the following formula:

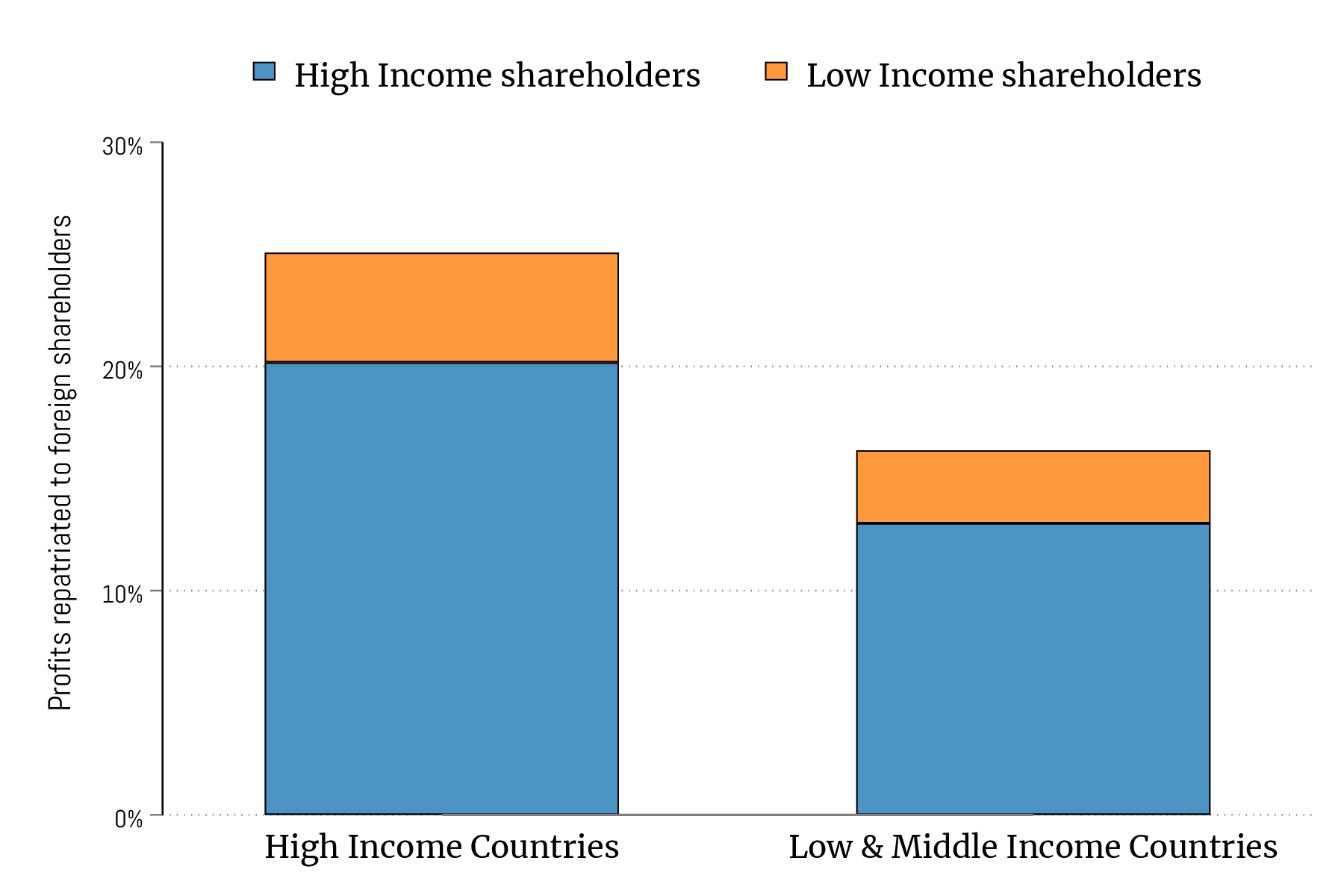

where \(\Omega _{i,t}\) denotes the set of firms operating in country \(i\) in year \(t\) in our sample. By applying this formula for each triplet \(\left (i,n,t\right )\), we obtain square matrices of bilateral profit ownership shares for each year in 2005-2015 that are compatible with ICIO tables. Table 2 in the appendix provides an overview of multinational profit ownership. For each country, it reports the share of profits retained in the country of origin, repatriated to high-income countries, and repatriated to low/middle-income countries.

A first glance at our data reveals that the majority of profits are distributed to domestic shareholders, with only a small portion being repatriated to foreign shareholders, primarily in high-income countries. Over 85% of the profits earned by firms are distributed within the country of origin, and this percentage is even higher among high-income countries. The remaining profits are primarily repatriated to foreign shareholders located in high-income regions. These patterns suggest that repatriated profits contribute to transfer of profits from low and middle-income countries to high-income nations, amplifying the profit-shifting effects due to trade-led specialization.

6.2 Global Markup Estimation

We estimate markups using two different approaches: The cost-based approach and the demand-based approach. While both approaches are well-understood, their macro-level implications have been rarely contrasted. In part, because the demand-based approach has proven difficult to implement at scale across a wide range of countries and industries.

6.2.1 Demand-Based Markup Estimation.

Markups can be recovered from demand elasticities, but demand estimation at scale presents several challenges. First, we must impose parametric assumptions to make progress. To navigate this issue without loss of generality, we estimate a mixed multinomial logit model (MMNL) which can approximate our semi-parametric demand system as closely as possible.This claim follows from Thisse and Ushchev (2016), who show that the homothetic with an aggregator demand system can be alternatively derived from a random utility model; and from McFadden and Train (2000) who establish that any random utility model can be approximated as closely as needed by the MMNL model. Second, the conventional approach to estimating the MMNL model, introduced by Berry et al. (1995, BLP hereafter), is computationally demanding, making it impractical to perform over thousands of product categories. To tackle this issue, we employ a log-linear approximation of the MMNL model proposed by Salanié and Wolak (2019), which is considerably simpler to estimate. The final difficulty lies in the data requirements for large-scale demand estimation. The standard BLP approach leverages data on observable product characteristics to achieve identification, but globally representative data on observed product characteristics is unavailable. We overcome this obstacle by leveraging high-frequency trade and exchange rate data to guide identification, eliminating the need for data on product characteristics.

Before diving into our estimation strategy, let us provide a high-level overview of the MMNL model, which forms the foundation of our estimation. Consider a market populated by an infinite number of households, each of which chooses one product variety from the set \(\Omega _{kt}\) of products available in industry \(k\) in year \(t\). There is also an outside good, the indirect utility of which is normalized to 0. Assuming that the idiosyncratic taste for product varieties is distributed iid according to a type-I Extreme Value distribution with scale parameter 1, the market share of variety \(\omega \in \Omega _{kt}\) can be specified as

In this equation, \(\mathbf{X}\) represents a vector of observed product characteristics, such as prices, and \(\overline {\boldsymbol {\beta }}\) denotes the mean coefficients on these characteristics. \(\boldsymbol {\epsilon }\) is a random coefficient that follows an iid distribution \(N\left (0,\boldsymbol {\Sigma }_{kt}\right )\), where \(\boldsymbol {\Sigma }_{kt}\) is a diagonal variance matrix.More specifically, the utility of household \(h\) derives from purchasing variety \(\omega\) is \(\left (\overline {\boldsymbol {\beta }}_{kt}+\boldsymbol {\epsilon }_{h,kt}\right )\cdot \mathbf{X}_{\omega t}+\xi _{\omega t}+u_{\omega t}\left (h\right )\), where \(u\) accounts for idiosyncratic heterogeneity in taste for product varieties, which is distributed iid according to a type-I Extreme Value distribution with scale parameter 1. The demand shifter, \(\xi\), captures unobserved product characteristics, such as perceived product quality at the market level. The BLP approach to estimating demand recovers \(\boldsymbol {\xi }\) by inverting the market share equation and using the recovered values to enforce the moment condition \(\mathbb {E}\left [\Delta \boldsymbol {\xi }\mid \mathbf{z}\right ]=0\), where \(\mathbf{z}\) represents a set of price instruments. The inversion approach, however, is computationally challenging, particularly for large-scale applications. To overcome these computational hurdles, Salanié and Wolak (2019) propose an alternative approach that approximates \(\boldsymbol {\xi }\) using the following equation:

where \(\tilde {\boldsymbol {\Sigma }}_{kt}=\text{Tr}\left [\boldsymbol {\Sigma }_{kt}\right ]\) and \(\mathbf{K}\) is an artificial regressor whose elements are:

Following this approach and omitting higher-order terms, we obtain an approximated value for \(\xi\), denoted by \(\check {\xi }\). We then estimate the demand parameters by exploiting the moment condition \(\mathbb {E}\left [\Delta \check {\xi }\mid \mathbf{z}\right ]=0\), which is similar to running a linear 2SLS regression.We instrument \(\Delta K_{\omega t}\) using the number of alternative product codes served by the firm in a year as an additional instrument. See Appendix K for more details. Given that \(\ln p\subset \mathbf{X}\), markups are recovered as \(\mu _{\omega t}=\frac {\partial \ln \lambda _{\omega t}}{\partial \ln p_{\omega t}}(1+\frac {\partial \ln \lambda _{\omega t}}{\partial \ln p_{\omega t}})^{-1}\), assuming single-product and profit-maximizing firms.

The next challenge is finding a valid instrument to guide identification with limited data on observed product characteristics. Our dataset reports three observable characteristics: the country of origin, the product classification used by the statistical agency, and the unit price (\(p\)). The demand residual conditional on these characteristics, \(\tilde {\xi }\), is presumably contaminated with omitted variables correlated with \(p\)—unlike small-scale estimations like BLP, where \(\xi\) is purged from a wider range of observable product characteristics using richer data. To overcome this identification challenge, we leverage high-frequency transaction data and interact it with high-frequency exchange rate data to construct a granular shift-share instrument for \(\ln p\) that measures the exposure to exchange rate fluctuations at the variety level and is uncorrelated with \(\tilde {\xi }\). We begin with the observation that the year-over-year change in the unit price of variety \(\omega\) can be approximated by the sales-weighted average of monthly price changes: \(\Delta \ln p_{\omega t}=\sum _{m\in \mathbb {M}_{t}}\lambda _{\omega t}\left (m\right )\Delta \ln p_{\omega t}\left (m\right )\), where \(\lambda _{\omega t}\left (m\right )\) and \(p_{\omega t}\left (m\right )\) denote month \(m\)’s share of export sales and the year-over-year change in export prices in month \(m\) of year \(t\) (i.e., \(m\in \mathbb {M}_{t}\)). Since \(p_{\omega t}\left (m\right )\) is denominated in the destination market’s currency, it varies with the year-over-year change in the exchange rate between variety \(\omega\)’s origin country and the destination market it serves in month \(m\), denoted as \(\mathscr {E}_{t}\left (m\right )\). Motivated by this accounting relationship, we construct the shift-share instrument: \(z_{\omega t}=\sum _{m\in \mathbb {M}_{t}}\lambda _{\omega t-1}\left (m\right )\Delta \ln \mathscr {E}_{t}\left (m\right )\). This instrument interacts the lagged export share \(\lambda _{\omega t-1}\left (m\right )\) with the concurrent exchange rate change per month to measure variety-level exposure to aggregate exchange rate fluctuations. The exposure measure \(z\) is uncorrelated with \(\tilde {\xi }\) under the identifying assumption that aggregate exchange rate fluctuations and past export composition are independent of unobserved concurrent demand shocks.

Our estimation uses the universe of import transactions for Colombia from 2007 to 2016. The dataset encompasses over 93,000 firms from 251 different countries and reports high-frequency transaction-level sales and quantities for individual firms exporting to Colombia at the Harmonized System 10-digit product level. We complement this data with matching high-frequency exchange rate data from the Bank of Canada for the same time period. To fully leverage the granularity of our data, we conduct our estimation using market share and price data for 10-digit product categories. However, to ensure compatibility between our estimated markups and the level of aggregation in the ICIO data, we pool all 10-digit product categories and estimate demand parameters at the ICIO industry level. Appendixes A and K provide further details about our data and estimation methodology.

6.2.2 Cost-Based Markup Estimation.

Our cost-based approach to markup estimation closely follows De Loecker and Warzynski (2012).We should note that the identifying assumptions underlying this approach align more closely with our extended model, which explicitly incorporates intermediate inputs (see Appendix H). This extended model is used for the quantification presented in the next section. It builds on the observation that firm markups can be calculated based on cost minimization as \(\mu _{\omega }=\alpha _{\omega }p_{\omega }q_{\omega }/\mathcal {C}_{\omega }\) for \(\omega \in \Omega _{kt}\), where \(\mathcal {C}_{\omega }\) denotes the variable inputs cost and \(\alpha _{\omega }\) is the firm-level output elasticity with respect to variable inputs. Since estimating the output elasticity at the firm level is practically infeasible, the standard approach to markup estimation recovers the output elasticity under the simplifying restriction that all firms within product category \(k\) use the same production function. Under this restriction, we can estimate the industry-wide output elasticity (\(\alpha _{\omega }\coloneqq \alpha _{kt}\) for all \(\omega \in \Omega _{kt}\)) using the control function approach in Olley and Pakes (1996).In the first stage, we purge output of measurement error and unanticipated shocks by regressing it on a second-order polynomial of inputs and investment. In the second stage, we estimate the output elasticities by fitting an AR(1) process for productivity and leveraging moment conditions that impose orthogonality between implied productivity and lagged variable inputs and current capital inputs. The estimation uses firm-level financial accounts data from COMPUSTATNorth America. The data is reported based on the SIC industry classification. So, we concord SIC industries into the 36 ICIO industries to mach our macro-level trade and production data. For each industry and year during the 2005-2015 period, we separately estimate the output elasticity using the control function method. Since panel data are required for the control function estimation, we employ 5-year rolling windows, assigning the elasticity estimates derived from data in years \(t-2\) to \(t+2\) the central year \(t\). Since balance sheet data record expenditure and sales rather than physical quantities, the structural error term in the production function is contaminated with unobserved prices shifter such as markups. Following De Loecker et al. (2020), we control for unobserved markups using firms’ sales shares within industries.

We then compute firm-level markups using internationally-representative data from the WORLDSCOPE GLOBAL DATABASE. The data reports the cost of variable inputs \(\mathcal {C}_{\omega }\) and sales \(p_{\omega }q_{\omega }\) across 71,546 publicly traded firms from 134 countries during the 2005 -2015 period. Some firms in this database operate in more than one industry, but we do not observe the breakdown of firm-level sales and costs by industry. To handle this, we assume that sales and costs are equally spread across different products. Following De Loecker and Eeckhout (2018), we assume that the output elasticity is the same across countries. Letting \(\hat {\alpha }_{kt}\) denote the estimated output elasticity in industry \(k\), we calculate the markup charged for variety \(\omega \in \Omega _{kt}\) as \(\mu _{\omega }=\hat {\alpha }_{kt}p_{\omega }q_{\omega }/\mathcal {C}_{\omega }\). We then compute the harmonic sales-weighted average markup in industry \(k\) as \(\widetilde {\mathbb {E}}_{\lambda }\left [\mu \right ]=\left [\sum _{\omega \in \Omega _{kt}}\lambda _{\omega }\mu _{\omega }^{-1}\right ]^{-1}\), where \(\lambda _{\omega }\) is firm \(\omega\)’s sales share within \(\Omega _{kt}\). Figure A.7 in the appendix reports \(\widetilde {\mathbb {E}}_{\lambda }\left [\mu \right ]\) derived from our cost-based markup estimates across various ICIO industries.

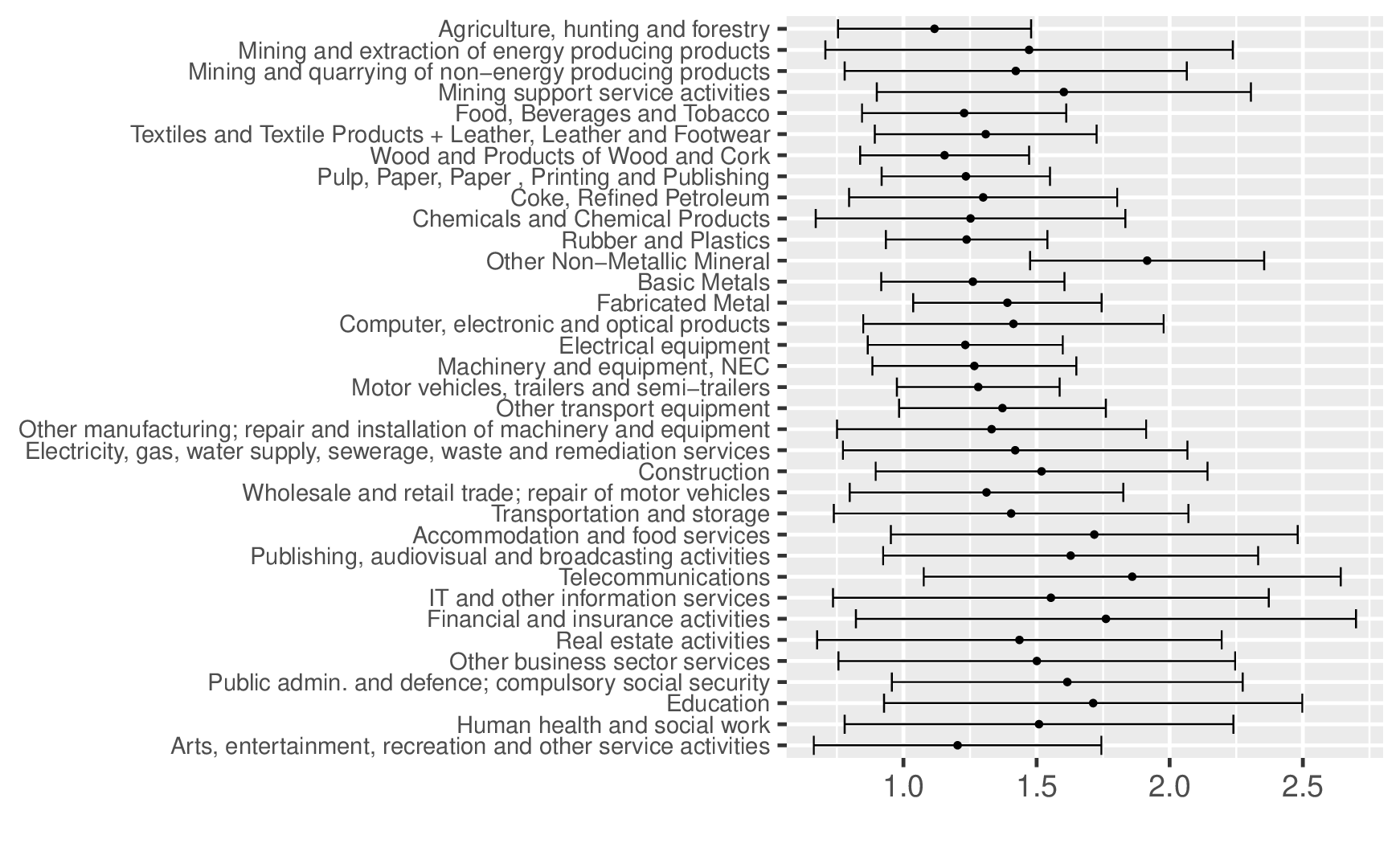

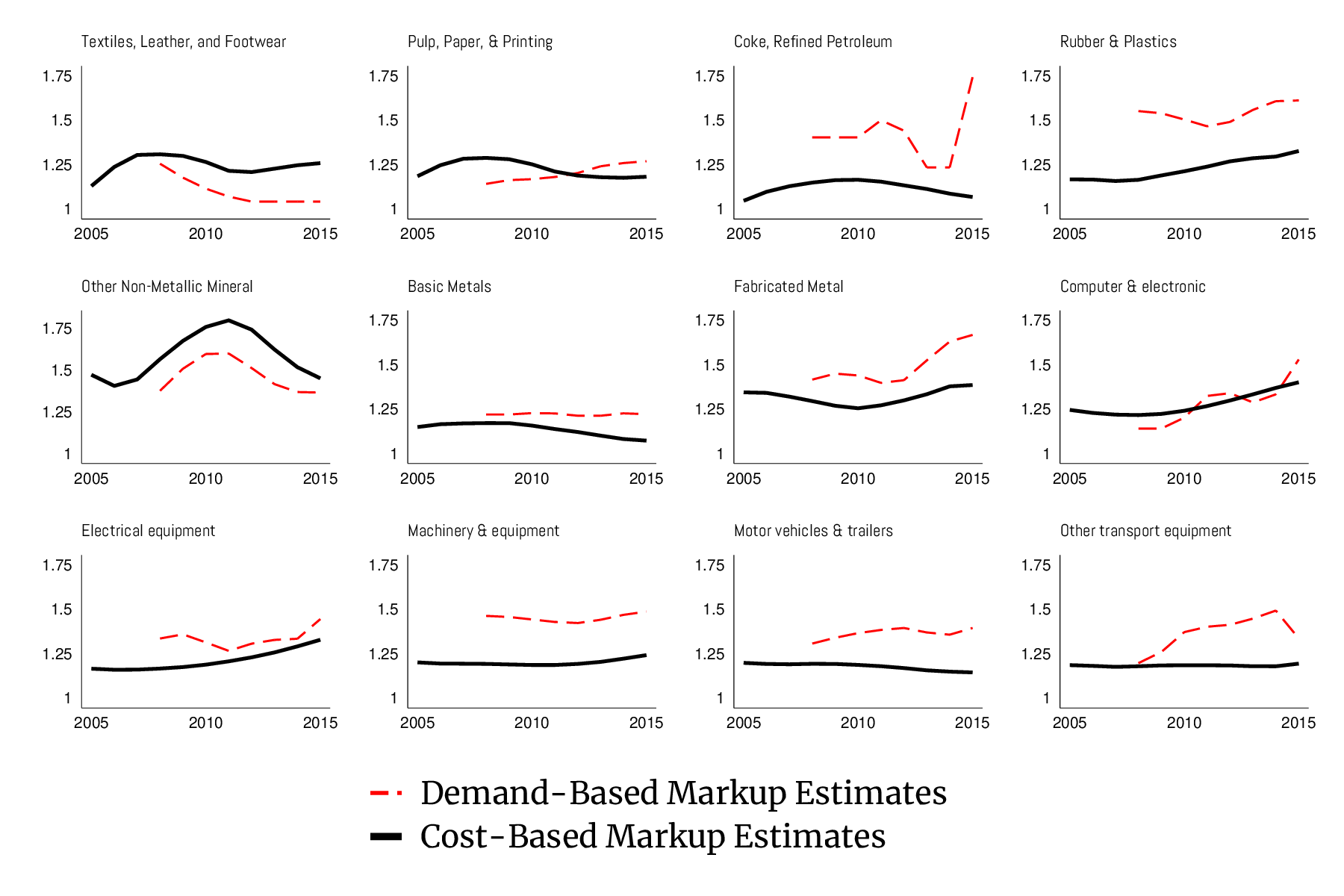

Estimation results. Figure 3 displays the estimated markups for select manufacturing industries during 2005-2015, based on both demand-based and cost-based approaches. The graph displays the arithmetic sales-weighted average markup for each industry in a given year. Since our transaction-level import data begins in 2007, our demand-based markup estimates (which are obtained from a first-difference estimator) cover years after 2008. As anticipated, there are some discrepancies between the demand-based and cost-based markup values. However, in many industries, the demand- and cost-based markup estimates closely track each other over time. As we show next, both markup estimates yield starkly similar macro-level predictions about the loss from market power and the role of trade specifically.

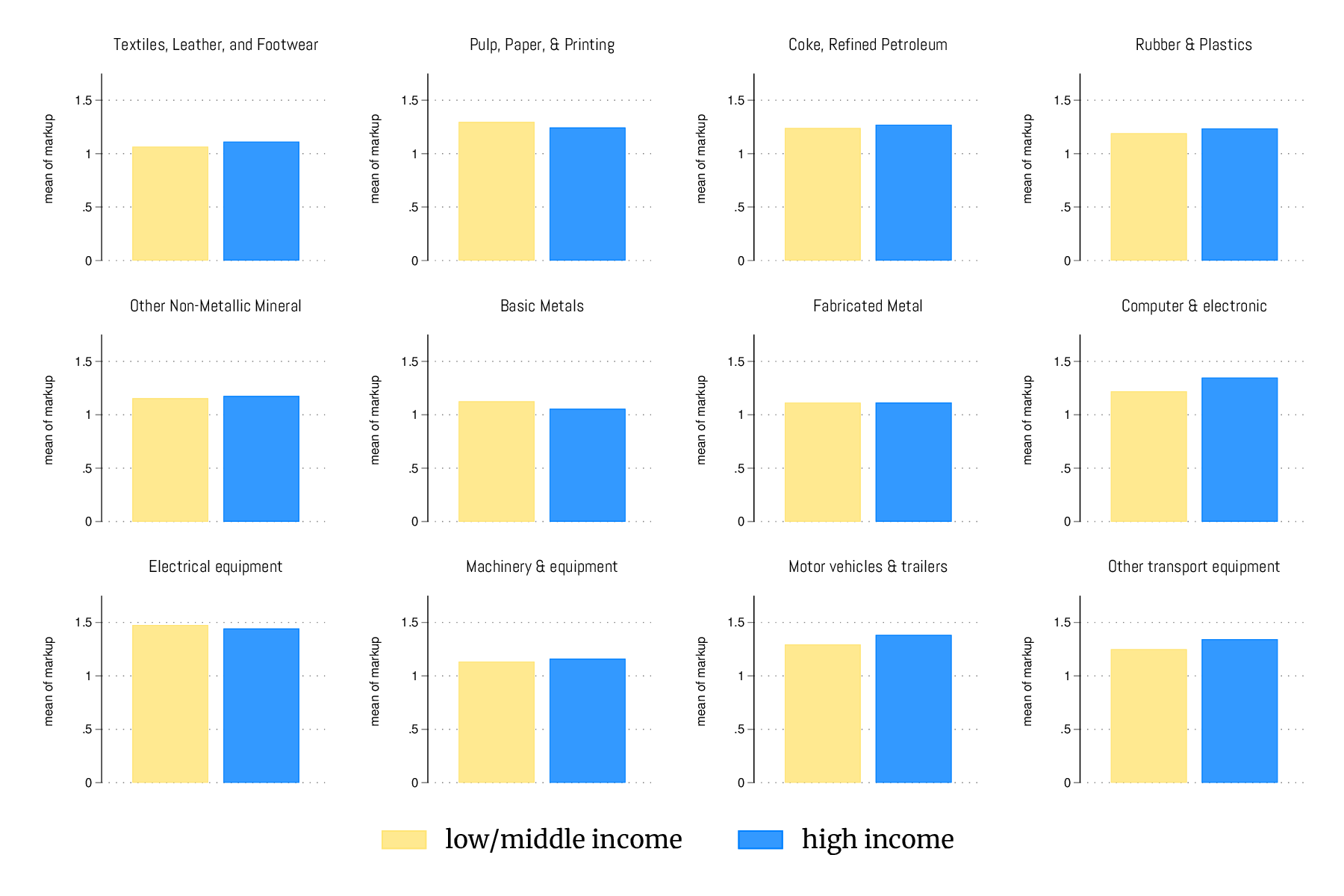

Model validation using estimated markups: A common implication of models featuring Pareto-distributed productivity and separable demand, such as ours, is that, although countries may differ in their aggregate markup distributions, they share a common markup distribution within narrowly defined industries. For this prediction to hold empirically, the industry classification must be sufficiently disaggregated. Using the ICIO industry codes, we assess this requirement by examining whether within-industry markup distributions are similar across countries. We do so by partitioning the WORLDSCOPE dataset into firms headquartered in high-income and low-/middle-income economies. We then compare average markups at the industry level across these two groups (Appendix Figure A.8). The results indicate that within-industry average markups are virtually identical across income groups, supporting the consistency of our semi-parametric framework with the data. In short, the ICIO industry classification is granular enough for our framework to be empirically valid.

6.3 The Welfare Loss from Market Power: A Global Perspective

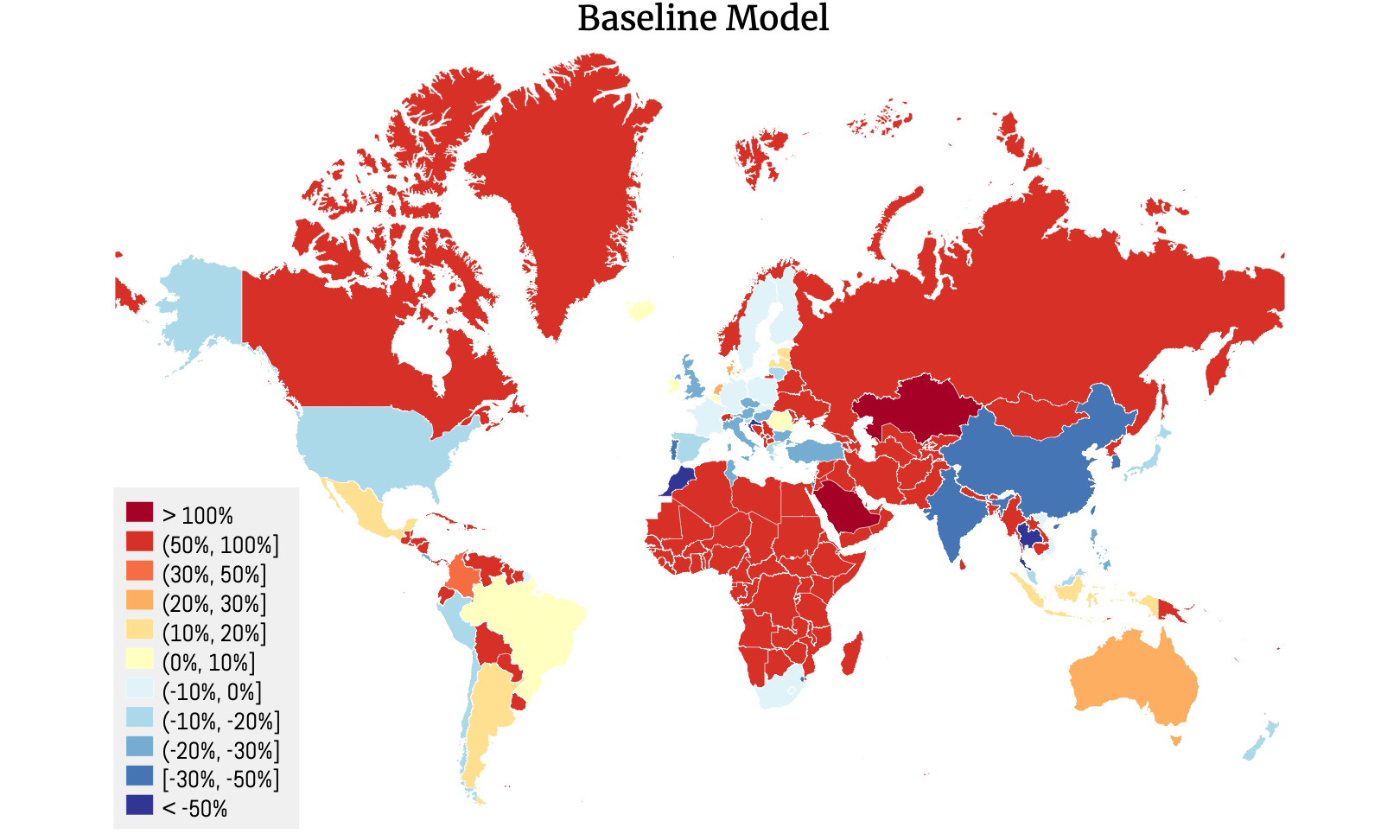

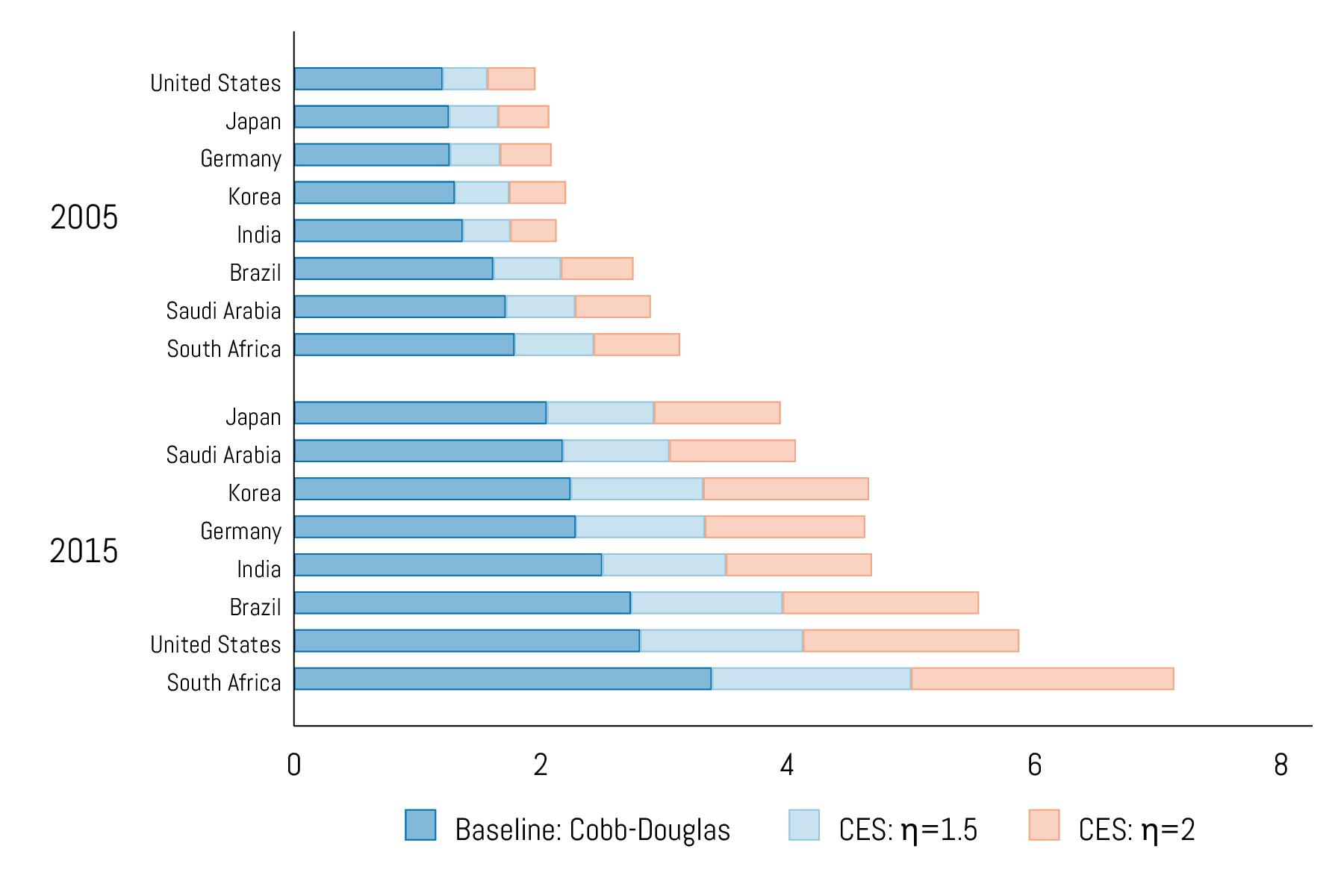

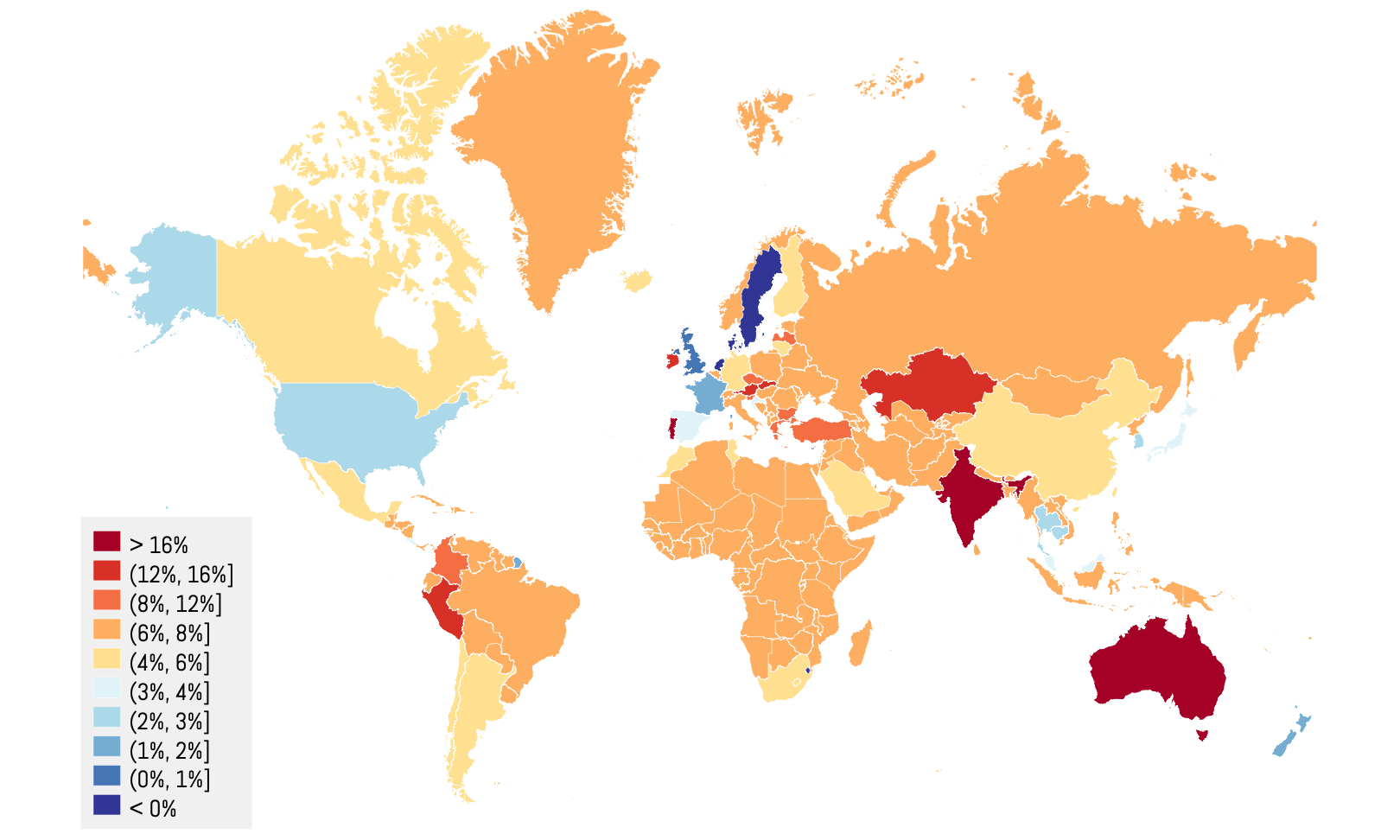

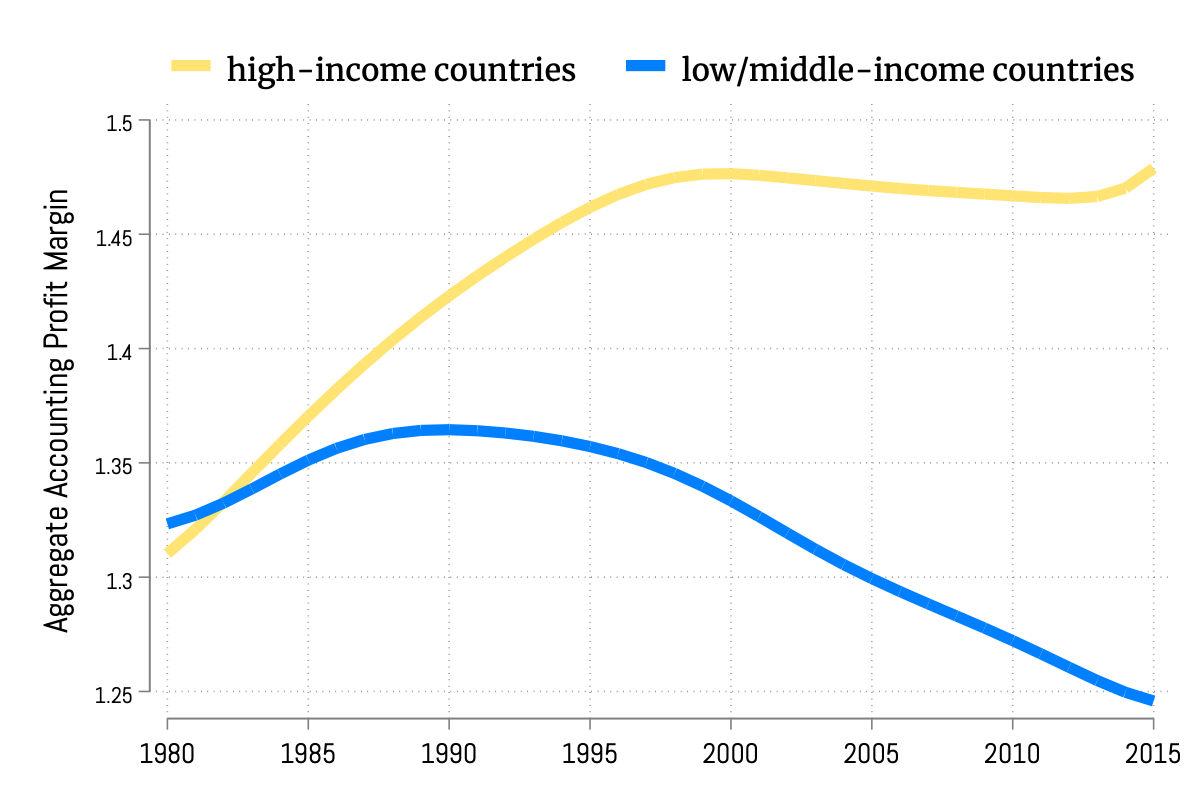

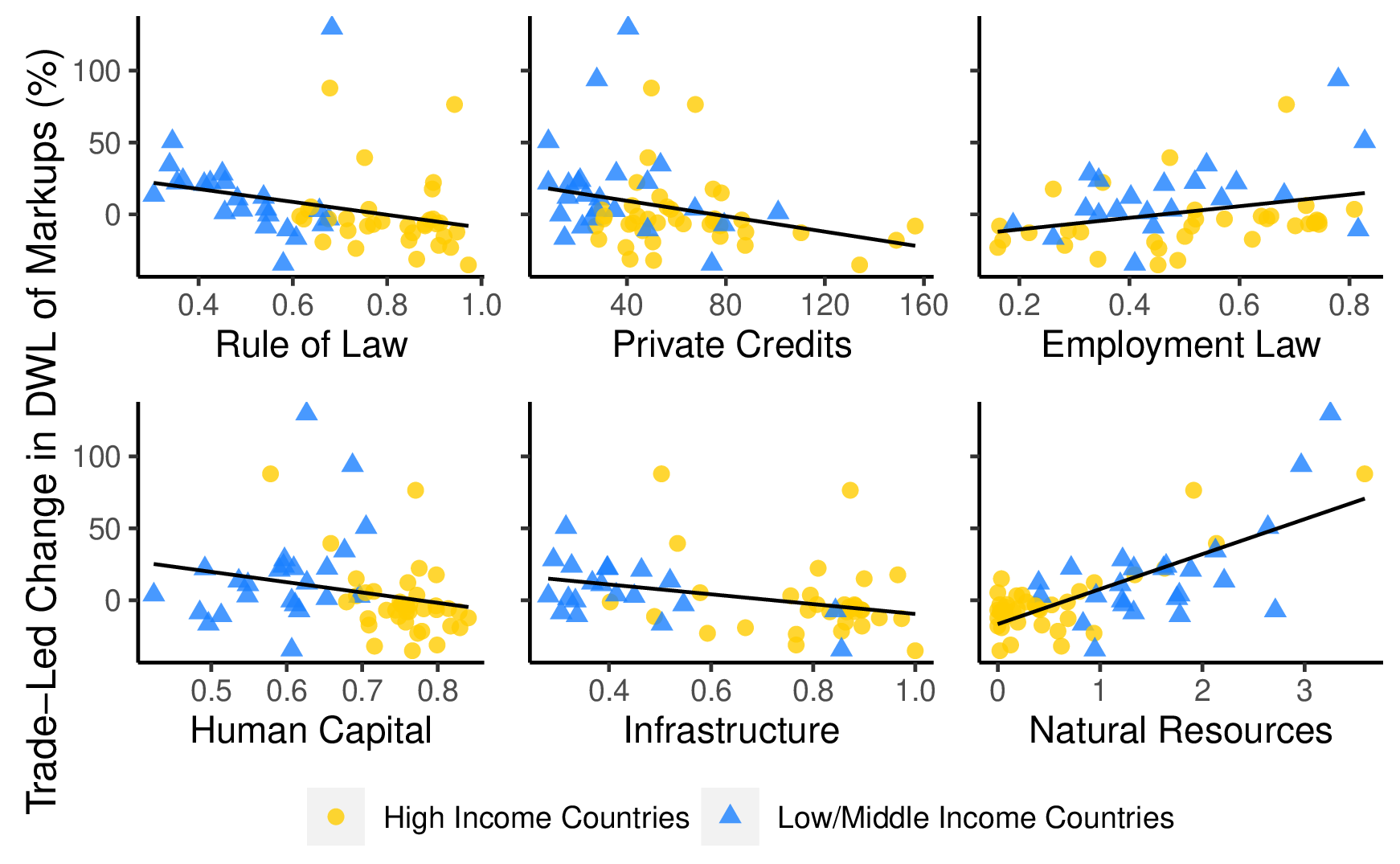

In this section, we report the aggregate loss from market power for various countries, which is the sum of the welfare loss due to markup dispersion and the country’s exposure to international profit-shifting externalities. We compute the welfare loss by plugging our estimated markup values and share data into our semi-parametric formula for \(\mathscr {D}_{i}\). Figure 4 presents the results when multi-national profit payments are accounted for. The welfare loss from market power is noticeably higher in low-income regions. Remarkably, some high-income countries, such as the Netherlands, actually benefit from markup distortions.It is important to emphasize that without trade, all countries would have experienced losses from markup distortions. This indicates that for these countries, the positive gains from profit-shifting more than offset the loss from markup dispersion. However, as noted earlier, profit-shifting effects are zero-sum, meaning that these benefits come at the expense of other nations, primarily low-income ones.

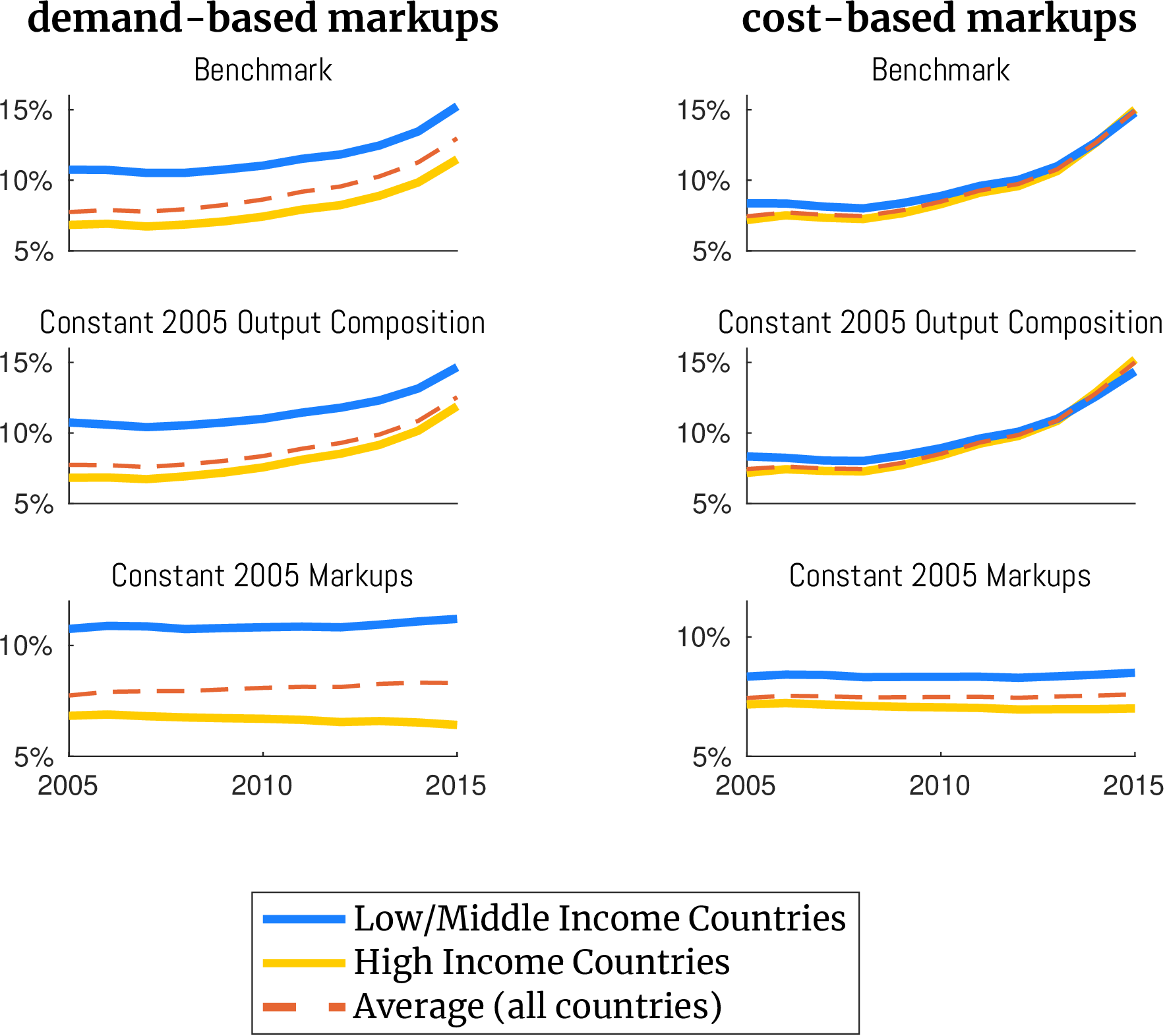

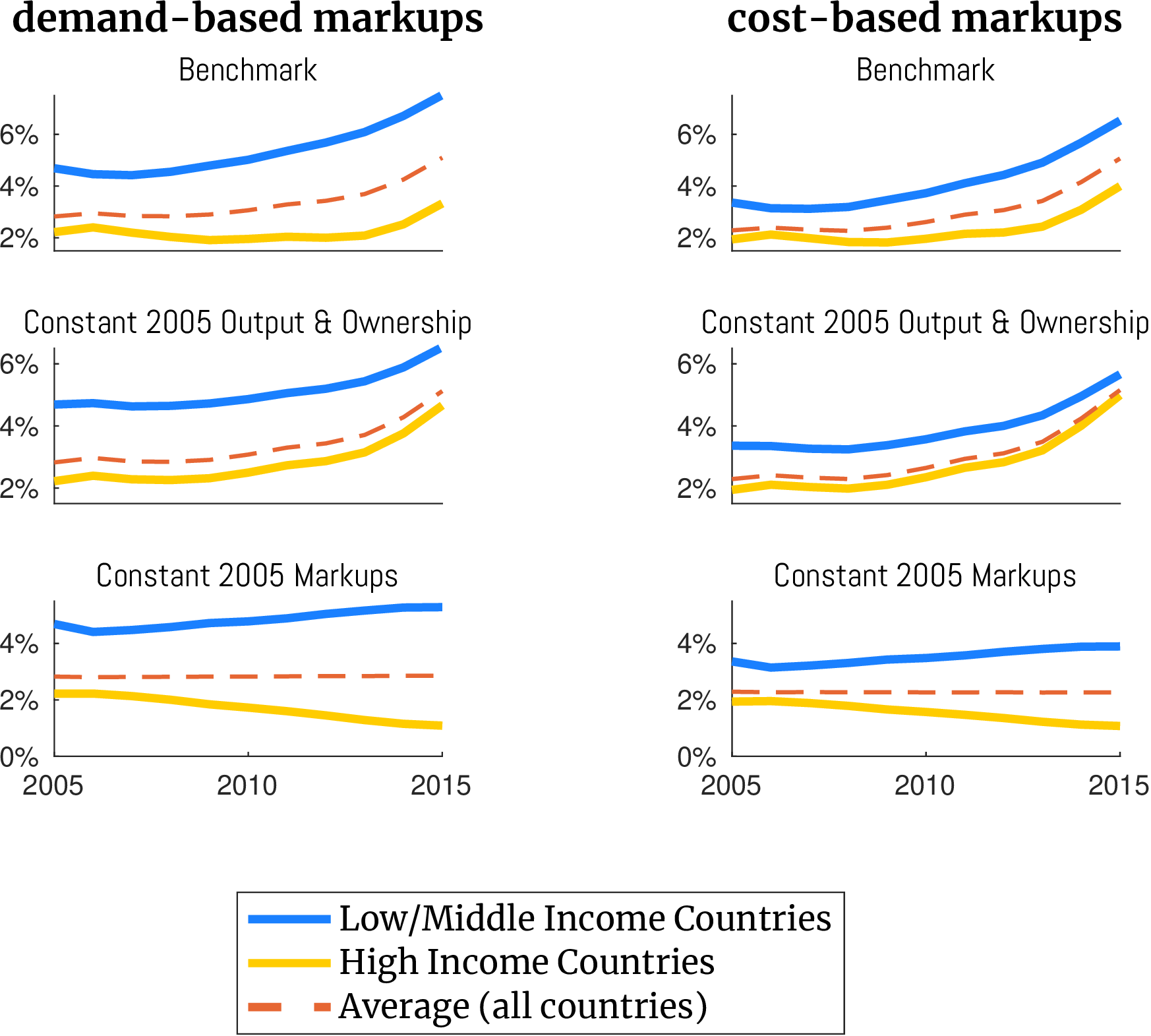

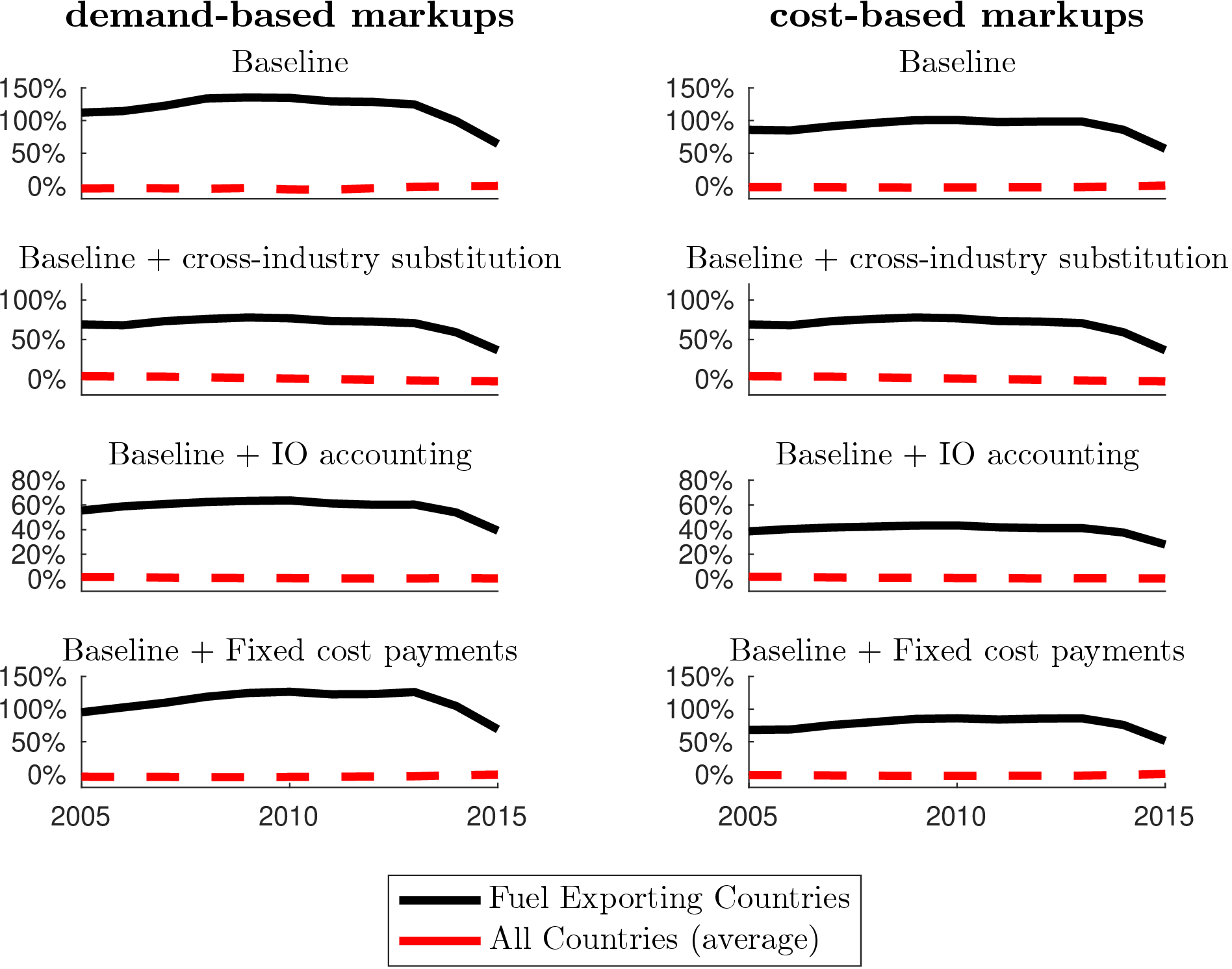

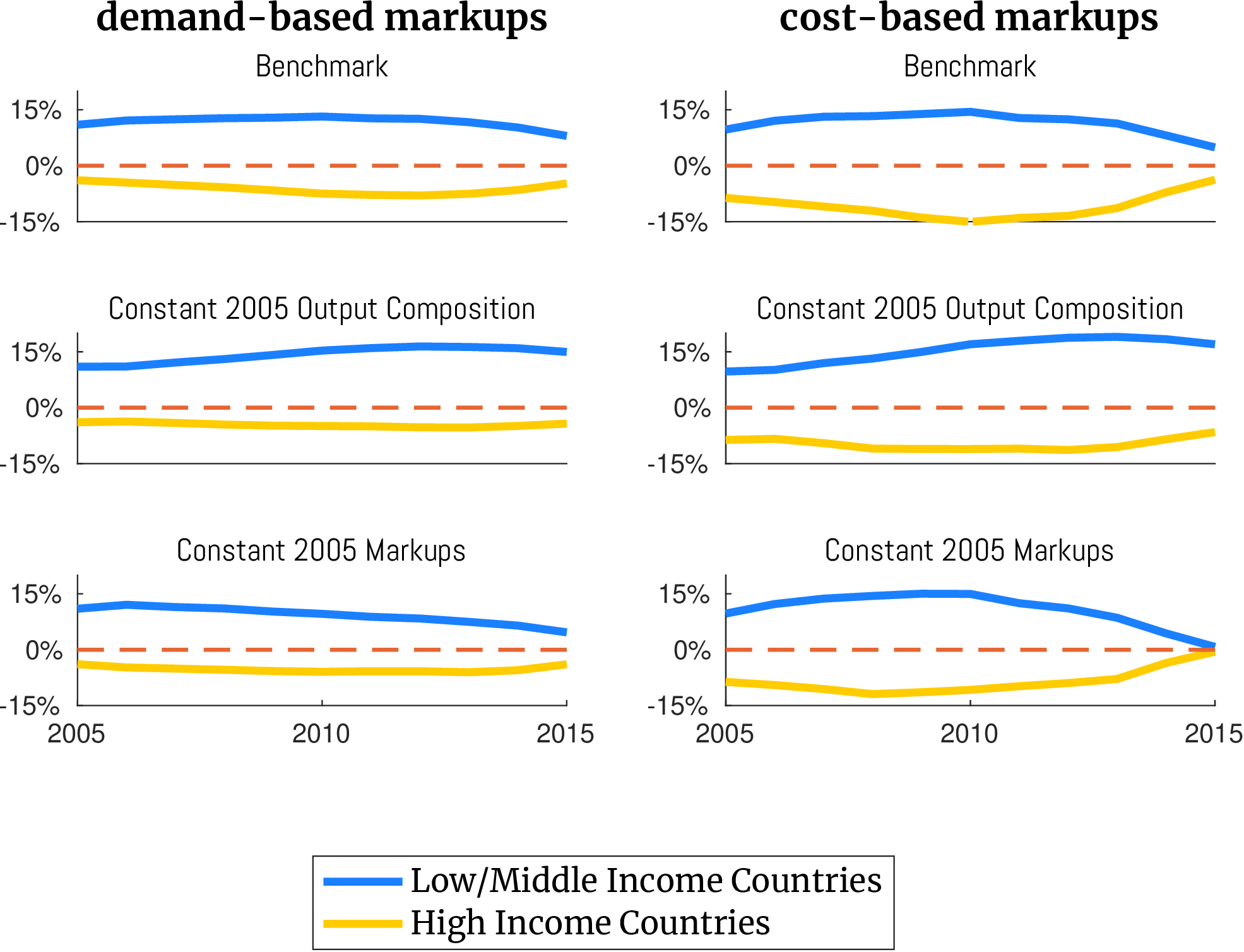

We next examine whether the welfare loss from market power has increased over time. Figure 5 presents the findings, tracing the change in the welfare loss from market power between 2005 and 2015. The y-axis denotes the welfare loss, quantified as the percentage loss in real consumption due to markup distortions. The figure presents GDP-weighted averages for high-income and low/middle-income groups, categorized according to the classification outlined in Table A.3. The left panel showcases the welfare loss calculated using demand-based markup estimates, while the right panel displays results derived from cost-based markup estimates. The results in Figure 5 point to substantial welfare losses, but it is important to recognize that these estimates may still understate the true extent of the loss, as they do not take into account the amplification from input-output linkages demonstrated in Figure A.9 in the appendix.A higher substitution elasticity between aggregate industries also amplifies the welfare loss from markup distortions. Figure A.13 in the appendix shows that the welfare rises significantly with a higher cross-industry elasticity of substitution. For the US, increasing elasticity from 1 to 2 more than doubles the welfare loss from markups. This is because resource allocation across industries becomes more sensitive to markup distortions as substitutability increases.

Figure 5 clearly illustrates that markups result in a greater welfare loss for low-income countries compared to high-income nations. Moreover, the welfare loss has been steadily increasing over time, with the trend being particularly acute among low-income nations. While these results are consistent with the existing literature on the rise of market power, there are two noteworthy aspects that set our analysis apart. First, rather than focusing on the sales-weighted average markup as De Loecker et al. (2020), we directly quantify the welfare loss of markups based on theoretical foundation. This distinction is crucial, as the average markup can, in principle, increase without necessarily leading to a greater welfare loss for the economy. Second, prior studies have primarily relied on cost-based markup estimates to document the rise in market power. However, Figure 5 suggests that the same pattern emerges even when demand-based markup estimates are employed.

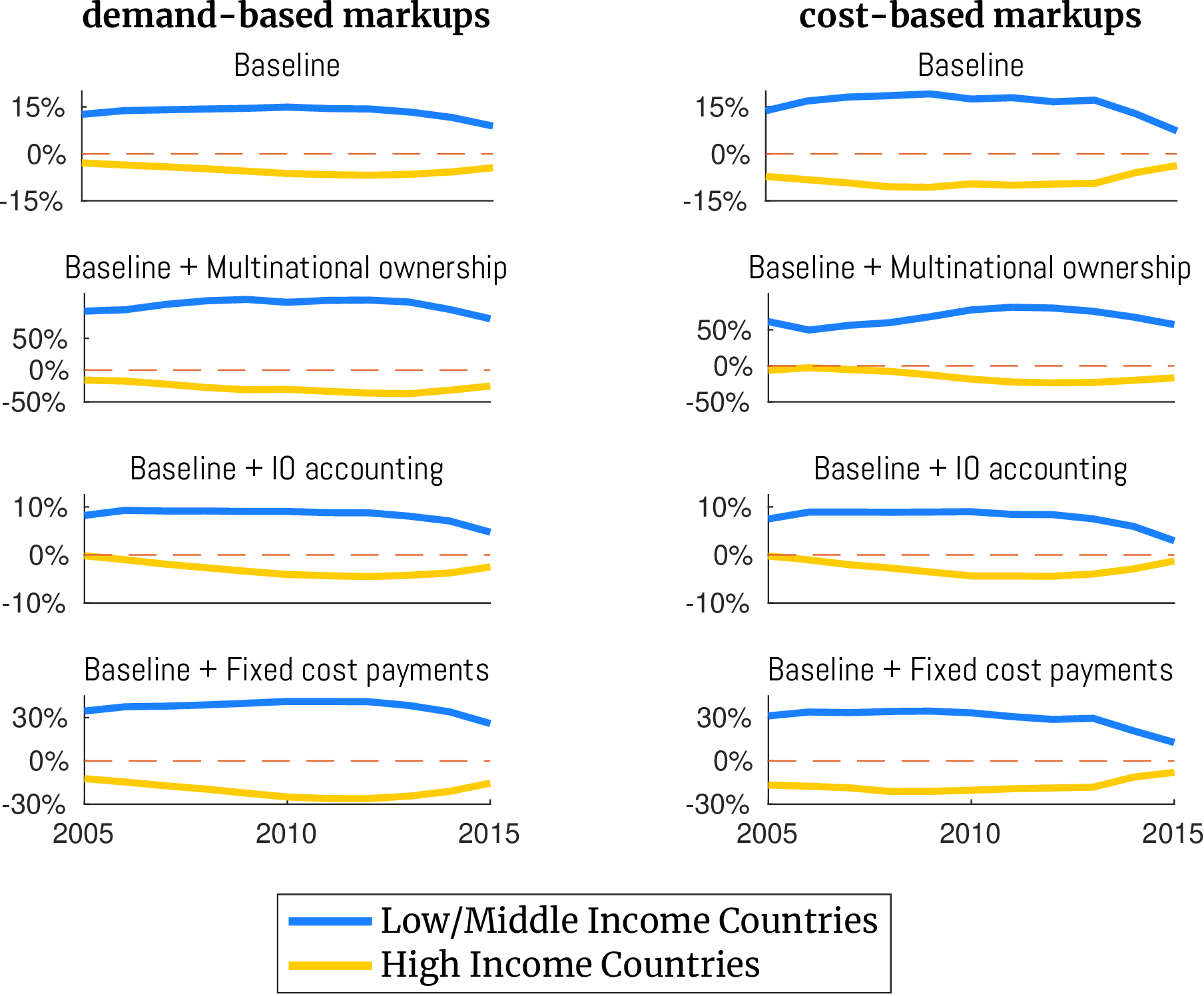

The lower panels in Figure 5 decompose the change in markup distortions into changes driven by \((1)\) adjustments to output composition and multinational profit payment over time, and \((2)\) adjustments to markup levels over time. The middle panel takes a ceteris paribus approach, holding output and expenditure shares constant at their 2005 levels. This allows us to isolate the effect of changing markup levels on the welfare loss measure, \(\mathscr {D}_{i}\). Conversely, the bottom panel keeps markups fixed at their 2005 levels and tracks the change in \(\mathscr {D}_{i}\) that can be attributed to shifts in the economic composition. The results from these lower panels are quite revealing. They demonstrate that the global increase in the welfare loss from markups is entirely driven by changes in markup levels over time. Meanwhile, the change in output composition and multinational profit payment has merely redistributed the burden of markup distortions, shifting it from high-income countries to their low-income counterparts. These findings provide an initial glimpse into the zero-sum nature of profit-shifting effects, which are formally quantified in the following section.

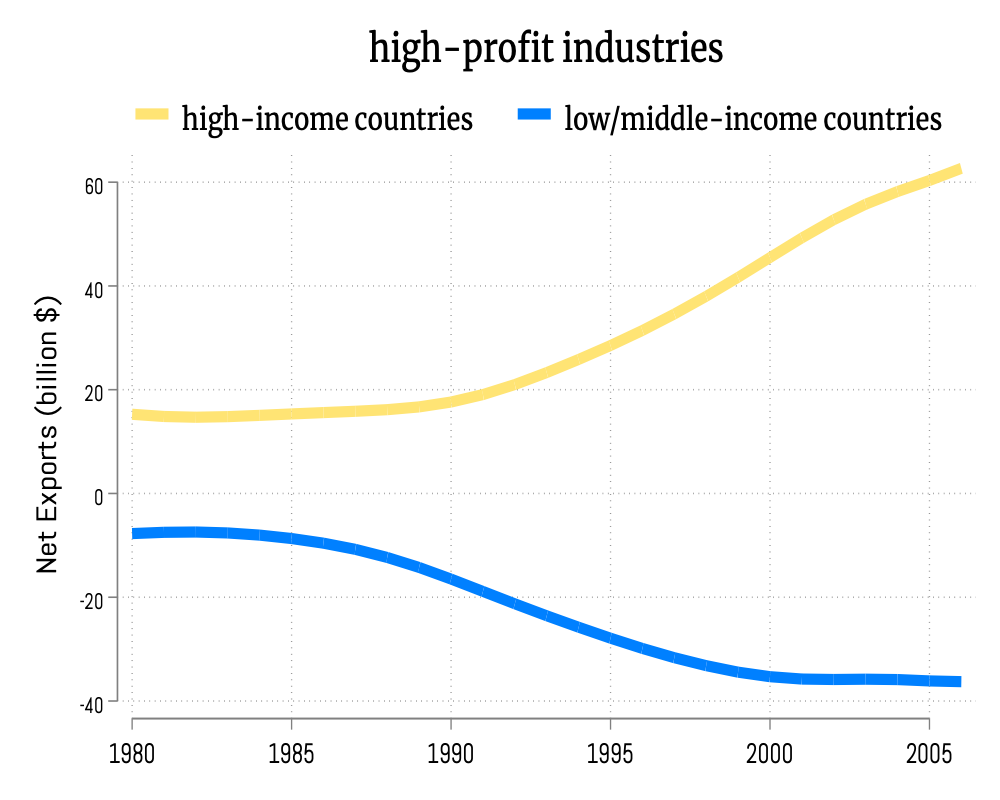

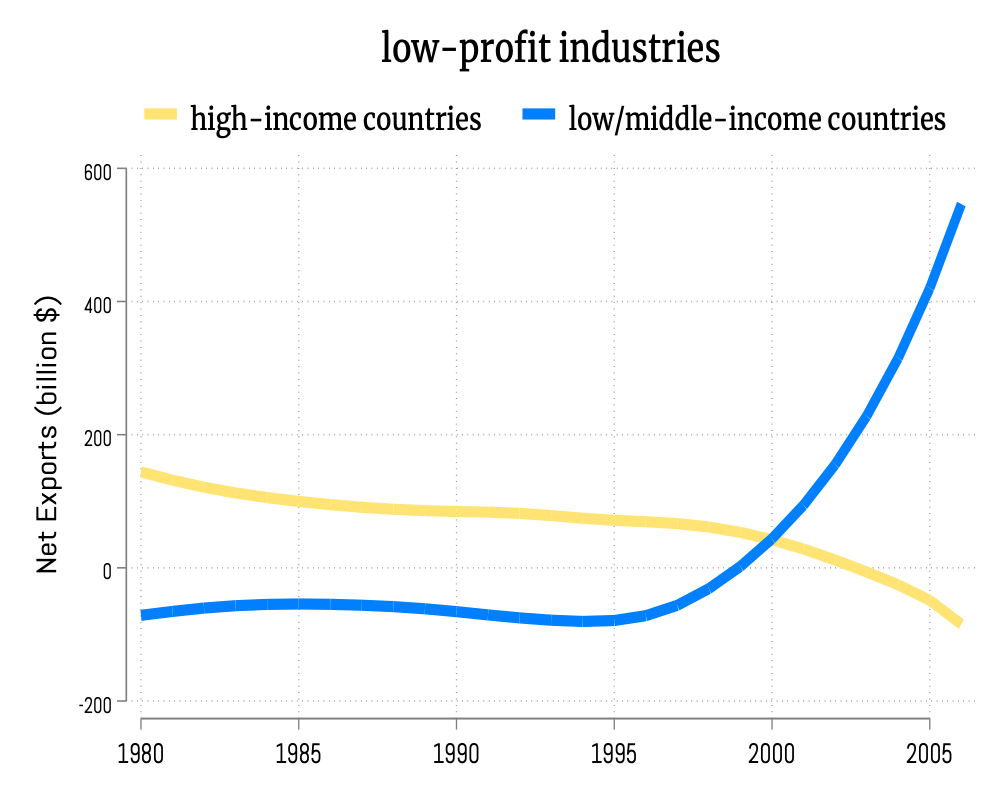

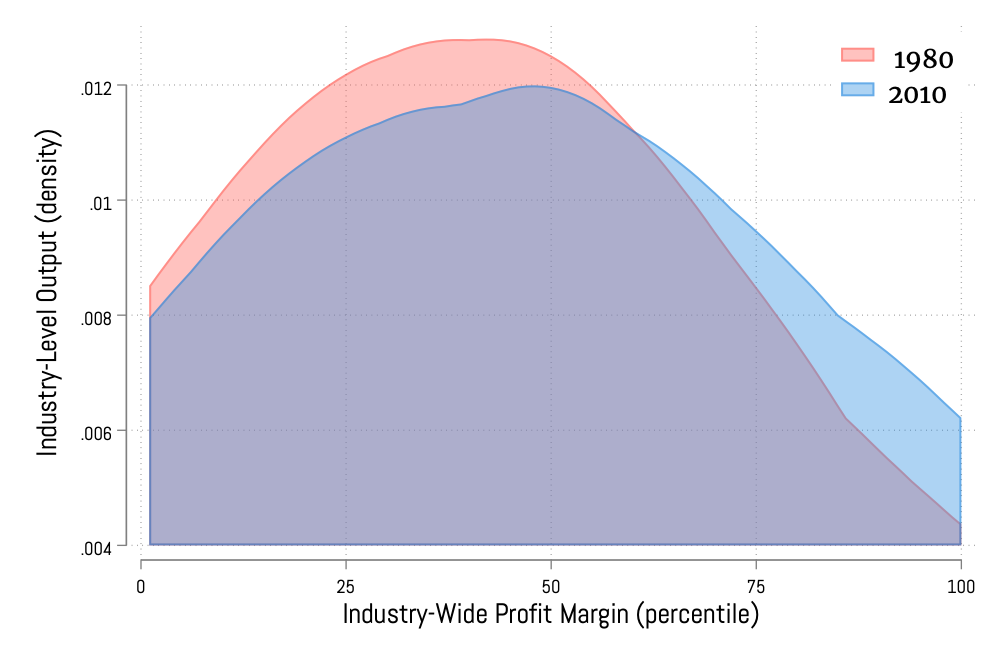

6.4 Profit-Shifting Effects: North-South Redistribution